FX outlook 2024: Our main calls

2024 should be the year US exceptionalism wanes and currencies outside of the US are allowed to refloat.

The Dollar’s long goodbye

This time last year we were forecasting fewer trends in global FX markets and more volatility. In fact, 2023 has proved a year of two halves: the first half more trendless and the second half characterised by a very orderly and powerful dollar bull trend.

This dollar rally has been built on the exceptionalism of the US economy – registering an incredible growth rate of 4.9% quarter-on-quarter annualised in the third quarter. And despite headline inflation dipping, there is really not enough evidence, yet, for the Fed to drop its hawkish guard. Holding dollars has therefore become the ‘no-brainer’ trade as investors price slowing aggregate demand globally – a theme that has weighed on the more open economies and currencies of Europe and Asia.

Will this theme continue into 2024? It feels like a wrestling match and the dollar will not roll over that easily. Yet our simple thesis is that tighter interest rates finally catch up with the US economy next year, growth registers a paltry 0.5% and the Fed, in line with its dual mandate to focus on inflation and maximum employment, cuts rates back into less restrictive territory. We forecast 150bp of Fed easing next year starting in the second quarter.

The end of US exceptionalism will allow greater diversification amongst the investor community and a lower bar to seek returns outside of the dollar. Portfolio capital can refloat some of those stranded non-dollar currencies.

In advance of the first Fed cut, we would expect the US yield curve to start a bullish steepening trend. This is a particular segment in the business cycle that favours a weaker dollar and is bullish for commodity currencies. It just so happens that some of the commodity currencies are incredibly undervalued based on our medium-term fair value model. This is the area of the FX market in which we see the most value. Or at least the commodity currencies are offered some protection by their extreme undervaluation, whereas the euro and sterling have no such support.

A lower US rate environment should also allow the recovery of what we term ‘growth’ currencies – similar to growth stocks such as tech and real estate. We consider the Swedish krona one such currency.

Our baseline view for 2024 therefore sees the dollar bear trend picking up pace through the year. Compared to year-end 2024 forwards, currencies could be as little as 2% (China’s renminbi) to as much as 13% (Scandinavian FX) firmer against the dollar.

FX Outlook 2024: Waiting for the tide to come in

ING forecasted performance versus year-end 2024 USD forwards

Source: ING, Refinitiv

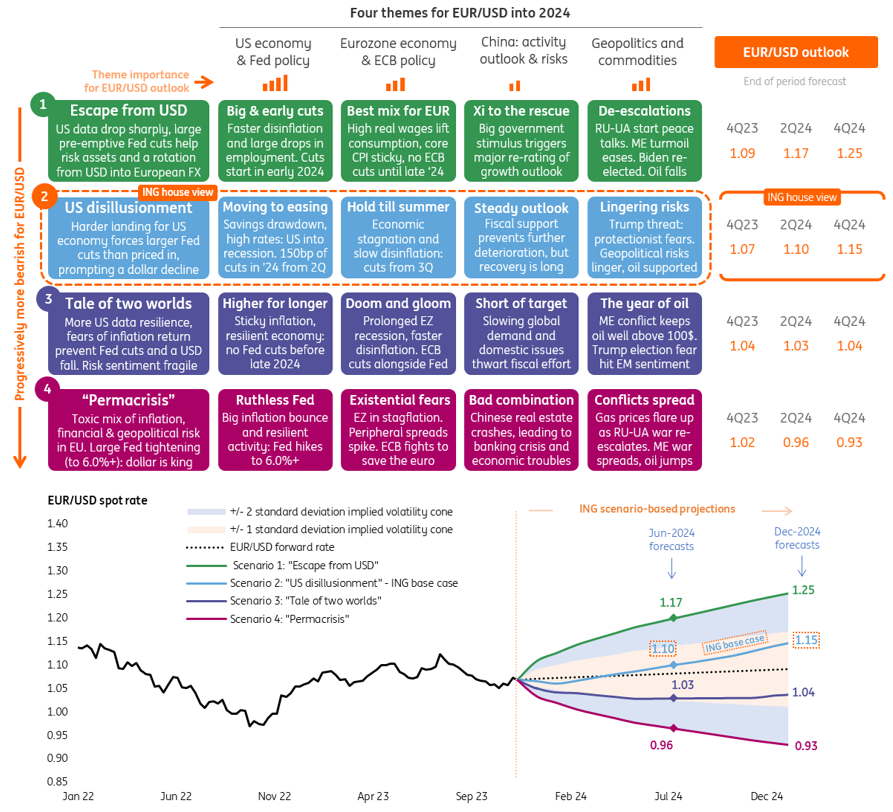

The above forecasts of course are built on many core assumptions. Using the most liquid FX pair, EUR/USD as the benchmark for the FX market in general, we see a range of outcomes in the 0.88 to 1.21 region.

If you think US inflation will not allow the Fed to cut, if you think a local recession and return of the Maastricht criteria sparks a eurozone crisis, if you think President Trump is elected on an even louder anti-China ticket and if you think tensions in the Middle East escalate into a major energy supply shock – then EUR/USD can plumb the depths.

If, however, like us you think that the Fed is allowed to deliver an orderly easing cycle and that soft landings are seen in Europe and China, then EUR/USD could be somewhere near our 1.15 baseline forecast by end-2024.

We now invite you to take a look through our G10, EMEA, ASIA and LATAM sections for insights into key local factors, such as elections, the fiscal-monetary mixes and also the FX preferences of the local authorities – all of which will shape FX trends next year.

EUR/USD: Four potential paths for the next quarter

Source: ING

Read the original analysis: FX outlook 2024: Our main calls

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.