US Dollar Weekly Forecast: The higher-for-longer trade lives on

- The US Dollar advanced markedly this week, hitting fresh yearly tops.

- The Fed’s hawkish hold lends extra legs to the buck’s recovery.

- Investors now see the Fed hiking its interest rates in September.

The week that was

A very auspicious week saw the US Dollar (USD) trade with robust gains, rapidly leaving behind the prior pullback and sending the US Dollar Index (DXY) to levels last traded in mid-May 2025, past the 101.00 barrier on Friday.

Indeed, the Greenback managed to regain strong and renewed upside traction following Wednesday’s hawkish hold by the Federal Reserve (Fed), the first meeting under Kevin Warsh’s realm.

Meanwhile, geopolitics has remained a central focus, particularly after the US and Iran reached a Memorandum of Understanding (MOU) over the past weekend, which both parties have signed electronically. The planned meeting in Switzerland to discuss the technical terms of the ceasefire deal was postponed.

Regarding the US money market, Treasury yields behaved in a mixed tone across various maturity frames: a solid bounce to more than a year's highs past 4.20% in the short end, while the belly remained somewhat consolidative below 4.50% and the long end slipped back to levels last seen in mid-April near 4.85%.

What about the US docket? The only release of note was firmer-than-expected results from Retail Sales in May.

Fed holds rates steady as Warsh signals a new approach

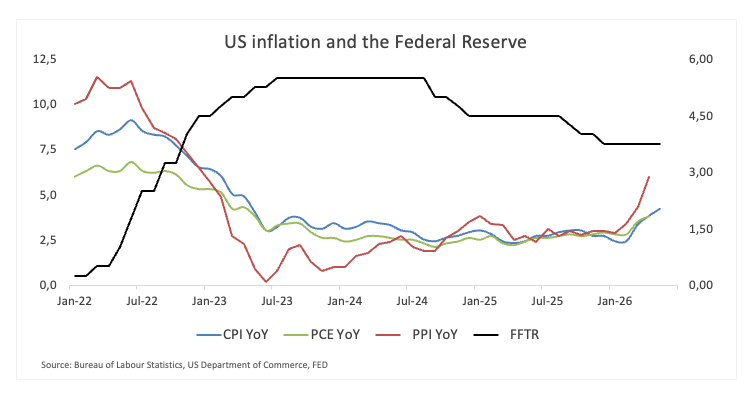

The Federal Reserve left interest rates unchanged at 3.50%-3.75% on Wednesday, but the updated projections and Kevin Warsh's first press conference delivered a clear higher-for-longer message.

The statement acknowledged that economic activity continues to expand at a solid pace despite uncertainty linked partly to the conflict in the Middle East. Policymakers also noted that inflation remains elevated, with recent supply shocks and higher energy prices contributing to ongoing price pressures.

The biggest surprise came from the Summary of Economic Projections (SEP). Fed officials sharply raised their inflation forecasts, with PCE inflation now seen at 3.6% in 2026 versus 2.7% previously, while inflation is still not expected to return to the 2% target until 2028. Policymakers also lifted their projected rate path for 2026, 2027 and 2028, reinforcing the view that rates are likely to stay higher for longer.

In his first press conference as chair, Warsh repeatedly stressed the Fed's commitment to restoring price stability, calling that commitment unanimous and unambiguous. He argued that persistently high prices remain a burden on households and maintained that inflation is primarily determined by monetary policy.

Warsh also used the occasion to signal broader changes at the central bank. He announced a review of the Fed's communications, balance sheet framework, data sources and inflation models, adding that changes to the SEP could be proposed later this year.

The overall message was straightforward: the Fed remains focused on inflation, sees little urgency to ease policy and is entering what Warsh described as a "new chapter" for the central bank.

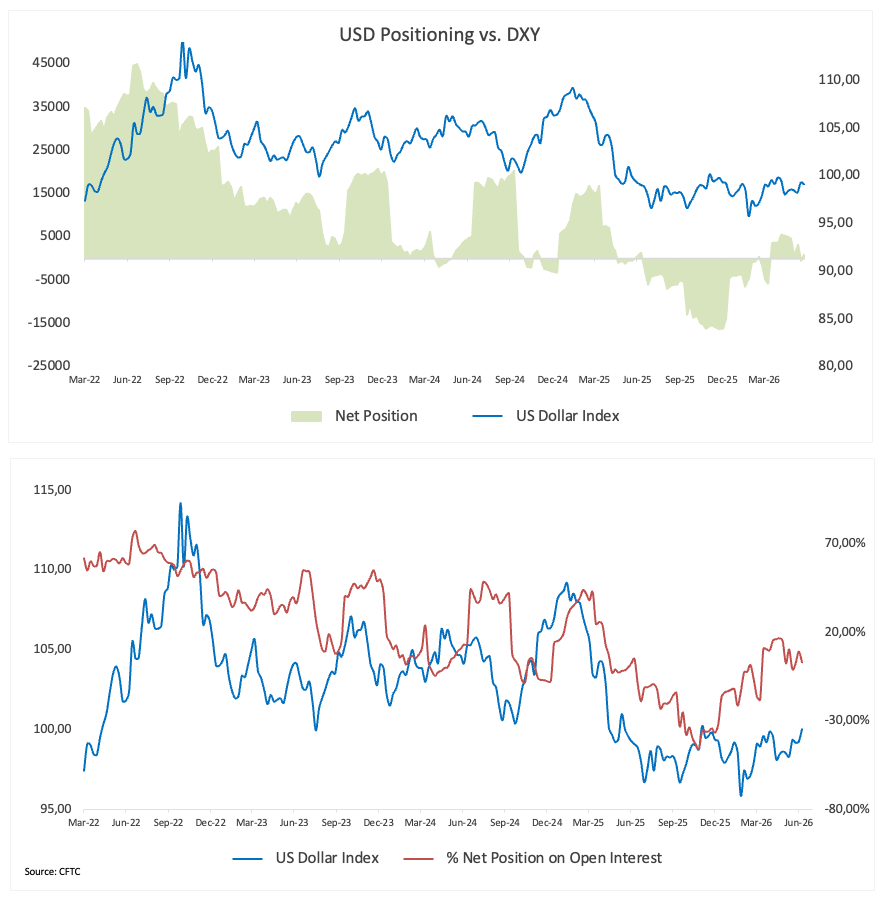

Speculators are watching closely, still unconvinced

Speculative positioning in the US Dollar remained relatively subdued in the latest reporting week, according to the Commodity Futures Trading Commission (CFTC). Net longs eased to around 1.4K contracts for the week ending on June 9, with both weekly and four-week changes remaining negative, suggesting investors continue to trim their exposure to the Greenback.

From a historical perspective, positioning remains light. The current net position ranks in just the 29th percentile of its 5-year range, while speculative exposure stands at 3%, corresponding to the 28th percentile. Together, these metrics indicate that speculative interest in the US Dollar remains below average, leaving positioning far from the crowded conditions typically associated with major turning points.

Inflation refuses to fade

As widely anticipated, inflation picked up notably in May.

Headline Consumer Price Index (CPI) inflation accelerated to 4.2% YoY from 3.8% in April, while core CPI, which strips out food and energy costs, increased by 2.9% from 2.8%.

The latest figures raise an uncomfortable question for policymakers and investors alike: what if the disinflation story that dominated the first part of the year is already beginning to lose momentum?

A renewed surge in Oil prices following the continued closure of the Strait of Hormuz has added fresh inflationary pressure to the mix, although this week's US-Iran deal sent crude Oil prices tumbling to multi-week lows in the vicinity of the $72.00 mark per barrel of WTI, challenging at the same time its critical 200-day SMA.

At the same time, the delayed effects of US tariffs are only now starting to work their way through supply chains and into consumer prices.

Taken together, it is precisely the kind of backdrop markets were hoping to avoid: inflation proving stubborn just as the US “exceptionalism” narrative remains well and sound.

What comes next for markets?

Attention now shifts to next week's Personal Consumption Expenditures (PCE) data as well as the final Q1 GDP Growth Rate.

Markets will be watching closely to see whether the data confirm the message that inflation remains uncomfortably above the Fed's 2% target and may stay there for longer than previously expected.

Beyond the data, investors will continue to track developments in the Middle East and the progress (or lack of it) of the recently clinched MOU between the US and Iran.

Fed speakers will add to the mix and are also expected to be a source of fresh volatility post-FOMC event.

The Fed rethink gathers pace

Until recently, investors operated under a relatively simple assumption: the Fed’s next significant move would eventually be towards lower interest rates.

That view is now in the rear-view mirror.

Sticky inflation, resilient economic activity, higher energy prices and renewed supply-chain disruptions have all complicated the path back towards policy easing. Perhaps more importantly, Fed officials no longer appear fully convinced that inflation will continue drifting lower without additional help from restrictive policy.

None of this necessarily points to an imminent rate hike. But what about a September hike?

It does, however, suggest that the hurdle for rate cuts has risen considerably, if not utterly disappeared.

For the US Dollar, that matters.

Higher-for-longer rates should continue to underpin Treasury yields and offer support to the Greenback.

Why the US Dollar keeps finding support

If there is one lesson from recent months, it is that bringing inflation down from very high levels is often easier than eliminating the last stretch of price pressures.

For now, that may be the US Dollar's biggest source of support.

Markets may simply have underestimated how difficult the final phase of the inflation fight was always going to be.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.