Gas prices are rising again, and that hurts Europe’s inflation fight

Europe could be facing a familiar economic challenge: inflation caused by imports. The rise of energy costs is enough to revive an uncomfortable question for policymakers: Is the ghost of stagflation coming back?

Dutch TTF Gas futures have climbed toward the €64/MWh area, extending their recent rally as geopolitical tensions and supply uncertainties push energy markets higher.

While prices remain far below the extremes seen during the 2022 energy crisis, a continued rise in energy costs could challenge Europe’s disinflation narrative.

Energy as an inflation channel

For the euro area, energy prices carry disproportionate macroeconomic weight.

Europe's energy situation is quite different from that of the United States, where a strong domestic energy supply is a given. The continent, in contrast, is heavily dependent on imported fuel, with Natural Gas being a critical component. It's the backbone of electricity generation, industrial processes, and heating systems.

Consequently, when Gas prices climb, the repercussions are felt throughout the economy almost immediately.

Increased wholesale energy prices translate into higher electricity bills, escalating costs for industrial operations, and, eventually, consumer inflation. Even modest increases can have outsized effects on headline inflation because of energy’s weight in consumer baskets.

In other words, energy shocks tend to arrive from outside the Euroland, but their inflationary impact is felt at home.

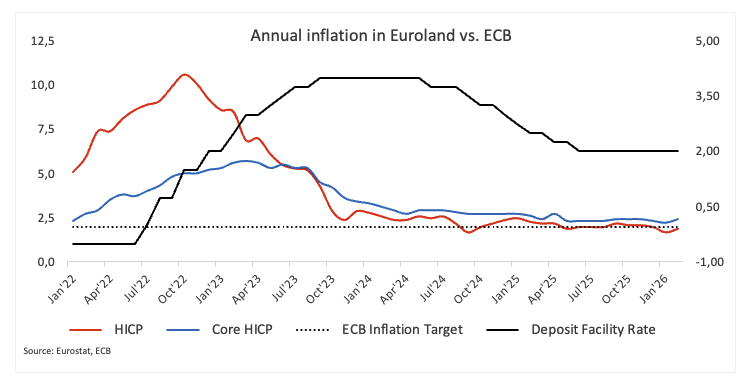

A fragile disinflation process

This matters because Europe’s inflation outlook had been gradually improving.

Energy costs, having dropped considerably from their earlier highs, contributed to a decrease in headline inflation, which in turn opened the door for a more accommodating policy approach.

However, the recent uptick in gas prices could throw a wrench into that plan.

Should the energy sector start to drive headline inflation up once more, it could hinder the progress of disinflation, even if the core price pressures stay relatively stable.

For the European Central Bank (ECB), that creates a familiar policy dilemma.

The ECB’s balancing act

The ECB is already navigating a delicate environment.

Growth across the euro area remains uneven, and parts of the industrial sector continue to struggle with weak demand and elevated input costs.

At the same time, policymakers remain cautious about declaring victory over inflation too quickly.

If Gas prices continue climbing, the risk is not necessarily a return to crisis-level inflation. Rather, it is that the final stretch of the disinflation process becomes slower and more uncertain.

That could limit the ECB’s room for manoeuvre.

The external vulnerability

Energy shocks also highlight a structural feature of the European economy.

Because the euro area imports a large share of its energy, rising fuel prices effectively act as a transfer of income abroad. Higher import bills weaken the region’s terms of trade and can weigh on growth even as they push inflation higher.

That combination, slower growth alongside rising prices, is precisely the type of macro environment central banks prefer to avoid.

FX implications: Not good news for the Euro

The currency markets present a clear picture.

Should Europe experience imported inflation due to rising energy prices, coupled with a weak growth outlook, the Euro could find it difficult to maintain a strong position against currencies supported by robust domestic energy sectors.

Historically, when Gas prices are high, the Euro often faces pressure, especially when the US economy demonstrates greater resilience.

Energy markets do not move currencies directly, but they can shape the macro backdrop that ultimately drives them.

-1773240322405-1773240322406.png)

Bottom line

At €64/MWh, Europe’s Gas prices are far from crisis territory, but they are moving in a direction that matters.

If the rally proves temporary, the inflation impact will likely remain manageable.

If it persists, Europe may once again face the uncomfortable reality of importing inflation from global energy markets, just as policymakers were beginning to believe the worst of the energy shock had passed.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.