Fuzzy Math on Fiscal Policy

Keeping score is sometimes a difficult thing. Millions of Americans cheered when bowling alleys mercifully automated the accounting for strikes, spares and splits. Tennis confuses some people: why are the first and second points in a game worth 15 and the third worth 10? With tallies above the line and below the line, bridge makes it hard to get to the bottom line.

But all these pale in comparison to the challenge of projecting the bottom line in a public budget. Economic trends and economic policies, which are difficult to evaluate, drive revenues and expenses. Past patterns may not bfe a good guide to future performance, and there are countless interdependencies among variables. In a sense, fiscal projections are a nexus for the horrors forecasters face.

Nonetheless, these exercises are critically important. Can we afford a tax cut? Will a massive infrastructure program pay for itself? How long will it be before entitlement programs run out of money? The answers to all these weighty questions rest on some very fuzzy math.

There are two stages to fiscal forecasting. The first is establishing a baseline, which depicts the most likely path of inflows and outflows using policies currently in effect. The process requires a series of economic assumptions, which are not easy to establish.

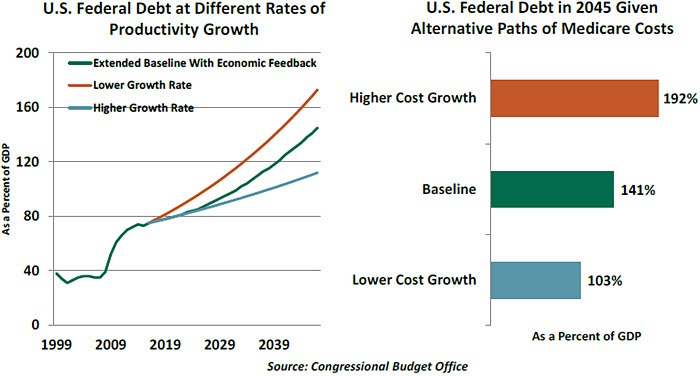

One of the more critical is the rate of productivity growth. Higher productivity growth tends to increase output without stressing inflation, both of which are favorable to national budgets.

Productivity has been disappointing in developed markets over the past decade, and there are alternative schools of thought about where it might be heading from here. As shown in the chart above, U.S. finances will hinge critically on this evolution. The same is true for many other countries.

Another key assumption is the growth rate of health care expenses. With aging populations living longer and taking advantage of advanced medical care, public costs will be escalating. Given the size of the numbers involved, modest changes in the growth rate of medical bills will have a substantial influence on fiscal solvency.

Believe it or not, setting a baseline is the easy part of the budgeting exercise. The challenges for forecasters increase as we move to the second phase: evaluating how policy changes might affect the outcome. Calculating the impact of proposed measures on public budgets is referred to as “scoring.”

Believe it or not, setting a baseline is the easy part of the budgeting exercise. The challenges for forecasters increase as we move to the second phase: evaluating how policy changes might affect the outcome. Calculating the impact of proposed measures on public budgets is referred to as “scoring.”

Oftentimes, measures are scored simply on the direct impact they have on revenue or spending. Under this “static” rubric, a tax cut would be viewed as increasing the deficit. But the hope of those who support lower taxes is that such a policy would generatef increased levels of economic growth, broadening the tax base and producing additional revenue.

In an attempt to capture these effects, “dynamic” scoring can be used. The dynamic part refers to after-effects that might be captured to make the analysis more comprehensive, such as the favorable impact of lower taxes on economic growth. The case for a more interactive approach can be found here.

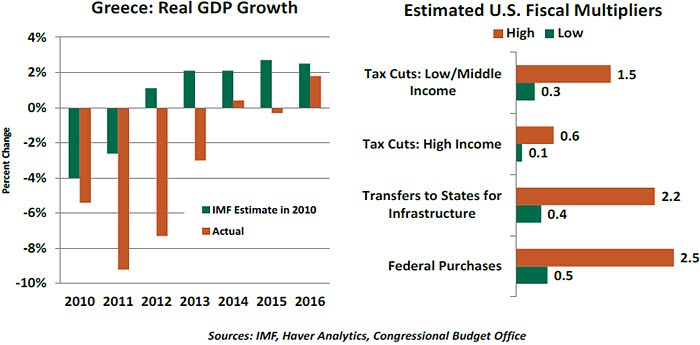

Dynamic scoring might certainly beneficial to Greece (discussed at length in our second piece). The reform program designed for the country seemed to underestimate the deleterious effect that budget cuts would have on growth, leading to a painful contraction that ultimately made matters worse.

Dynamic scoring might have revealed that austerity that is too extreme damages the tax base to a point that hinders the quest for budget balance. This is something that deserves consideration as Greece heads back to bargaining with its creditors.

While theoretically meritorious, performing dynamic scoring is extraordinarily difficult. For example, if taxes are cut, the heightened level of activity could threaten to become inflationary. In that event, the central bank might tighten monetary policy to cool things down, which would restrain the economy and tax collections. Slower growth might prompt higher unemployment, which might prompt the central bank to ease, and so on. The circular relationship between economic variables makes analyzing policy changes challenging.

Even with a full inventory of causes and effects, calculating their magnitudes is very difficult. The science (if it can be called that) focuses on “fiscal multipliers,” which relate the cost of a policy to the amount of economic activity it generates. A fiscal multiplier of more than one signifies the program generates incremental output that exceeds its cost. (It should be noted that this is not the same as saying that the program “pays for itself,” since incremental tax revenue is far less than incremental national income.)

Models that estimate fiscal multipliers have a large margin of error, and different models may come up with vastly different conclusions. There is also concern that an analyst’s political leanings may steer the assumptions used to evaluate policies dynamically. Even the U.S. Congressional Budget Office, which purports to be nonpartisan, has been criticized in some corners for allowing bias to creep into its studies.

Models that estimate fiscal multipliers have a large margin of error, and different models may come up with vastly different conclusions. There is also concern that an analyst’s political leanings may steer the assumptions used to evaluate policies dynamically. Even the U.S. Congressional Budget Office, which purports to be nonpartisan, has been criticized in some corners for allowing bias to creep into its studies.

Opponents of dynamic scoring cite this uncertainty as a reason to continue with the simpler approach. But it seems clear that a myopic view produces bad policy. We’ll need to exercise discipline around dynamic scoring, but it seems like the best way to go.

Many governmental entities around the world are being challenged to establish their long-term solvency. Getting the scoring right will be essential to the integrity of these efforts. This is no game; world markets have a lot riding on the outcome.

Editor’s note: “Fuzzy Math” is a refreshed version of an essay that appeared two years ago. With government budget issues at the forefront in the world today, an encore seemed warranted.

Ongoing Drama

Greece may no longer be on the list of top risks to the global markets, but the travails of the Greek economy are far from over. Unemployment remains unconscionably high at 23%. The economy has only just emerged from three years of deflation and real gross domestic product (GDP) remains more than a quarter below its pre-crisis peak.

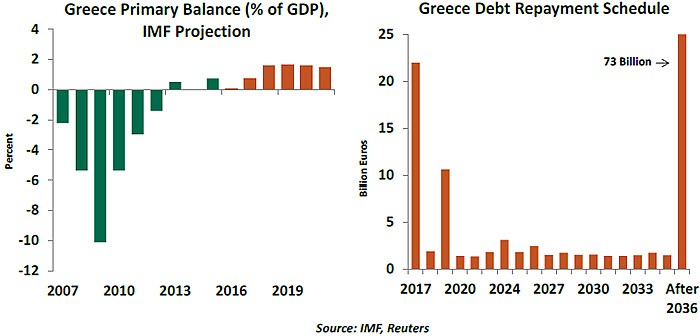

Public debt in Greece is at a level that is not sustainable. The International Monetary Fund (IMF) has urged debt relief, while European creditors (primarily Germany) have counseled austerity. The fate of the next phase of the €87 billion Greek bailout will depend on the reconciliation of these two perspectives.

There is even a difference of opinion on the current state of Greek public finances, with the IMF projecting a near balance (fiscal balance excluding interest payments) and other debtors estimating a primary surplus of up to 1% of GDP for 2016. Key here is the assumption of the fiscal multiplier, and the IMF expects the fiscal tightening to be much more contractionary. If the IMF’s growth and deficit projections find the debt to be unsustainable, it would no longer participate in the bailout.

The IMF is concerned about the viability of asking Greece to run annual primary budget surpluses to the tune of 3.5% of GDP, which is mandated by the current program. At the same time, the IMF is frustrated at the lack of progress toward “growth-enhancing” structural reforms in Greece by the government of Prime Minister Tsipras.

With elections coming up, governments in the Netherlands and Germany want to keep the IMF on board and avoid debt relief, lest they give an impression of going easy on the Greeks. An optimistic fiscal projection allows European leaders to keep the IMF involved in the program while preserving the right to blame Greece if targets go unmet.

The only common ground between Europe and the IMF is the need to dictate future spending cuts up front. The Greek government wants so much to avoid this that it is willing to give up on its demand for debt relief. Its immediate target is to secure a successful conclusion of the second review by the Eurogroup meeting on the 20th of February, even if the IMF refuses to participate. A successful review should mean that Greece’s debt repayment obligations are met and its debt is considered sustainable by the European institutions. Greek debt might then become eligible for purchase by the European Central Bank under its quantitative easing program.

The only common ground between Europe and the IMF is the need to dictate future spending cuts up front. The Greek government wants so much to avoid this that it is willing to give up on its demand for debt relief. Its immediate target is to secure a successful conclusion of the second review by the Eurogroup meeting on the 20th of February, even if the IMF refuses to participate. A successful review should mean that Greece’s debt repayment obligations are met and its debt is considered sustainable by the European institutions. Greek debt might then become eligible for purchase by the European Central Bank under its quantitative easing program.

There is some urgency to this process. 2017 could shift the political center further away from the EU in Berlin, Paris and the Hague, something that will make its governments even less willing to give concessions to the Greeks. At the same time, a non-deal would complicate matters with a crisis-weary electorate.

To complicate matters further, there is a reasonable chance of the Greek government calling for fresh elections if it is forced to adopt more painful reforms and spending cuts in return for new funding. Given that the Tsipras government would most certainly lose, new elections would be either “anti-austerity” political grandstanding or a bargaining chip with European governments that would rather avoid another Greek crisis while they seek reelection at home. Overall, with so many pieces needed to fall in place for a successful continuation of the current bailout program, a re-run of the 2015 crisis should not be ruled out.

The Challenge of Shrinking the Fed’s Balance Sheet

This year, in addition to the customary market concern about the path of interest rates, a hot conversation topic is when the U.S. Federal Reserve (Fed) will pare back its holdings of Treasury and mortgage-backed securities. The Fed’s balance sheet increased nearly five-fold as a result of its actions following the global financial crisis.

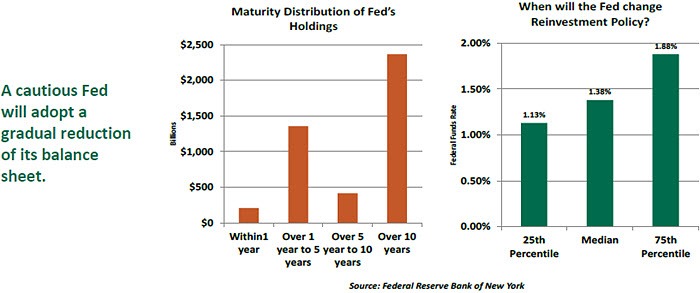

Of the Fed’s $4.4 trillion balance sheet, Treasury securities (56%) account for a significant share, with mortgage-backed securities (39%) following closely behind. The Fed stopped purchases of assets in October 2014 and since then has been replacing maturing securities to maintain the balance sheet level.

In December 2015, the Fed indicated that reinvestment of the securities portfolio would continue until “normalization of the level of the federal funds rate is well underway.” This statement does not indicate when precisely the Fed will stop reinvesting. A good proxy is the response of primary dealers to the New York Fed’s December survey asking for their expectations for the federal funds rate “when the Committee first changes its reinvestment policy” and the month they forecast the change to occur. The dealers’ median responses were 1.38% for the policy rate and June 2018 on timing.

In the past few weeks, Fed officials have offered their views about the balance sheet. These developments suggest the Fed is perfecting its views in preparation for changing strategy. Former Fed Chairman Ben Bernanke offered his thoughts on appropriate timing here.

Sustained expansion should expedite the termination of the current reinvestment policy. The Fed will have to choose between a gradual reduction in reinvestment or a complete termination. There are benefits to shrinking the balance sheet instead of raising the policy rate. Such an action might tend to weaken the dollar, which could spur exports and boost factory activity. In the global context, a depreciation of the dollar would reduce pressures on countries with fixed exchange rates and external debt.

Our view is that the 2013 “Taper Tantrum” event is etched in the memory of Fed officials and there is no appetite for another such episode. The Fed will want to be especially sure of its timing and will endeavor to provide enhanced communication to minimize market turbulence.

But all these pale in comparison to the challenge of projecting the bottom line in a public budget. Economic trends and economic policies, which are difficult to evaluate, drive revenues and expenses. Past patterns may not bfe a good guide to future performance, and there are countless interdependencies among variables. In a sense, fiscal projections are a nexus for the horrors forecasters face.

Nonetheless, these exercises are critically important. Can we afford a tax cut? Will a massive infrastructure program pay for itself? How long will it be before entitlement programs run out of money? The answers to all these weighty questions rest on some very fuzzy math.

There are two stages to fiscal forecasting. The first is establishing a baseline, which depicts the most likely path of inflows and outflows using policies currently in effect. The process requires a series of economic assumptions, which are not easy to establish.

One of the more critical is the rate of productivity growth. Higher productivity growth tends to increase output without stressing inflation, both of which are favorable to national budgets.

Productivity has been disappointing in developed markets over the past decade, and there are alternative schools of thought about where it might be heading from here. As shown in the chart above, U.S. finances will hinge critically on this evolution. The same is true for many other countries.

Another key assumption is the growth rate of health care expenses. With aging populations living longer and taking advantage of advanced medical care, public costs will be escalating. Given the size of the numbers involved, modest changes in the growth rate of medical bills will have a substantial influence on fiscal solvency.

Oftentimes, measures are scored simply on the direct impact they have on revenue or spending. Under this “static” rubric, a tax cut would be viewed as increasing the deficit. But the hope of those who support lower taxes is that such a policy would generatef increased levels of economic growth, broadening the tax base and producing additional revenue.

In an attempt to capture these effects, “dynamic” scoring can be used. The dynamic part refers to after-effects that might be captured to make the analysis more comprehensive, such as the favorable impact of lower taxes on economic growth. The case for a more interactive approach can be found here.

Dynamic scoring might certainly beneficial to Greece (discussed at length in our second piece). The reform program designed for the country seemed to underestimate the deleterious effect that budget cuts would have on growth, leading to a painful contraction that ultimately made matters worse.

Dynamic scoring might have revealed that austerity that is too extreme damages the tax base to a point that hinders the quest for budget balance. This is something that deserves consideration as Greece heads back to bargaining with its creditors.

While theoretically meritorious, performing dynamic scoring is extraordinarily difficult. For example, if taxes are cut, the heightened level of activity could threaten to become inflationary. In that event, the central bank might tighten monetary policy to cool things down, which would restrain the economy and tax collections. Slower growth might prompt higher unemployment, which might prompt the central bank to ease, and so on. The circular relationship between economic variables makes analyzing policy changes challenging.

Even with a full inventory of causes and effects, calculating their magnitudes is very difficult. The science (if it can be called that) focuses on “fiscal multipliers,” which relate the cost of a policy to the amount of economic activity it generates. A fiscal multiplier of more than one signifies the program generates incremental output that exceeds its cost. (It should be noted that this is not the same as saying that the program “pays for itself,” since incremental tax revenue is far less than incremental national income.)

Opponents of dynamic scoring cite this uncertainty as a reason to continue with the simpler approach. But it seems clear that a myopic view produces bad policy. We’ll need to exercise discipline around dynamic scoring, but it seems like the best way to go.

Many governmental entities around the world are being challenged to establish their long-term solvency. Getting the scoring right will be essential to the integrity of these efforts. This is no game; world markets have a lot riding on the outcome.

Editor’s note: “Fuzzy Math” is a refreshed version of an essay that appeared two years ago. With government budget issues at the forefront in the world today, an encore seemed warranted.

Ongoing Drama

Greece may no longer be on the list of top risks to the global markets, but the travails of the Greek economy are far from over. Unemployment remains unconscionably high at 23%. The economy has only just emerged from three years of deflation and real gross domestic product (GDP) remains more than a quarter below its pre-crisis peak.

Public debt in Greece is at a level that is not sustainable. The International Monetary Fund (IMF) has urged debt relief, while European creditors (primarily Germany) have counseled austerity. The fate of the next phase of the €87 billion Greek bailout will depend on the reconciliation of these two perspectives.

There is even a difference of opinion on the current state of Greek public finances, with the IMF projecting a near balance (fiscal balance excluding interest payments) and other debtors estimating a primary surplus of up to 1% of GDP for 2016. Key here is the assumption of the fiscal multiplier, and the IMF expects the fiscal tightening to be much more contractionary. If the IMF’s growth and deficit projections find the debt to be unsustainable, it would no longer participate in the bailout.

The IMF is concerned about the viability of asking Greece to run annual primary budget surpluses to the tune of 3.5% of GDP, which is mandated by the current program. At the same time, the IMF is frustrated at the lack of progress toward “growth-enhancing” structural reforms in Greece by the government of Prime Minister Tsipras.

With elections coming up, governments in the Netherlands and Germany want to keep the IMF on board and avoid debt relief, lest they give an impression of going easy on the Greeks. An optimistic fiscal projection allows European leaders to keep the IMF involved in the program while preserving the right to blame Greece if targets go unmet.

There is some urgency to this process. 2017 could shift the political center further away from the EU in Berlin, Paris and the Hague, something that will make its governments even less willing to give concessions to the Greeks. At the same time, a non-deal would complicate matters with a crisis-weary electorate.

To complicate matters further, there is a reasonable chance of the Greek government calling for fresh elections if it is forced to adopt more painful reforms and spending cuts in return for new funding. Given that the Tsipras government would most certainly lose, new elections would be either “anti-austerity” political grandstanding or a bargaining chip with European governments that would rather avoid another Greek crisis while they seek reelection at home. Overall, with so many pieces needed to fall in place for a successful continuation of the current bailout program, a re-run of the 2015 crisis should not be ruled out.

The Challenge of Shrinking the Fed’s Balance Sheet

This year, in addition to the customary market concern about the path of interest rates, a hot conversation topic is when the U.S. Federal Reserve (Fed) will pare back its holdings of Treasury and mortgage-backed securities. The Fed’s balance sheet increased nearly five-fold as a result of its actions following the global financial crisis.

Of the Fed’s $4.4 trillion balance sheet, Treasury securities (56%) account for a significant share, with mortgage-backed securities (39%) following closely behind. The Fed stopped purchases of assets in October 2014 and since then has been replacing maturing securities to maintain the balance sheet level.

In December 2015, the Fed indicated that reinvestment of the securities portfolio would continue until “normalization of the level of the federal funds rate is well underway.” This statement does not indicate when precisely the Fed will stop reinvesting. A good proxy is the response of primary dealers to the New York Fed’s December survey asking for their expectations for the federal funds rate “when the Committee first changes its reinvestment policy” and the month they forecast the change to occur. The dealers’ median responses were 1.38% for the policy rate and June 2018 on timing.

In the past few weeks, Fed officials have offered their views about the balance sheet. These developments suggest the Fed is perfecting its views in preparation for changing strategy. Former Fed Chairman Ben Bernanke offered his thoughts on appropriate timing here.

Sustained expansion should expedite the termination of the current reinvestment policy. The Fed will have to choose between a gradual reduction in reinvestment or a complete termination. There are benefits to shrinking the balance sheet instead of raising the policy rate. Such an action might tend to weaken the dollar, which could spur exports and boost factory activity. In the global context, a depreciation of the dollar would reduce pressures on countries with fixed exchange rates and external debt.

Our view is that the 2013 “Taper Tantrum” event is etched in the memory of Fed officials and there is no appetite for another such episode. The Fed will want to be especially sure of its timing and will endeavor to provide enhanced communication to minimize market turbulence.

Author

Northern Trust Economic Research Department

Northern Trust

More from Northern Trust Economic Research Department