The Iran war didn't break the US economy, but what happens next?

Nearly four months after the start of the Iran war, the US economy remains remarkably resilient. While the conflict initially triggered a severe disruption to global energy markets and a sharp rise in Oil prices, recent diplomatic progress between Washington and Tehran has eased concerns about a prolonged supply shock. Even before the signing of a preliminary peace agreement, most economic indicators suggested that the US economy was weathering the conflict far better than many economists had feared.

The conflict has reignited inflationary pressures and fueled widespread concerns about a potential economic slowdown. Yet, most of the key indicators released since the conflict began suggest that economic activity remains solid.

While inflation has clearly accelerated and consumer confidence has deteriorated, the labor market remains relatively stable, business activity continues to expand and household spending has so far resisted the loss of purchasing power caused by higher energy costs.

The contrast between gloomy sentiment surveys and resilient hard economic data has become one of the defining features of the US economy in recent months.

The Oil shock has not derailed economic activity

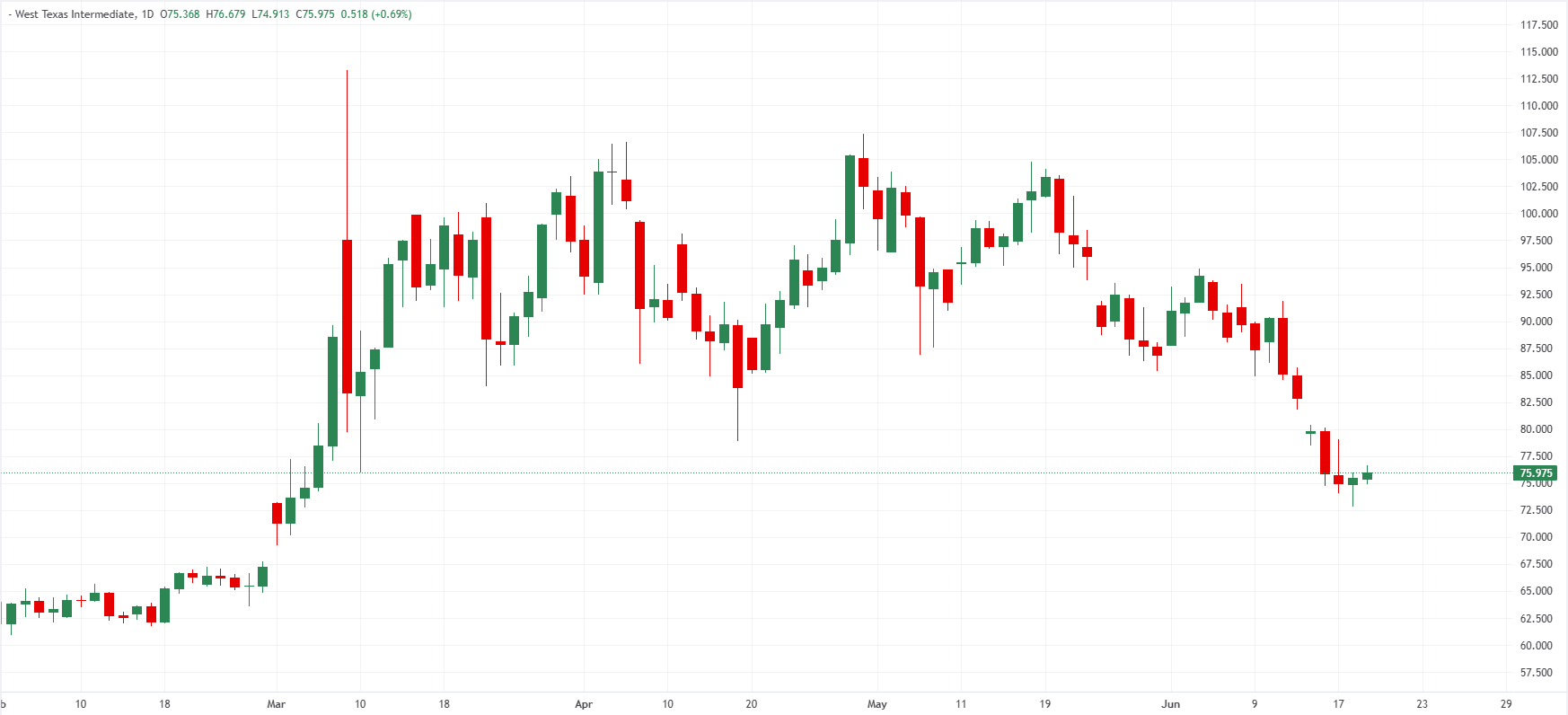

Historically, major Oil price shocks have often preceded periods of economic weakness in the United States (US). For several months, the Iran war appeared to be following that script, with Oil prices surging as the closure of the Strait of Hormuz disrupted nearly a fifth of global energy supplies.

However, recent developments have significantly improved the outlook. The United States and Iran have signed a memorandum of understanding aimed at ending the conflict, while shipping traffic has gradually resumed through the Strait of Hormuz after Washington lifted its naval blockade. As a result, West Texas Intermediate (WTI) Crude has fallen sharply from its war highs and is now trading near $76 per barrel, reducing the inflationary pressure that had built up during the conflict.

The easing in energy prices has reinforced the view that the US economy may avoid the worst-case scenarios that many economists feared earlier this year.

Despite this, activity indicators remain firmly in expansion territory. The Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) rose to 54 in May, while the ISM Services PMI climbed to 54.5. Both readings point to continued growth across the economy and stand in stark contrast with recession fears that intensified following the outbreak of the conflict.

Jonathan Golub, Chief Equity Strategist at Seaport Research Partners, recently said to CNBC that business demand remains in "clear expansion mode," noting that consumers have yet to show significant weakness despite higher gasoline prices.

Part of this resilience may stem from structural changes within the US economy. As Eswar Prasad, Senior Professor of Trade Policy and Economics at Cornell University, recently told Fortune: "The US is not the manufacturing powerhouse it once used to be." Prasad argues that the growing importance of the services sector has helped cushion the economy from the impact of higher energy prices, while America's position as a net Crude exporter provides an additional buffer against the current Oil shock.

The US labor market remains remarkably stable

Perhaps the strongest argument in favor of economic resilience comes from the labor market. While economists continue to warn that higher energy prices could eventually weigh on hiring, the latest employment data show little evidence of a significant deterioration.

Nonfarm Payrolls (NFP) increased by 172K in May, beating expectations and posting a third consecutive month of strong gains. The Unemployment Rate is stable at 4.3%, still below the 4.4% level recorded before the outbreak of the war.

Beyond payrolls, the Job Openings and Labor Turnover Survey (JOLTS) showed that Job Openings increased to 7.618M in April, the highest level since May 2024 and well above expectations. The data suggest that labor demand remains healthy despite heightened uncertainty.

Signs of cooling are nevertheless emerging. Weekly Initial Jobless Claims have been trending higher since late April and reached 226K during the week ending June 12. Even more notably, the 4-week average reached its highest level since the start of the war at 223.25K.

However, Continuing Jobless Claims remained relatively steady, printing at 1.81 million during the week ending June 5, slightly below the 1.847 million recorded during the final week of February, immediately before the conflict began.

The labor market's resilience reflects several structural factors, as the Federal Reserve’s (Fed) Beige Book has described the current environment as a "low-hire, low-fire" labor market, where companies have become more cautious about hiring but remain reluctant to lay off workers amid persistent labor shortages.

At the same time, business activity remains in expansion territory while manufacturing hiring has been supported by defense-related demand and growing investment in data centers, helping offset weakness in other sectors.

Inflation is emerging as the main economic headache

If the broader economy has so far absorbed the shock remarkably well, inflation is proving to be the clearest and most immediate consequence of the Iran war. The Consumer Price Index (CPI) accelerated to 4.2% YoY in May, up sharply from 2.4% in February and its highest level since May 2023. The Personal Consumption Expenditures (PCE) Price Index, the Fed's preferred inflation gauge, climbed to 3.8% in April, while core PCE reached 3.3%, its highest level since November 2023.

Importantly, inflationary pressures are no longer confined to energy prices alone. Core CPI, which excludes Food and Energy, increased to 2.9% in May from 2.5% before the conflict began, suggesting that higher Oil prices are gradually feeding through to other parts of the economy.

Rising inflation expectations may prove even more concerning. The University of Michigan's 1-year Inflation Expectations measure jumped to 4.6% in June from 3.4% before the conflict began, reflecting growing concerns among households that higher prices could persist for longer. Such a sharp increase raises the risk that consumers and businesses begin adjusting their behavior to a higher-inflation environment, potentially making price pressures more difficult to contain.

The Fed's latest projections underscore this challenge. While policymakers left interest rates unchanged at 3.5%-3.75% in June, they raised their inflation forecasts significantly and now expect PCE inflation to end the year at 3.6%, up from 2.7% projected in March. At the same time, the Fed only modestly lowered its growth outlook and maintained a relatively optimistic view of the labor market. The updated dot plot showed policymakers now expect interest rates to stand at 3.8% by the end of 2026, suggesting that officials remain more concerned about inflation than economic weakness.

So far, however, there is limited evidence that higher inflation is translating into stronger wage pressures. Wages grew by 0.3% MoM and by 3.4% YoY in May, suggesting that labor costs are not yet accelerating at a pace consistent with a self-reinforcing inflation cycle.

The recent decline in Oil prices could also help ease some inflationary pressure in the coming months. Following the signing of a preliminary agreement between Washington and Tehran and the gradual reopening of the Strait of Hormuz, WTI Crude has fallen by roughly 15% over the past week. While policymakers continue to warn that inflation has broadened beyond energy alone, lower fuel costs could provide some relief to households and reduce one of the main drivers behind the recent inflation surge.

US consumers are feeling the pressure, but spending remains resilient

Perhaps the most striking divergence in the US economy is the contrast between consumer sentiment and actual spending behavior. The University of Michigan Consumer Sentiment Index fell to 48.9 in June from 56.6 in February, reflecting growing frustration over higher fuel costs and rising inflation. The decline suggests that households are becoming increasingly concerned about their purchasing power and the broader economic outlook.

Yet spending data tells a very different story. Retail Sales rose 0.9% MoM in May following a 0.4% increase in April. On a yearly basis, Retail Sales accelerated to 6.9%, up from 4.8% in April and 4% before the conflict began, indicating that consumers continue to spend despite higher energy costs and elevated inflation.

Part of this resilience may reflect consumers bringing forward purchases in anticipation of further price increases. As Scott Anderson, Chief US Economist at BMO Capital Markets noted, households appear to have "moved forward some planned purchases to get ahead of any further inflationary spike due to the war." Such behavior is common during periods of rising inflation expectations, as consumers seek to avoid paying higher prices in the future.

This interpretation suggests that some of the recent strength in spending may not be entirely sustainable. If households are accelerating purchases today, consumption could weaken in the coming months as those purchases are effectively borrowed from future demand.

Other indicators point to a growing strain on household finances. Several reports note declining savings rates, rising credit card usage and increasing pressure on lower-income consumers, who are more exposed to higher food and energy costs. The Fed's Beige Book describes an increasingly "K-shaped economy," where higher-income households continue to spend relatively freely while middle- and lower-income consumers become more cautious.

For now, consumer spending remains one of the economy's main sources of support. However, it may also prove to be one of the most vulnerable areas if elevated inflation and energy prices persist through the second half of the year.

Why is the US economy holding up better than expected?

Several factors help explain why the economy has so far absorbed the shock. First, the US economy entered the conflict from a position of relative strength. Economic growth remained solid throughout 2025, providing a stronger starting point than during many previous geopolitical crises.

Second, labor market conditions remain sufficiently healthy to support household income and consumption. Third, consumer spending continues to benefit from higher-income households, which account for a disproportionate share of total expenditure and are less affected by rising gasoline prices.

Finally, strong investment linked to Artificial Intelligence remains a major source of support for economic activity. Bank of America and the Organisation for Economic Co-operation and Development (OECD) both identify AI-related capital expenditure as one of the key drivers of growth in 2026, helping offset some of the drag created by higher energy prices.

The key risks to watch in the coming months

Despite its resilience, the US economy is far from immune to the consequences of a prolonged conflict. The most immediate downside risk has eased considerably following the preliminary agreement between the United States and Iran and the reopening of the Strait of Hormuz. However, uncertainty remains high as negotiations toward a final settlement continue, and both Washington and Tehran have warned that military tensions could re-emerge if talks break down.

A second risk is that inflation may continue to erode household purchasing power. While spending has remained resilient so far, consumer sentiment indicators suggest that households are becoming increasingly uncomfortable with the higher cost of living.

The labor market also warrants close attention. Most economists agree that employment tends to react to energy shocks with a lag, meaning that the full impact may not yet be visible in current data.

Finally, a prolonged period of elevated energy costs could weigh on corporate investment, including energy-intensive sectors linked to artificial intelligence, which many analysts currently view as a critical pillar of US economic growth.

For now, the data continue to tell a surprisingly consistent story. The US economy has absorbed the Iran war far better than many economists expected, while recent diplomatic progress has reduced one of the main threats to growth. Inflation remains elevated and the labor market is gradually cooling, but the feared recessionary impact of the conflict has yet to materialize.

Whether that resilience can persist through the second half of the year will depend not only on the trajectory of inflation and employment, but also on whether the current US-Iran agreement evolves into a durable peace settlement.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.