From the earth to the sky

While coal remains the leading source of electricity production in the world (36% of the total) and particularly in the emerging world (74% of the total in India, 63% of the total in China), its use has been marginalised in the European Union (EU). In 2022, the war in Ukraine caused concern about a possible resurgence of coal, which never actually materialised. In its latest European Electricity Review published in January[1], the think tank Ember states that the reactivation of coal-fired power plants has been limited, both over time and in respect of additional megawatt hours generated. This was due to a relatively mild winter, calls for fuel economy which were heeded, and an all-round diversification of gas supplies, which in the end were not lacking, with gas continuing to account for around 20% in the European mix.

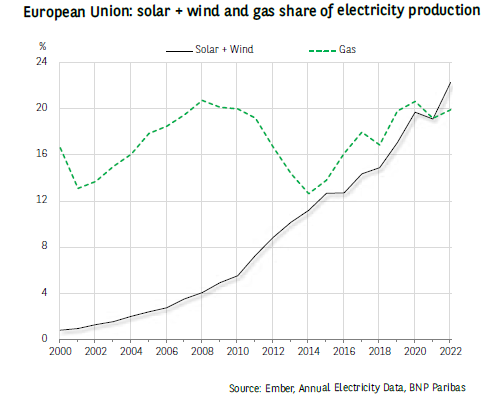

But the remarkable point lies elsewhere. By cutting out Russian hydrocarbons, the EU has accelerated its shift towards renewable energy. Promoted by States and governments, increasingly competitive (the cost of photovoltaics is a tenth of what it was fifteen years ago) and subjected to a learning curve that is constantly improving their yields, solar and wind technologies are now making their mark on the Old Continent. In 2022, they overtook gas in electricity generation (graph), for the first time and no doubt permanently.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.