GBP/USD analysis: UK data disappointed big, no rate hike at sight

GBP/USD Current price: 1.3779

- Market players dumped expectations of a BOE's rate hike next May.

- UK April Markit PMIs will be out this week and could hurt the Pound even further.

The Sterling Pound plunged for a second consecutive week, settling against its American rival at 1.3779, its lowest in nearly two months, as the UK preliminary Q1 GDP disappointed, adding to the latest batch of sour data and further fueling speculation that the BOE won't raise rates next May, as previously expected. According to the official figures, growth in the UK slowed to 0.1% in the first quarter, well below the previous 0.4% or the expected 0.3%. US Q1 preliminary GDP, on the other hand, came in better-than-expected as the country is estimated to have grown 2.3% during the three months to March, against the expected 2.0%. The UK Markit PMIs on manufacturing, construction, and services for April will be out this week, forecasted to have improved from March figures. If that's the case, the Pound could see some relief, but poor readings will add to the bearish case, despite the pair shed roughly 600 pips in this last two weeks.

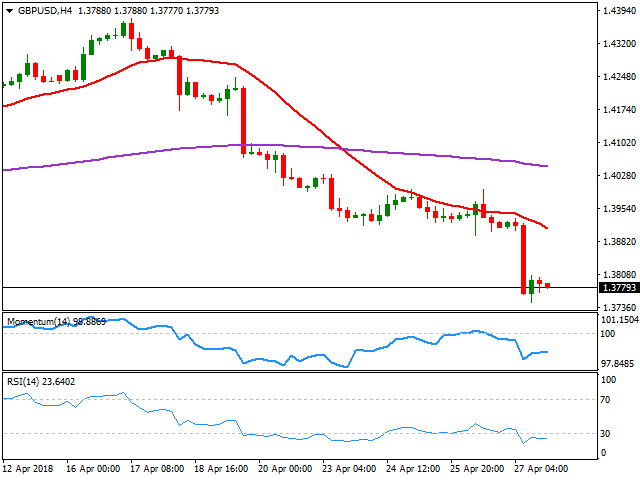

The GBP/USD pair is technically bearish according to the daily chart, as the pair settled far below its 20 DMA, which slowly gyrates south, while technical indicators maintain their strong downward slopes near oversold readings. Shorter term, and according to the 4 hours chart, the risk is also leaned to the downside, as a bearish 20 SMA has been steadily capping the upside, now around 1.3900, while technical indicators stalled their recoveries from extreme oversold levels and the RSI already turned south, currently at 23. The pair bottomed at 1.3746 last Friday, making of the level and immediate support and the one to break to confirm additional declines ahead.

Support levels: 1.3745 1.3710 1.3680

Resistance levels: 1.3820 1.3860 1.3900

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.