US disinflation could be drowned out by European politics

Were it not for events in Europe, FX markets would now be focusing on the welcome disinflation in the US and the prospects of a softer dollar. As it is, President Macron’s gamble has added some unexpected volatility into European currencies - likely to keep risk appetite in check. If the dollar is to go lower, it will be non-European currencies that prosper.

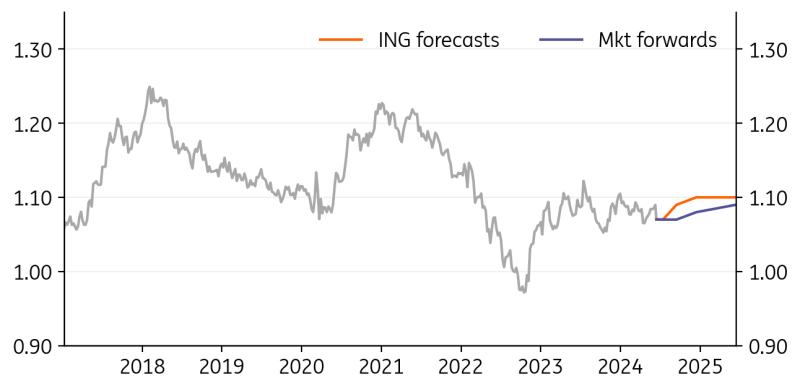

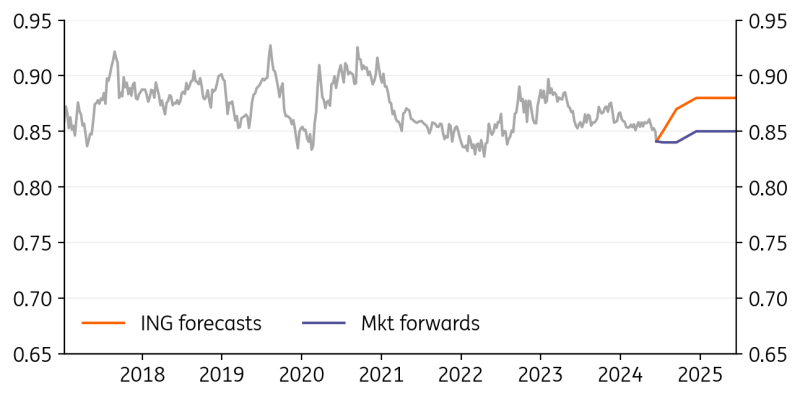

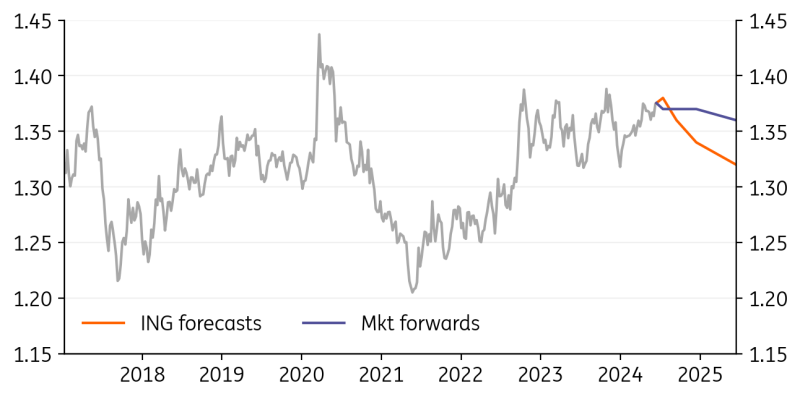

EUR/USD: Fed convergence trade faces French politics

-

It has been a struggle, but it is starting to look like investors are swinging behind Federal Reserve rate cuts this year. US May CPI and PPI price data are showing encouraging signals and point to another low print for the Fed’s preferred price gauge – core PCE - when it is released on 28 June. We think there is plenty of room for US short-dated yields to fall – a clear dollar negative.

-

EUR/USD may not be able to take advantage of the softer dollar. French elections on 30 June / 7 July and the risk of a Le Pen-led government at loggerheads with the European Commission over spending plans creates risks for the French bond market.

-

These will be the two themes dominating ahead of US elections.

Source: Refinitiv, ING forecasts

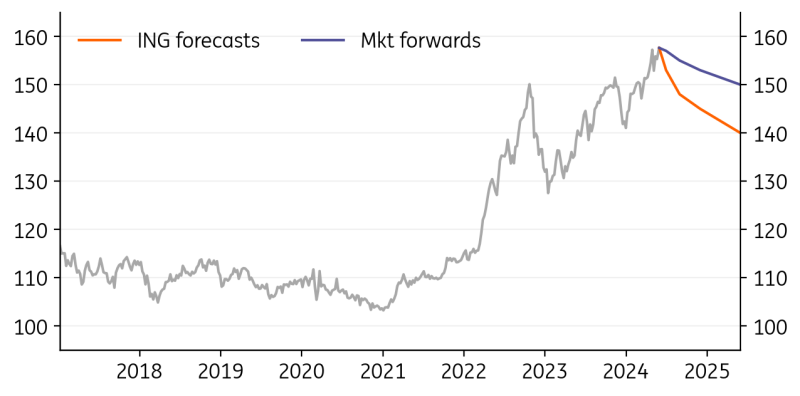

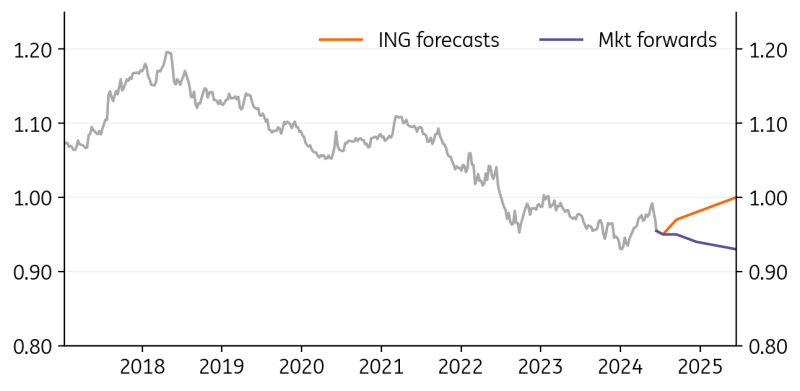

USD/JPY: The Yen is not a compelling sell

-

It was confirmed that the Bank of Japan sold around $62bn of FX around the end of April near the 160 area. Most economists view this as a waste of valuable assets in what will be an ineffective move. We see it at as: i) the BoJ injecting more two-way risk into FX markets and ii) a likely view from Tokyo that US rates will turn lower later this year. A similar thing occurred in Sep/Oct 2022.

-

We expect the BoJ to hike rates again at the late July meeting and announce a gradual reduction in its JGB buying plan.

-

We doubt the BoJ’s move will turn USD/JPY lower, but we do favour lower US rates and higher FX volatility, which are bearish factors for USD/JPY.

Source: Refinitiv, ING forecasts

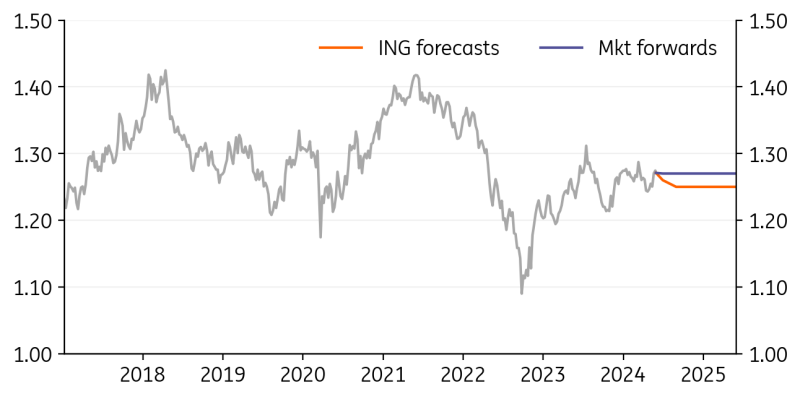

GBP/USD: Short-lived gains

-

Some softer US data plus sticky April UK CPI has pushed GBP/USD to the highs of the year. Despite ING’s call for a Fed rate cut starting in September, we think GBP/USD comes lower. This is entirely based on the view that UK CPI follows US CPI lower – giving the Bank of England enough information to start cutting rates in August. We look for three BoE rate cuts this year.

-

The trigger for that BoE rate repricing may come as soon as 19/20 June. On the 19th, we’ll see May CPI, where services should drop to 5.2% year-on-year from 5.9%. A day later, the BoE’s policy statement should hint strongly at an August rate cut.

-

We doubt UK elections 4 July will have a big bearing on sterling.

Source: Refinitiv, ING forecasts

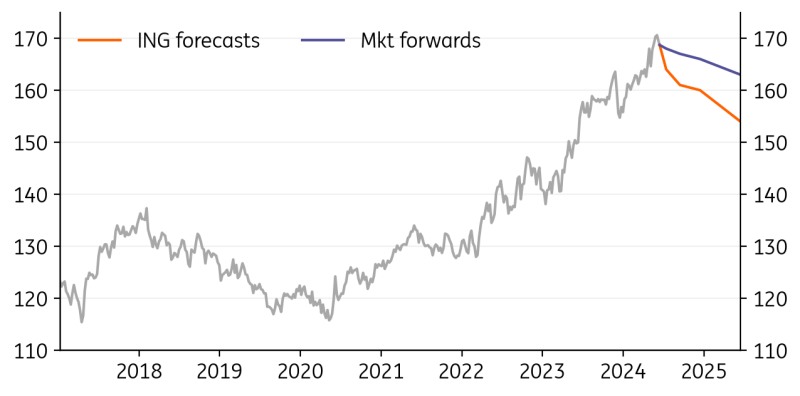

EUR/JPY: French debt will be the focus this month

-

Looking more closely at French political risk we see that French government bonds are the focal point of stress. The fears are that Le Pen could perhaps do a ‘Liz Truss’ (unfunded tax cuts which crashed the UK bond market in 2022.) These fears will not be resolved for a while and at least not before 7 July, which marks the second round of the French elections.

-

There is not a lot eurozone policymakers can do to address this. Should the French bond market sell off, the European Central Bank could try to use its new Transmission Protection Instrument to help.

-

Yet that scheme requires France not to be under an excessive deficit procedure. That may not be the case after a decision on 19 June.

Source: Refinitiv, ING forecasts

EUR/GBP: BoE versus French elections

-

EUR/GBP has broken below big support at 0.8500. The driver has been a combination of UK interest rates staying firm and now French political risks. 19 June could be a big day. We get to see the May UK CPI (downside risks to sterling) but this could also be the day that the European Commission puts France under an Excessive Deficit Procedure.

-

We estimate that the euro call fall another 1% if the political risk premium builds. We have greater confidence though in UK rates softening and EUR/GBP being dragged back above 0.8500.

-

Currently, it looks like the UK Labour party could secure a landslide win on 4 July. Fiscal risks look contained.

Source: Refinitiv, ING forecasts

EUR/CHF: Close call for the SNB policy meeting on 20 June

-

EUR/CHF volatility has picked up as spot has fallen sharply from 0.9930. Driving that move at first was the sense that the Swiss National Bank was a little concerned that the franc was falling too fast. President Thomas Jordan said a weaker CHF was the biggest risk to inflation. And then French politics hit.

-

The market is now split on whether the SNB cuts rates 25bp to 1.25% on 20 June. The case for the cut is that core inflation remains very low at 1.2% YoY. The case against is that the SNB is not sounding as dovish as it once was and is in no hurry.

-

It looks like we’ll see a 0.96-0.99 range now, with the SNB using FX intervention on both sides of the market.

Source: Refinitiv, ING forecasts

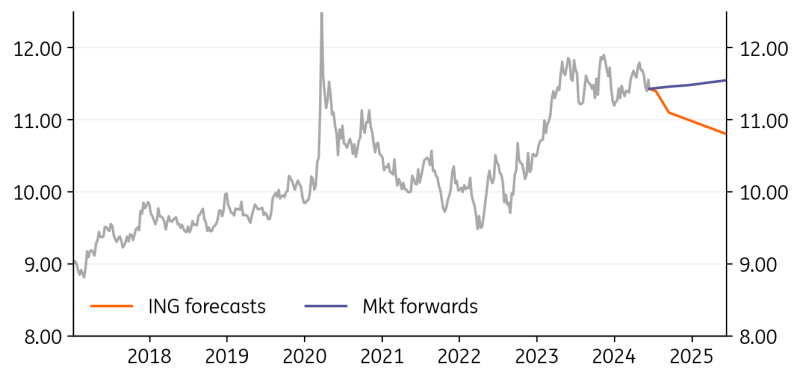

EUR/NOK: A major winner in the risk-on rally

-

The Norwegian krone remains uniquely positioned to benefit from more drops in USD rates and improvements in risk sentiment. The chances of a move below 11.30 this summer have increased after the latest US CPI report.

-

We currently have two rate cuts pencilled in by Norges Bank this year, although that primarily depends on our call for three Fed cuts. Norges Bank has remained hawkish and that should not change until the Fed starts easing.

-

There are some risks for NOK on the horizon: we suspect that markets will start to trade increasingly on the back of US election expectations after the summer, and NOK may be one of the major underperformers in a Trump victory scenario.

Source: Refinitiv, ING forecasts

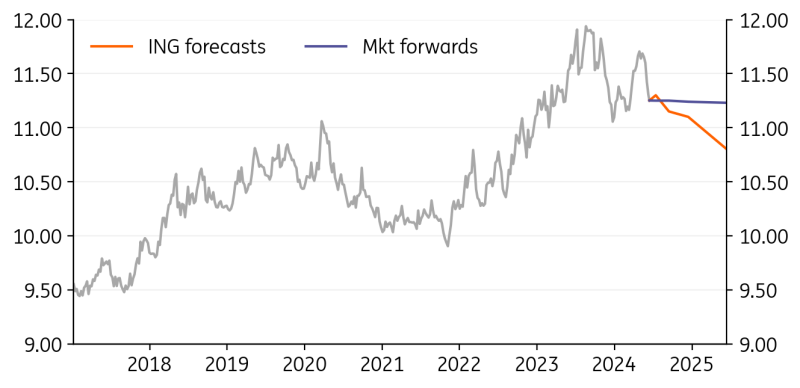

EUR/SEK: Krona may have rallied too fast

-

It is not news that global macro developments (especially in the US) are a much bigger driver of Sweden’s krona than domestic factors. However, the outperformance of SEK over other high-beta currencies does not look likely to last, in our view.

-

Disinflation halted in May but may well resume in the coming months in Sweden. Now that SEK is stronger, the Riksbank has more flexibility to cut rates. Our expectations are for 75bp of easing by year-end, more than market’s 50bp.

-

If we are right and the Fed cuts three times too, EUR/SEK should be able to stay capped. This summer, there is a chance we see sub-11.00 levels, although we are less constructive on SEK in 4Q.

Source: Refinitiv, ING forecasts

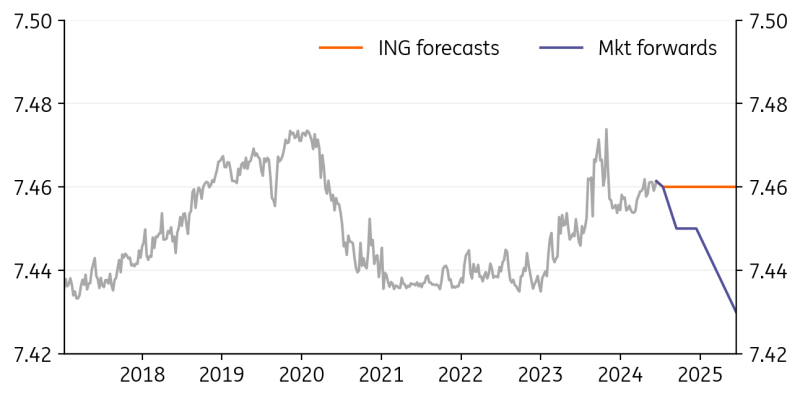

EUR/DKK: Denmark starts easing

-

Danmarks Nationalbank followed the ECB with a 25bp rate cut in June. We currently estimate two more cuts in the eurozone and Denmark by the end of the year.

-

Danish policymakers will need to acknowledge a higher inflation outlook and tighter jobs market, but the stabilisation of EUR/DKK around its central peg rate of 7.460 means policy divergence from the ECB remains unlikely.

-

We also doubt FX intervention will be revamped any time soon, and we continue to forecast EUR/DKK flat at 7.46 in the coming quarters.

Source: Refinitiv, ING forecasts

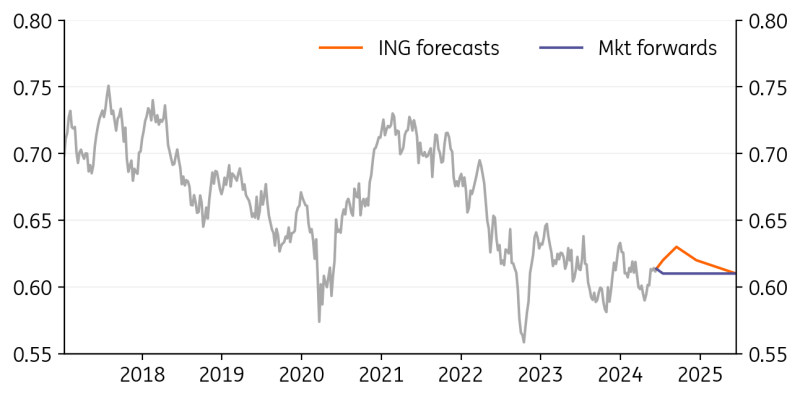

USD/CAD: Looking trapped

-

The Bank of Canada rate cut in June will – in our view – be followed by 75bp in 2H24. This is more than the market’s current pricing for 60bp, and means that we still expect the Canadian dollar to underperform other commodity currencies.

-

USD/CAD looks trapped in a relatively tight range, as the loonie tends to underperform when US data come in soft. When adding BoC easing, the weaker USD effect is largely being offset.

-

This summer could still see a gradual move lower in USD/CAD as the USD downtrend becomes more dominant. But don’t expect the loonie to do any better than other high-beta currencies. On the flipside, CAD faces less US election-related downside risks further down the road.

Source: Refinitiv, ING forecasts

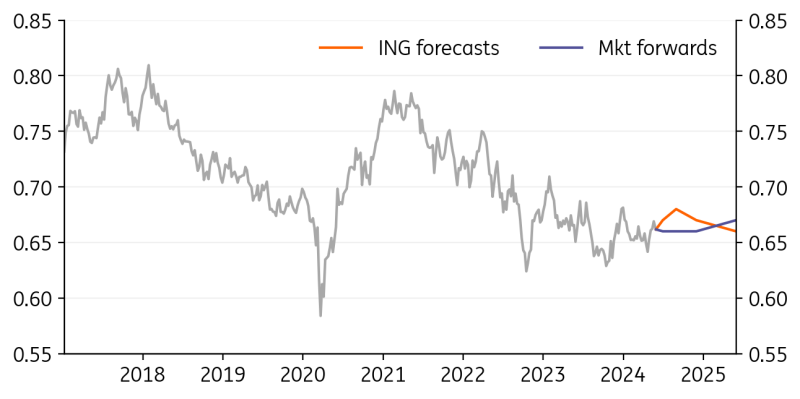

AUD/USD: Inflation to keep RBA hawkish

-

The Reserve Bank of Australia continues to have an inflation problem. Monthly CPI figures beat expectations again in the April print, rising to 3.6% YoY. While the RBA shouldn’t hike again, they may raise the threat of more tightening if needed at the 18 June meeting.

-

Markets are pricing in 11bp of RBA easing by year-end, which is largely a function of Fed expectations. We recently changed our forecasts to no cuts this year.

-

This hawkish domestic narrative is a positive for the Aussie dollar, and we still like the chances of more AUD gains (above 0.67) this summer before US election risk starts to creep in.

Source: Refinitiv, ING forecasts

NZD/USD: RBNZ still awaiting key data inputs

The 10 July Reserve Bank of New Zealand meeting should not be a huge event. The only extra bit of data available to policymakers will be 1Q GDP (quarter-on-quarter growth expected to inch back above zero), which should not move the needle dramatically from a policy perspective.

The Kiwi dollar will remain primarily driven by external factors and in our view can have a good summer, in line with our AUD view. Domestic factors remain supportive.

Once 2Q inflation and jobs data are released (July and August), a clearer path for the RBNZ should emerge. We suspect there will not be enough in the data to justify a 3Q cut, and we only expect easing to start in 4Q.

Source: Refinitiv, ING forecasts

Read the original analysis: G10 FX talking: US disinflation could be drowned out by European politics

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.