Fuel rates cut, subsidy on gas cylinders as Centre steps up to curb inflation

Key Highlights

- U.K. consumer confidence hits all-time low but retail sales bounce.

- Japan's GDP shrinks as surging costs raise spectre of a deeper downturn.

- Eurozone Q1 GDP growth rate revised upward to end-2021 pace.

- WPI inflation rises further to 15.08% in April from 14.55% a month back.

- RBI MPC minutes show the need for front-loading interest rate hikes in upcoming meetings, experts say.

- China cuts mortgage lending rate by the record as lockdowns hit the economy.

USD/INR Weekly performance & Outlook

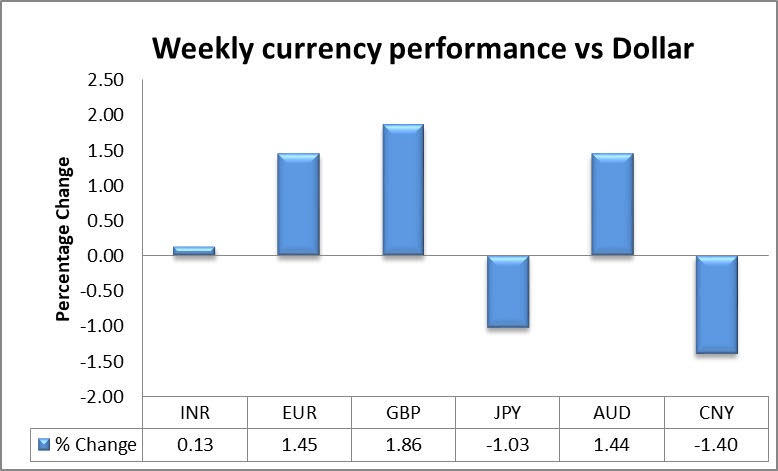

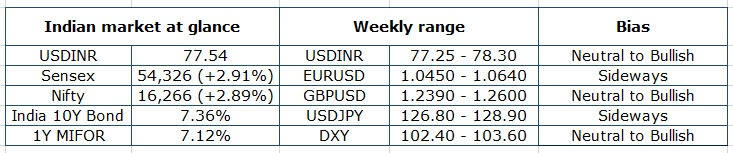

The USD/INR pair made a gap up opening at 77.67 levels and remained volatile during the week. The pair closed the last trading session at 77.54. The USD/INR pair initially rose tracking the strong dollar, along with the prospects for a more aggressive policy tightening by the Fed. However, later in the week, the pair was seen trading in a range-bound manner as investors lacked direction. The U.S. dollar edged slightly lower but remained above the 103 mark, handing back some of the previous session's gains although the safe haven remained in demand with risk sentiment fragile. The pair is expected to trade with a neutral to bullish bias amid the unending Russia-Ukraine war and further anticipated escalation in the war situation after Sweden and Finland officially joined NATO which will keep the dollar in demand for a little longer. The Reserve Bank of India’s continued intervention to protect the level of 77.50-77.70 level, capped any major gains in the USD/INR pair. The Centre on Saturday finally slashed excise duty on petrol and diesel by Rs 8 and Rs 6 per litre respectively. This will reduce the price of petrol by Rs 9.5 per litre and of diesel by Rs 7 per litre. This is expected to cool off the surging inflation pressure in the near term. The RBI surplus transfer to the government was sharply down at ₹30,307 crores and the added cut in the petrol prices is expected to impact the Govt revenue and thereby Budget maths. The focus will be on the US GDP data and FOMC meeting minutes expected to be released later in the week.

Eurozone April inflation revised down to 7.4%; still a record high.

EURUSD:

The EURUSD pair opened the week at 1.0405 and moved upwards to touch a weekly high of 1.0607 levels. The pair remained volatile and closed the week at 1.0562 levels. The pair majorly remained above the 1.05 level during the week on the back of a weaker US dollar, despite a risk-aversion environment that usually benefits the dollar. In the last trading session, the Euro traded a tad down against the US dollar on worries over rising inflation and investors' weak risk sentiments. ECB unveiled its last monetary policy minutes, in which ECB hawks are calling the shots. The minutes confirmed the increasingly hawkish tone of many ECB members since the April meeting. There seems to be an eerie feeling that the ECB is acting too late and quickly needs to join the bandwagon of monetary policy normalization. This means that the question is no longer whether the ECB should hike interest rates in July but by how much. The focus will be on the PMI data from Eurozone, Eurogroup Meetings, and ECB Financial Stability Review. The pair is expected to trade with a sideways bias.

UK inflation hits a 40-year high of 9.0%, squeezing households harder.

GBPUSD:

The pair has rallied from a low of 1.2217 seen at the beginning of the week and continued to trade on an upward trajectory. The pair saw a high of 1.2524 during the week and closed the week at 1.2489. A pullback in the dollar index and better-than-expected UK macro data also supported the pound. The UK Office for National Statistics reported that Retail Sales unexpectedly rose by 1.4% in April as against consensus estimates pointing to a drop of 0.2%. Market data suggests another 25 bps hike is priced in for the next meeting on June 16. Looking ahead, the swaps market is pricing in 150 bps of total tightening over the next 12 months that would see the policy rate peak near 2.50%, steady from the start of last week. Brexit issues cloud over cable as the EU ambassador to the UK has rejected the UK's demand that the Northern Ireland protocol is rewritten, and issued a blunt warning of retaliation if the government passes a law disapplying aspects of the agreement. The pair is expected to trade with a neutral to bullish bias.

Powell says the Fed will not hesitate to keep raising rates until inflation comes down.

Dollar Index:

Following Thursday’s deep pullback to 2-week lows in the sub-103.00 region, the index regained some ground lost amidst the mixed note in the US cash markets and the absence of a clear direction in the broad risk appetite trends. In the meantime, investors remain vigilant on the possibility of a “hard landing” of the US economy amidst elevated inflation and the Fed’s more aggressive tightening of its monetary conditions. According to CME Group’s FedWatch Tool, the probability of a 50 bps rate hike at the June 13 meeting is at 93% and 85% when it comes to the July 27 event. The dollar attempts a mild rebound to the 103.00 neighborhood following the multi-session drop recorded on Thursday. In the meantime, and supporting the dollar, appears investors’ expectations of a tighter rate path by the Federal Reserve and its correlation to yields, the current elevated inflation narrative, and the solid health of the labour market. On the negative for the dollar turn up the incipient speculation of a “hard landing” of the US economy as a result of the Fed’s more aggressive normalization. The dollar index is expected to trade with a neutral to bullish bias.

Domestic and Global Equities:

Domestic Equities:

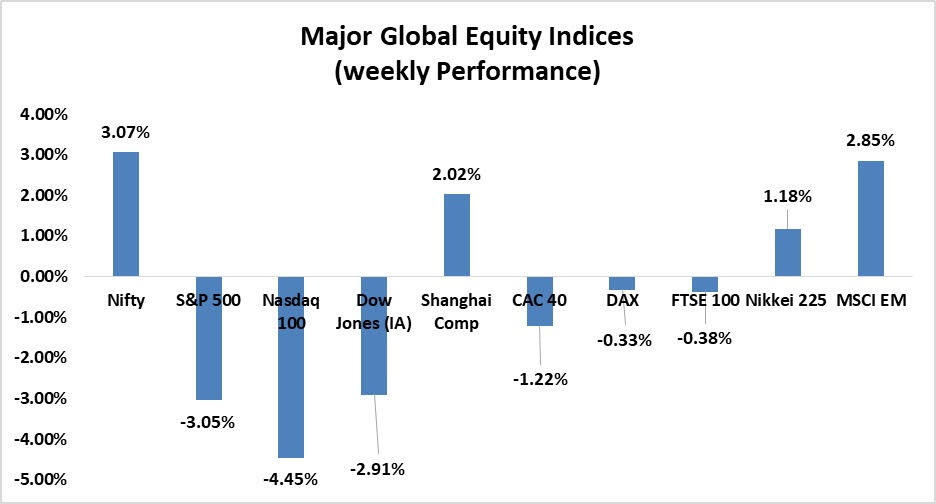

Indian indices bounced back in style from the previous slumps in the last session of the week as both the Sensex and Nifty advanced close to 3%, tracking positive trends from Asian peers. Asian investors reacted positively to the Chinese central bank's decision to reduce its rate on a five-year loan, which would shore up weak housing sales by cutting mortgage costs. On a weekly basis, Nifty Metal and Nifty Auto were the biggest gainers whereas Nifty IT was the only loser. With concerns over an economic slowdown and rate hikes across the globe, investors will continue to invest with caution.

Global Equities:

Global equity markets rebounded after the S&P 500 pared losses that briefly took it into the bear market territory, as investors unease about Federal Reserve policy tightening to curb inflation kindled fears of a recession. Shares rebounded in Europe and Asia after China cut a key lending benchmark to bolster its weakening economy, helping initially to drive gains on Wall Street. While a late-day rally stopped the S&P 500 from confirming a bear market, the gloom on Wall Street led the benchmark to fall for the seventh consecutive week, an event that has occurred only five times since 1928, according to S&P Dow Jones Indices. Overall, global stock markets have seen another volatile week as recession fears gripped investors after weak Chinese retail sales data and dismal results from big US retailers highlighted the impact of surging inflation. Shares rose in Japan, South Korea, Australia, Hong Kong, and Shanghai.

Domestic and Global Bonds:

Domestic Bonds:

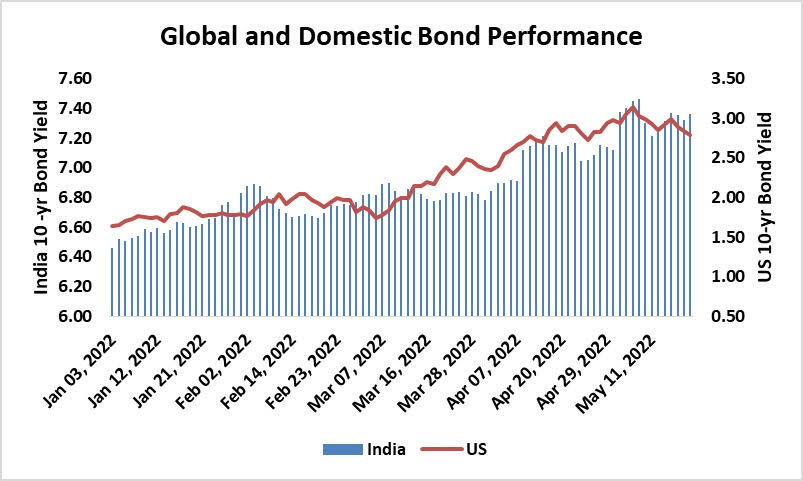

Indian government bonds have experienced much turbulence over the last couple of weeks, see-sawing between considerable gains and losses as traders have reacted to a wide range of contrasting developments. The elevated inflation, surging crude prices, and other global cues kept the domestic bond market under pressure during the week. India's 10-year benchmark closed the week at 7.359%. One of the members of India's rate-setting Monetary Policy Committee stated that there is a need to front-load rate hikes as higher long-term yields can affect private Capex spending.

Global Bonds:

The yield on the benchmark 10-year U.S. Treasury note has moved down to 2.79% from May peaks of 3.2% on expectations that forthcoming U.S. rates by the Federal Reserve in June and July will be capped at a half-percentage point each round, instead of the initially-speculated three-quarter point. Yet, with rate expectations often moving on a dime, yields could jump too.

Monthly FPI Net Investments:

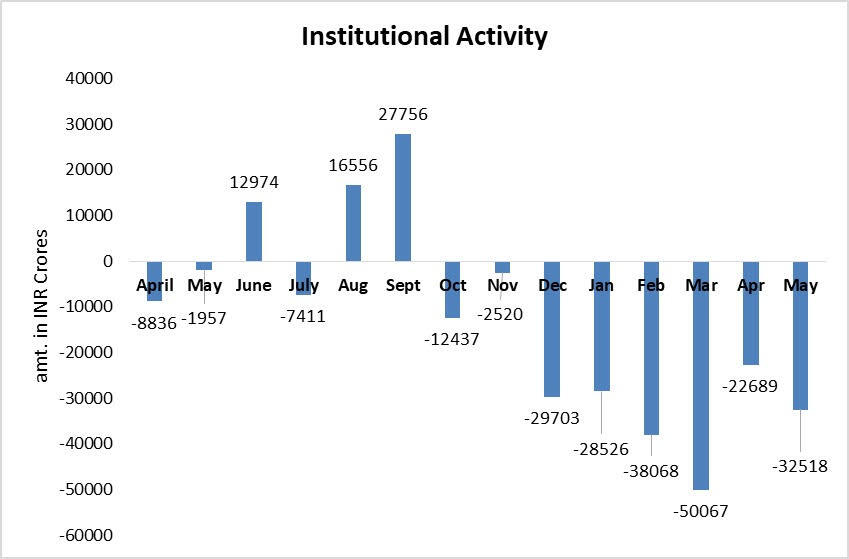

Since October last year, FPIs have sold equities worth nearly 2 trillion rupees with 4 of the eight months seeing selling of over 30,000 crore rupees each. That said, what has worsened the correction is the relentless selling by foreign portfolio investors for eight consecutive months. Despite retail investors and domestic institutional investors giving muscle to the market, FPIs are having an upper hand. Soaring oil prices and earnings downgrades are expected to keep market confidence muted in the near term.

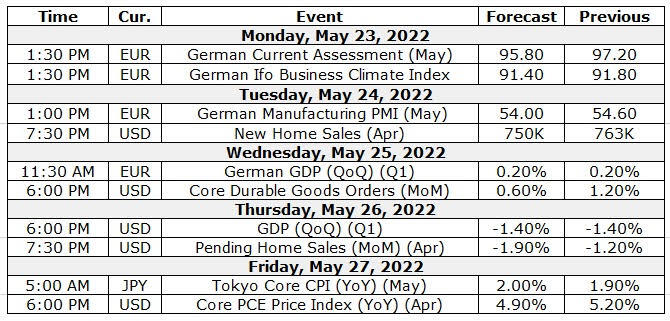

Macro-economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.