France: The decrease in outstanding housing loans is expected to continue

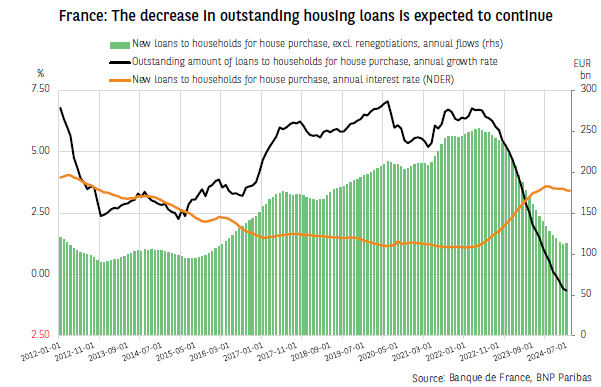

The outstanding amount of loans to households1 for house purchase fell year-on-year by 0.65% in July 2024. It stood at EUR 1,424 billion, compared to EUR 1,433 billion at its record high in July 2023. This fourth consecutive decline is particularly remarkable, given that the first (-0.06% in April 2024) was already unprecedented for this series of data, which has been recorded since April 1994.

The decline in the outstanding amount is entirely due to decreasing new loans to households for house purchase (excluding redemptions and renegotiations, which have no effect on outstanding loan amounts at a banking system level). New housing loans are no longer balancing out repayment flows, which have nevertheless decreased since the end of 2022 due to deferrals and suspensions of installments. Cumulated over one year, new loans amounted to EUR 113 billion in July 2024, compared to EUR 253 billion at their peak in May 2022 and a level constantly above EUR 150 billion seen between December 2016 and October 2023. Taking the interest rates and initial loan terms into account, our estimate of repayment flows suggests that the decline in the outstanding amount of loans would continue pending a more pronounced recovery in new monthly production (EUR 12.2 billion in July 2024, compared to its low of EUR 7.5 billion in March 2024). This recovery in new monthly production could take time to materialise while real estate prices continue to fall rather modestly in view of the drop in transactions and the sharp fall in new production, whereas the pace of decline in average loan rate (3.41% in July 20242) slows down.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.