GBP honeymoon period ending way sooner

News that the British government is to legislate against an extension of the Brexit transition period - meaning a 'hard Brexit' could be back on the table - is taking positive 'hope' premium out of sterling. This is in line with our V-shape EUR/GBP profile, and transition uncertainty will weigh on the pound in 1H20; in fact, GBP looks to have reached its peak.

Market pricing out positive GBP "hope" premium

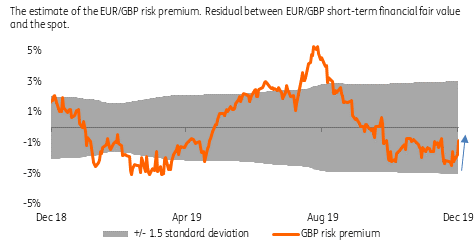

We are observing a big reversal in sterling's post-election gains in response to news that PM Boris Johnson intends to legislate against the possibility of extending the Brexit transition period, which is due to finish at the end of 2020. Leaving without a trade deal at the end of next year is much the same as a hard Brexit and that's clearly negative for sterling. Consequently, any positive “hope” premium is currently being priced out of GBP, and our short-term financial fair value model suggests that EUR/GBP is currently 0.8% undervalued (vs the 2% undervaluation yesterday – Figure 1). This means that EUR/GBP can easily get back to the 0.8500 level without any (short-term) valuation constraints.

Our medium-term BEER fair value estimates also suggest that EUR/GBP 0.8500 is the pair’s medium-term value (meaning that GBP is currently not trading cheaply - see G10 FX valuation).

Figure 1: Positive “hope” premium being priced out of sterling

Source: ING

V-shaped EUR/GBP profile unchanged, but bottoming just sooner

Our EUR/GBP profile was always V-shaped: we expected GBP strength after the election but looked for a reversal of some of the sterling gains around 2Q20 due to the anticipated uncertainty about the extension of the transition period. However, the news that the British Prime Minister wants to legislate to ensure parliament can't demand an extension of the transition period brings the trough in EUR/GBP way earlier and ends the sterling honeymoon period sooner than we had expected.

Still, the bottom line is the same. As we argued in our 2020 FX Outlook, the likely passage of the Withdrawal Agreement isn’t the end of Brexit saga. Uncertainty about the extension of the transition period will weigh on GBP and the latest reports suggest that the anticipated uncertainty is likely to curb GBP gains just sooner than originally expected.

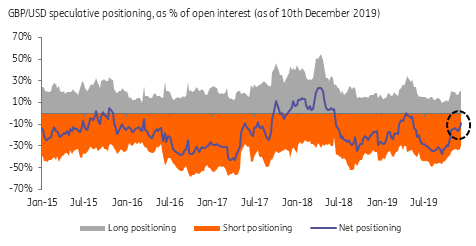

Position way cleaner and won’t prevent possible further GBP drop

From a technical point of view, we note that short GBP speculative positioning is likely to be cleaner at this point. As we note in our report, FX Positioning: Sterling heading to the neutral zone, the sterling speculative shorts (as reported by the CFTC) declined to 9% of open interest as of last Tuesday (vs close to 40% in mid-September). The latest reported data still doesn't cover the post UK election clean-up, meaning that speculative shorts are likely to be even lower than the latest data suggest. From this perspective, the cleaner positioning won’t be a factor preventing a possible further GBP drop.

Figure 2: Short GBP speculative positioning is cleaner

Source: ING, CFTC

Tricky 1H 2020 for GBP ahead, but gains in the latter part of 2020 still likely

Should the reports be true and the government legislates against an extension of the transition period, this means that we have likely seen a local peak in sterling. EUR/GBP is unlikely to test the 0.8300 level again in the coming months and GBP/USD won’t be biased to converge towards last Friday’s peak (of close to 1.3500).

Our economists still see the extension of the transition period, in one form or another, as the most likely scenario (as eleven months is a too short a period to complete complex trade negotiations), but the uncertainty about it should curb GBP gains during 1H 2020. This means that it is likely that any more pronounced GBP gains are to be backloaded into the latter part of 2020.

This is in line with our forecast where we expect GBP/USD to drop to 1.31 by 2Q20 but to rise towards 1.38 by 4Q20 on the back of optimism caused by the eventual extension of the transition period or, alternatively, a bare-bones trade agreement with a subsequent implementation phase baked in.

Author

Petr Krpata, CFA

ING Economic and Financial Analysis

Petr Krpata is an FX strategist at ING and has been covering G10 and CEE currencies since May 2014. Previously, he was an FX and Rates strategist at Barclays Wealth and Investment Management.