FTSE snaps 3 day winning streak

The FTSE has opened on the back-foot snapping three straight sessions of gains. Despite the slip lower this morning the UK index is still on track for gains in the region of 10% across the week, its first winning week since early February.

The big question is whether this is a false floor or whether it is the start of a more meaningful advance? The awful data is only just starting to show through. Chinese industrial profits slumped by the most on record. Italian and French consumer confidence is expected to plunge.

US consumer confidence in focus

US consumer confidence figures will guide trader’s sentiment this afternoon. After yesterday’s record breakingly dreadful initial jobless claims, consumer confidence in the US has to be on its knees. Whilst yesterday we saw dire data boost expectations of more US stimulus and lift markets higher, today we might not see the same reaction. There is a good chance that traders[fg1] are still too nervous to hold positions over the weekend. This will be at telling signal as to how ready traders are to continue the push higher.

The number of cases in the US, the world’s largest economy have surpassed the number in China or Italy. Numbers over the weekend could escalate sharply.

House builders under pressure as housing market stalls

Here on the FTSE UK house builders could struggle as the UK housing market is being brought to a near standstill by coronavirus. Even those that have exchanged contracts are being advised not o complete, with mortgage lenders extending mortgage offers for three months to help the rebound after the social distancing measures are eased.

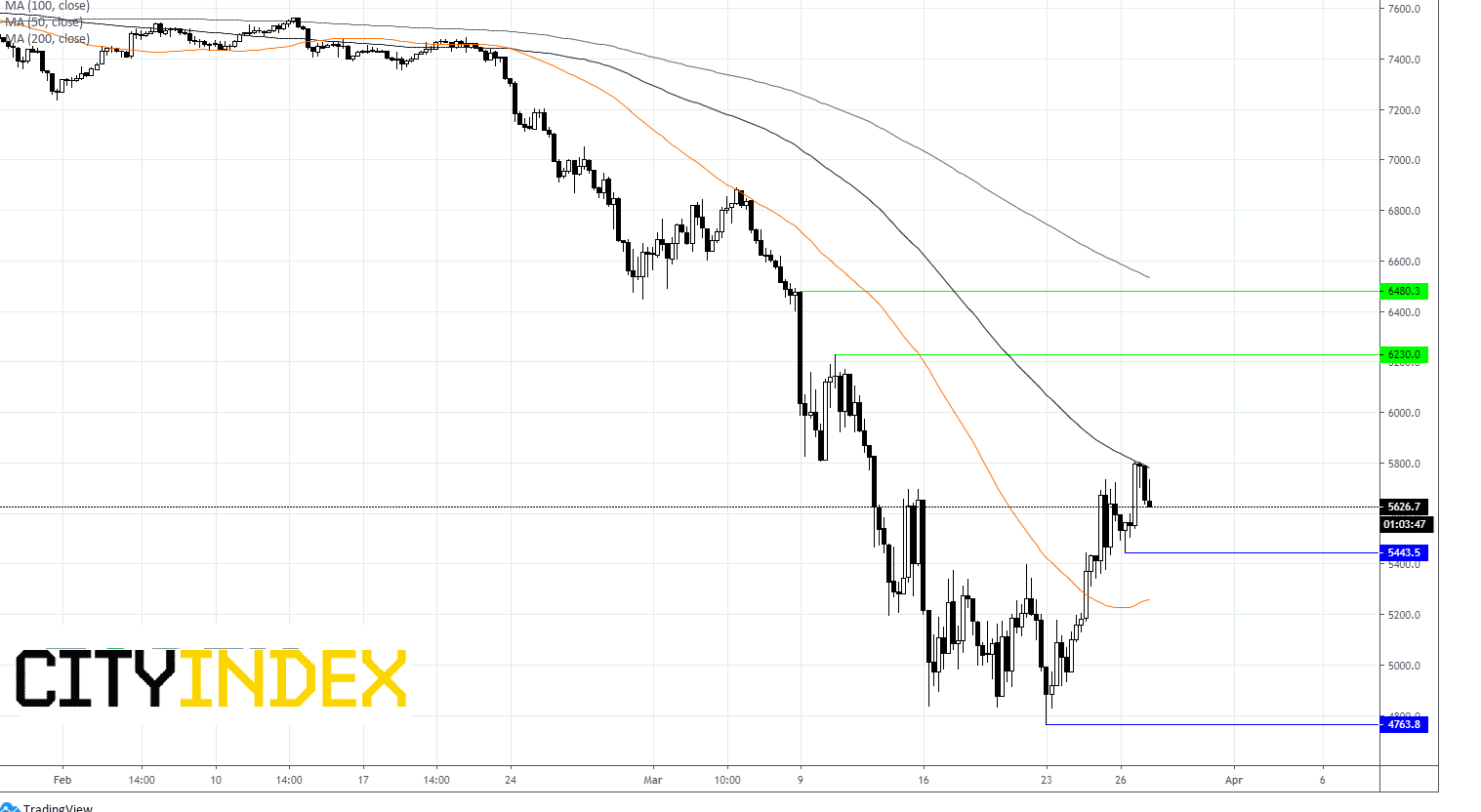

Levels to watch

The FTSE has dropped 3% on the open after failing to push through resistance at 100 sma on 4-hour chart.

Immediate support can be seen 5448 (yesterday’s low) prior to 5254 (50 sma) and 4762 (low 23rd March).

On the flip side, strong resistance is at 5787 (today’s high & 100 sma) prior to 6230 (high 10th March).

Author

Fiona Cincotta

CityIndex