FX Update – USD Index 5-month low

USD/JPY, EUR/USD, H1

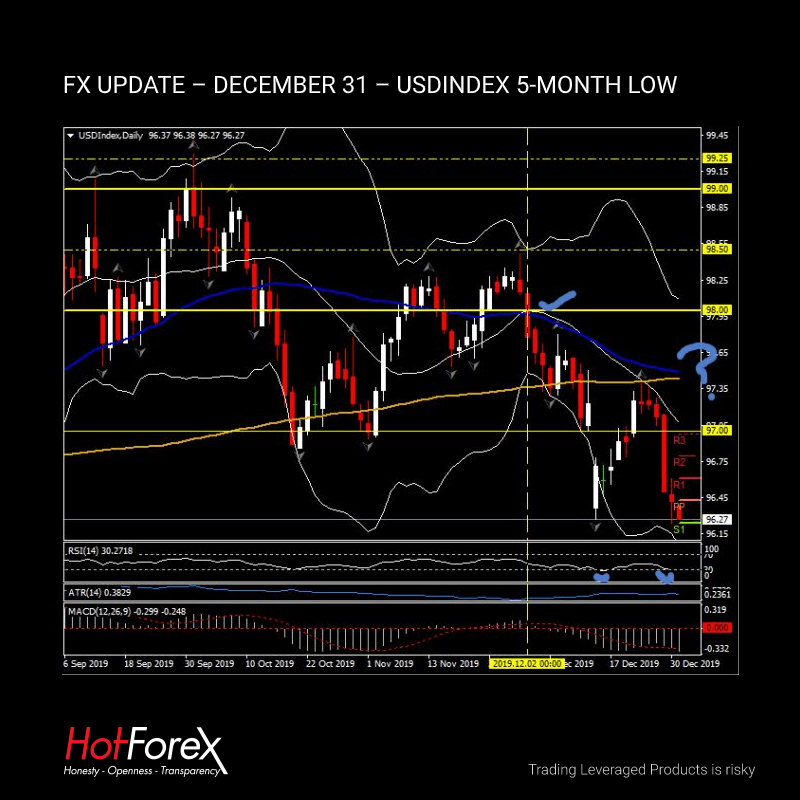

The Yen, other Asian currencies, and Dollar block units have rallied following above-forecast manufacturing PMI data out of China. USDJPY fell to an 18-day low at 108.59. AUDUSD posted a fresh one-month peak at 0.7012, in what is now the pair’s fifth consecutive up week, and NZDUSD also made a new five-month peak, with the pair amid its sixth straight up week. USDCAD fell to a fresh five-month low, at 1.3025, in what is now sixth consecutive down week the pairing has seen. The USDIndex closed yesterday (December 30) at its lowest level (96.42) since July 18 and currently trades down again at 96.31. It has been a weak month for the USDIndex with the initial move lower triggering December 2 and the break of the 20-day moving average, followed by the key 200-day moving average breach on December 11 and then the gap lower December 13. The 200-day moving average proved strong resistance to any recovery before the December 13 low was breached again yesterday. Is this simply end of year balancing on low volumes or a move to a new lower paradigm fro the USD? Only time will tell we move into 2020.

Overnight, China’s official manufacturing PMI for December came in at 50.2, a tad up on the median forecast for 50.1, and unchanged from the month prior. This offset a slight miss in the services PMI (and with the Chinese service-sector performance being off lesser interest to markets than the performances of the dominant manufacturing sector). Of note was the first above-50.0 reading in manufacturing new export orders for the first time in 18 months (the duration of the trade war with the US). With the US and China expected to sign-off on their phase-1 trade deal in the coming weeks, the data was a tonic, at least for currencies, with stock markets sputtering after recent strong gains.

Elsewhere, EURUSD has been trading on either side of 1.1200 since making a four-month high yesterday at 1.1220, but remains biased to the upside. Cable also remained below the high seen yesterday. The UK’s Telegraph newspaper cited Phil Hogan, the new EU trade commissioner, predicting that Prime Minister Johnson will renege on his self-imposed legal commitment to exit the Brexit transition period by the end of 2020. Hogan drew attention to Johnson’s high profile pledge to “die in a ditch” rather than let Brexit be extended beyond October. The Classics Oxford alumni PM is renowned for his flowery language, however with 11 only months to go I tend to concur with Mr Hogan.

The key data point of note today is the US Consumer Board’s Consumer Confidence Index (15:00 GMT) report which is expected to rise to 128.5 in December, after falling -0.6 ticks to a 5-month low of 125.5 in November. All of the weakness last month was in the present situation index, which is expected to rebound to 168.0 from 166.9 in November. The expectations index should rise to 103.0 in December from 97.9 previously. Despite various headwinds, the confidence measures remain historically high, and there has been an updraft in the various consumer confidence measures this month thanks to reduced uncertainties over trade and the end of the UAW strike. The lift may gain steam with late-month responses given the positive news flow on trade, as well as the rally in the equity markets.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c