G10 FX Week Ahead: History repeating

Investors might see history repeating itself as geopolitical tensions – with China at the centre – revived concerns about another trade war. Meanwhile, Australia has already seen the first Chinese tariffs, with AUD now bearing considerable downside risk. A defensive stance may prevail in global markets next week, with the yen and USD leading the board.

USD: US-China tension in focus again

The rally in risk assets is proving a little slower-going now that that the turn in Covid-19 curves and lock-down exit strategies have been factored in. Energy markets have certainly played a big role in asset market recoveries and again it is not clear if Brent needs to trade up to $45/bl immediately. Instead, investors are left to guess how hard President Trump is prepared to press China in a fragile election year – with the current focus on potential US sanctions in response to new national security laws in Hong Kong. This story may dominate the early part of the week - especially in the final few days of China’s National People’s Congress.

After Monday’s Memorial Day public holiday, the US calendar gets into gear with the Fed Beige, Book, the first revision to 1Q20 GDP and consumer sentiment for May. We expect the GDP release to be revised a little lower from the first -4.8% QoQ annualised print and the market to remain to look for fresh US stimulus – which may be several weeks away. On balance, DXY may test the upper bound of its recent trading ranges.

EUR: European Commission to convert EU recovery plan to action

The EUR has been finding a little more support recently, buoyed by the Merkel-Macron EU recovery plan. This coming Wednesday, the European Commission will try to convert this plan into proposed action. While there will be push-back from the more frugal members of the EU, we suspect the plan will be greeted well by markets such that 1.08 becomes a slightly stronger support level in EUR/USD.

Other events this week include German IFO on Monday and ECB Chief Economist Philip Lane speaking at an IIF virtual conference on Tuesday. On balance we think the ECB will announce a top-up to its PEPP programme at the 4 June ECB meeting and remarks from the chief economist in that direction could be seen as EUR supportive, via the fiscal risk channel.

JPY: USD/JPY stubbornly strong

USD/JPY is carving out a new 106-108 trading range and might edge lower in the week ahead if President Trump tips stock markets lower with retaliatory action against China. In the background, we wonder whether USD/JPY resilience is also being caused by USD funding issues, where Japanese banks are still drawing down $9bn in the 7-day USD swap auctions with the Fed.

In the week ahead, we’ll see Japanese data updates on Tokyo CPI, Jobs, retail sales and industrial production. They should all be pretty soft (Tokyo department store sales fell 76% YoY in April) and will keep the focus on whether Japanese authorities are doing enough to support the economy. Ultimately, we think USD/JPY breaks lower later this year, but so far there are few signs of a broader dollar bear trend emerging.

GBP: No respite for sterling

It is a very quiet week on the UK data front. With the market already pencilling in Bank of England interest rates to start turning negative by the year-end (which we still view as far from certain), the near-term negative impact from the expectations of the looser monetary policy on GBP should be now limited. The next main hurdle for GBP should be the negative news-flow on the UK-EU trade negotiations and the likely no extension of the UK-EU transition period.

As limited risk premium is priced into the GBP spot, speculative shorts not being material and the sterling implied volatility curve showing signs of complacency, the likely non-extension of the transition period and the associated negative news flow should weigh on GBP and send GBP/USD even closer to the 1.20 level by June. The upcoming weeks should be therefore associated with downside risks to GBP, hence our modestly bearish view on GBP/USD for the next week.

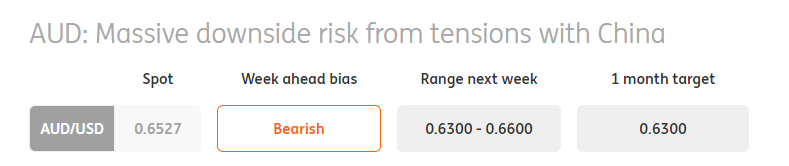

AUD: Massive downside risk from tensions with China

Australia and China have entered a diplomatic spat lately after the Australian government pushed for an investigation on the origins of Covid-19 (and possible responsibility of the Chinese government). In what many identified as retaliation, China levied tariffs on Australian barley and is reportedly working on a list of other Australian exports to potentially target with duties. If iron ore and coal were to be hit by protectionist measures, the (negative) implications for the Australian economy and the AUD would be considerable.

Markets had shown some complacency around rising tensions between China and some developed economies lately. Now, the risk of a new geopolitical turmoil and possibly a new trade war starts to be priced in and recent developments in Hong Kong may further unnerve investors. AUD still has some relatively strong fundamentals, one of which is being a good commodity backdrop thanks to extra-resilient iron ore prices, largely boosted from strong Chinese demand.

However, rising Australia-China tensions mean that AUD now bears a big deal of downside risk (and may get quite volatile), which likely puts it at the bottom of the G10 commodity currencies rank in a risk-reward perspective.

NZD: Watch for Aussie-China spat spill-over

New Zealand is not directly involved in the diplomatic tensions between Australia and China, but NZD is still set to suffer if the spat escalates towards a trade war, due to its strong ties to both countries. In turn, we could see NZD/USD push the 0.60 psychological support next week if the situation fails to defuse.

The larger idiosyncratic risks for Australia suggest NZD may outperform AUD in the near term, with AUD/NZD giving up some of the recent gains, edging back towards 1.05. Incidentally, the NZD is facing less downward pressure from the RBNZ after Governor Orr downplayed negative rates as an imminent policy measure. He will speak next week (otherwise, nothing else to note on the calendar) as the Bank publishes the financial stability report.

CAD: Monitoring oil's reaction function

CAD slightly depreciated over the past week as risk sentiment took a toll with escalating geopolitical tensions. Markets may remain on a defensive stance next week as such tensions linger and we may see some pressure added to the loonie. What matters the most for CAD, however, is whether this will trigger a material correction in oil prices or if crude keeps showing some resilience. In general, WTI at a more sustainable level is already providing some shelter to CAD, which now appears in a much better position compared to its peers AUD and NZD, due to the tensions between Australia and China.

Data-wise, we’ll see March GDP data coming out next week. Our economics team is expecting a sharp contraction in Q1 (-7.5% QoQ) while showing a -4% YoY drop in March. This may put some additional pressure on CAD towards the end of the week, although the limited explanatory power about the implications of lockdown measures (which have become more evident in Q2) on the economy likely suggests a short-lived impact on the loonie. On the central bank side, keep an eye on two speeches by Governor Stephen Poloz next week.

CHF: Bear market bounce in EUR/CHF

Momentum towards an EU recovery fund and what it means for Italian debt servicing costs have allowed EUR/CHF to bounce off 1.0500. A positive performance from the European Commission this week in providing details on how such a plan could work would also be greeted well by EUR/CHF. However, EUR/CHF is not just an Italian debt story, but also one governed by the ECB printing presses. We think the SNB will struggle to match ECB balance sheet expansion this year and EUR/CHF breaks 1.05 at some point.

Away from Wednesday’s European Commission update, the Swiss calendar sees industrial output, exports and the KOF leading indicator on Friday. A weak bounce back is expected in the KOF, but we still look for a full year Swiss contraction of more than 6% in 2020.

NOK: Weighed down by oil, for now

The likely limited near-term upside to oil prices (due to the mix of concerns about the US-China relations and its effect on risk sentiment, and what looks like an exaggerated rise in Brent oil price, out of sync with its near-term oil fundamentals) points towards a limited scope for EUR/NOK decline. EUR/NOK to stay around / modestly below the 11.00 level.

It is a fairly quiet week on the Norwegian data front. 2Q consumer confidence due on Tuesday and April retail sales due on Wednesday and should have a limited impact on the currency. Of interest will be the publication of NB FX purchases (Friday) which picked up materially as the NB is buying NOK / selling foreign currencies (from the liquidation of the oil fund assets denominated in foreign currencies) to fund the rising domestic fiscal deficit. Beyond the near-term market jitters, this means NOK stands out among G10 currencies as the central bank is helping to navigate the government’s rising spending not via the QE, but via the purchases of domestic currency.

SEK: Potential G10 cyclical outperformer next week

It is a busy week on the Swedish data front. May Economic Tendency Survey out on Thursday, April retail sales also due on Thursday and 1Q GDP due on Friday. But the overall effect on SEK should be limited as the spillover into monetary policy should be muted. The Riksbank seems unwilling to move interest rates back into the negative territory and QE has been already expanded.

Should oil and commodity prices remain under pressure next week, SEK is likely to outperform its G10 cyclical peers, benefiting from its lack of exposure to commodity prices (vs NOK, CAD, AUD and NZD), while it now also exerts the second-highest real rate within the wider G10 FX space (only very modestly surpassed by CAD).

Read the original analysis: G10 FX Week Ahead: History repeating

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.