France-Germany: The roots of equity capital increases for NFCs (excluding valuation effects)

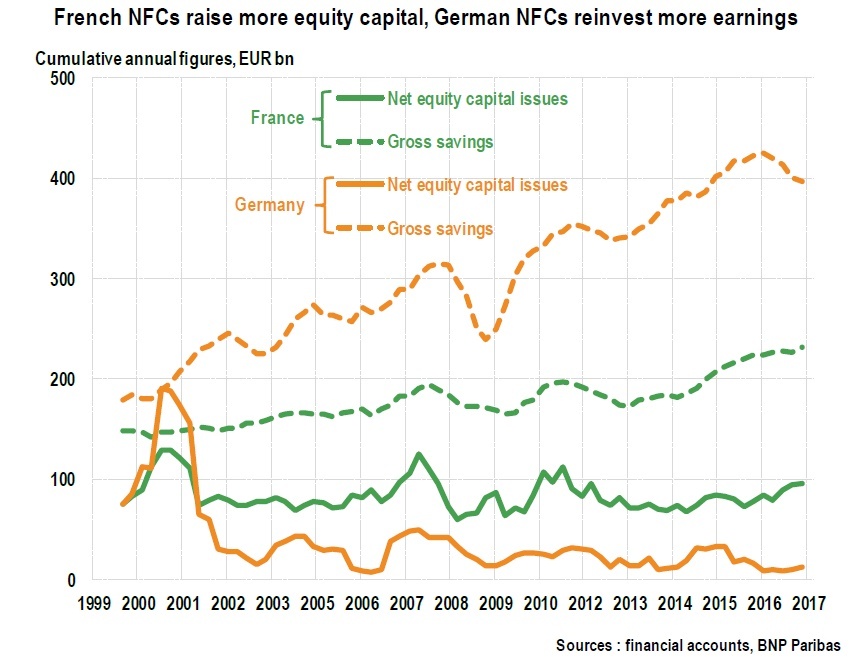

Between 2012 and 2017, French non-financial companies (NFCs) generated 35% less value added than German NFCs, but net annual issues of equities and other share capital (i.e. after repurchases) were nearly five times higher on average (EUR 80 bn vs. EUR 17 bn). This shows that most companies have had no trouble raising funds in France. Moreover, this ranking can be seen regardless of the instrument under consideration (listed or unlisted shares, other share capital).

In contrast, reinvested earnings (indicated here as gross savings) were almost twice as high in Germany (EUR 386 bn vs EUR 202 bn, or a spread of 190%), resulting in a much bigger annual increase in equity capital than in France (42% higher at EUR 403 bn a year vs EUR 283 bn). At a time when apparent earnings distribution rates are comparable (50% in France, 46% in Germany), the smaller increase in the equity capital of French companies can be attributed to their lower financial returns.

Author

Laurent Quignon

BNP Paribas