French election has market fretting

No US rate hike until June

Economic data, including the numbers for employment growth, continue to point to a buoyant US economy. Inflation has risen slightly recently, though without feeding through to wage growth. Hence, the economy looks ready for another rate hike from the Federal Reserve and indeed several FOMC members have recently begun to edge towards hiking rates once again. In our view, the Fed will most likely wait hiking rates until June and then deliver another hike in December. The financial markets are also pricing two rate hikes this year. If we and the markets are proved correct, US monetary policy should not have any great significance for the USD this year. We still expect EUR/USD to rise to around 1.12 in the coming 12 months.

Oil price has stabilised

Brent oil prices have stabilised at around USD55-57/bbl over the past month. OPEC and a number of non-OPEC producers appear to have implemented their planned production cuts more or less fully. Nevertheless, oil inventories in the US are rising again despite stocks normally being drained lower in the winter. Moreover, the number of active oil rigs in the US has continued to climb, indicating that US oil production is set to increase in coming years. All in all, there is still ample supply in the market, which should tend to dampen oil price increases for now and in coming years.

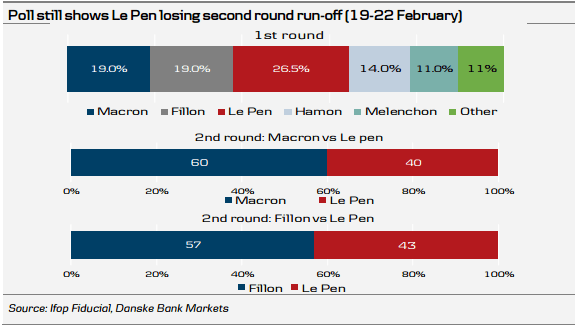

French election has market fretting

The French are due to cast their votes in the first round of the presidential elections in April. While French presidential elections are not normally a big attention grabber for the financial markets, this time is different as Le Pen has declared that she would like to pull France out of the euro and reintroduce a national currency. According to the polls, it is most likely that either the independent Emmanuel Macron or the Republican Francois Fillon will become France's next president. However, polls also indicate that it is a close race between the candidates, and thus there is a significant risk that Marine Le Pen will win the presidential election. Uncertainty on France’s commitment to the euro has pushed French government bond yields up, while sending yields on German government bonds lower and weakening the EUR. Whether Le Pen will/can actually hold an EU/euro referendum will to a large degree depend on the National Front’s performance in the parliamentary elections in June and support from the PM. The road to 'Frexit' is long and it is questionable whether the public would vote in favour of such a step. In Le Pen - What If? Implications for Euro and Nordic markets, 23 February, we lay out our take on the market implications if Le Pen wins, with a particular focus on the euro and Nordic markets.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.