Forex markets lacking conviction as US yields lose direction

Market Overview

With the dollar starting to claw back some of the lost ground of the past week, forex markets have begun to look increasingly uncertain. Market sentiment remains bogged down in concerns over trade wars which have seen 10 year Treasury yields lose direction and meant that conviction has gone out of the market. Other factors helped to support the dollar overall yesterday though and the rise in Italian bond yields ahead of a key bond auctions later in the week have weighed on the euro (although the Bund/Treasury spread is still pointing towards support for the euro on the yield differentials). Sterling has been hit as incoming Bank of England policy committee voter, Jonathan Haskel, seemed to suggest he is fairly dovish in his first real indication of stance yesterday. However, as we near the end of the quarter there is little real direction of not today across the forex majors. The oil price has been boosted as the US is urging its allies to boycott Iranian supplies after November whilst a surprisingly large drawdown in the API crude inventories is also supportive. Equity markets are being buoyed by the support for oil, although after the somewhat listless rebound yesterday, if the lack of conviction continues there is little to drive any decisive rally.

Wall Street closed marginally higher with the Dow marginally positive and the S&P 500 +0.2% higher at 2723. However, with US futures suggesting a pulling back on these gains today, the Asian markets have struggled (Nikkei -0.3%). European markets are basically flat and once more lack the conviction in a recovery. In forex, there is a mixed picture developing for the dollar as yesterday’s gains are consolidated. The euro has ticked marginally higher, whilst the yen has also clawed back some ground, however the New Zealand dollar is the big underperformer eve ahead of tonight’s RBNZ meeting announcement. In commodities, it seems as though there is little respite for gold which is once more lower, by around $3, whilst oil is consolidating the strong gains from yesterday.

The main data point of the day for traders to be interested in is the US Durable Goods Orders release at 1330BST which is expected to see core (ex-transport) grow by +0.5% for the month of May (+0.9% in April). Pending Home Sales are at 1500BST and are expected to growth by +0.5% on the month (last month was a fall of -1.3%). The EIA oil inventories are at 1530BST and are expected to show crude stocks in drawdown by -2.5m barrels (-5.9m barrels last week) whilst distillates are expected to build by +1.0m barrels (+2.7m last week) and gasoline stocks build by +1.0m (+3.3m last week). Very late in the session we have the Reserve Bank of New Zealand monetary policy at 2200BST which with little real data changing since the May meeting is expected to hold the Official Cash Rate steady at +1.75%. New Zealand inflation is still subdued and should mean that a dovish tone should persist in the statement. Markets are currently not expecting an increase in the OCR until Q3 2019. Aside from the data, traders will also be interested in the comments of the “unreliable boyfriend” Bank of England Governor Mark Carney who speaks at 0930BST at the Financial Stability Report press conference. FOMC voting member Randall Quarles (centrist/hawk) speaks at 1600BST.

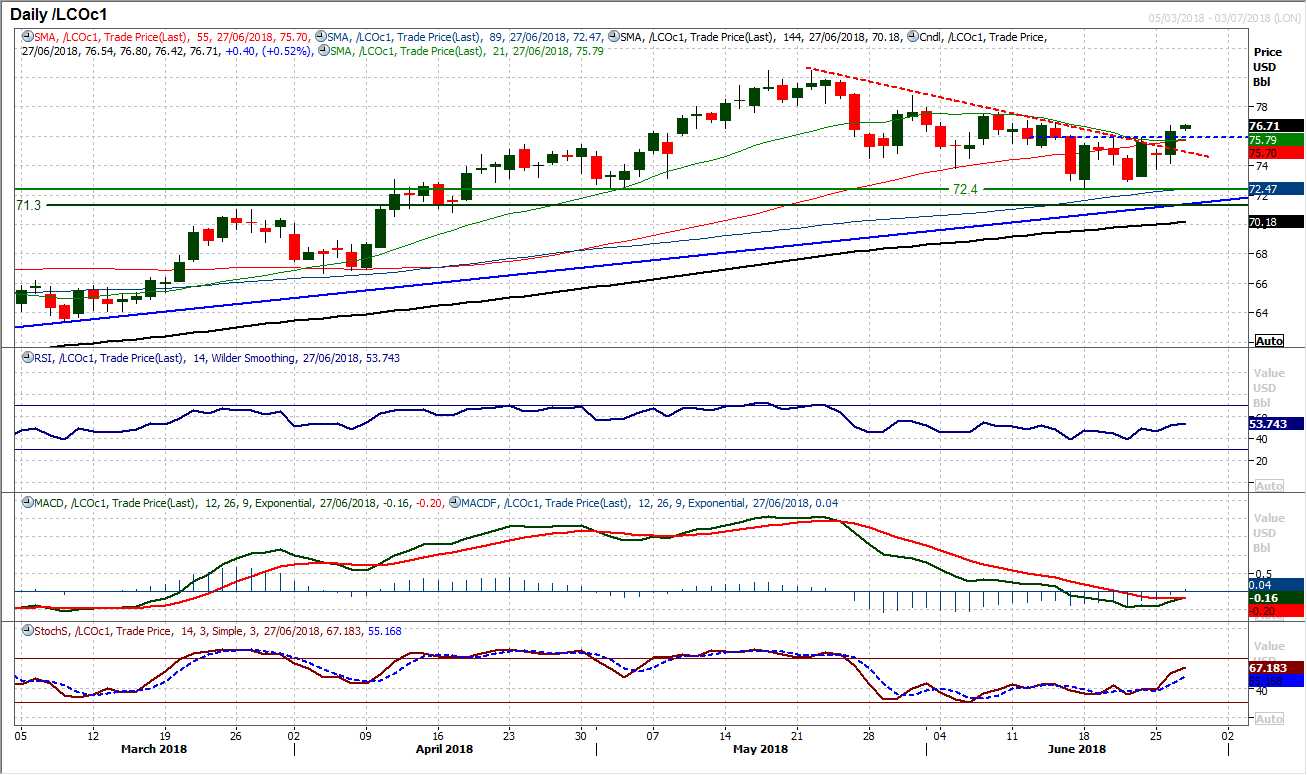

Chart of the Day – Brent Crude

With such variation in the spread between WTI and Brent Crude, the technical analysis of Brent can be significantly different to its US oil peer. There has been a very well-defined downtrend on Brent Crude in the past five weeks as the market has corrected back towards the old key breakout at $71.30 only to find a basis of support at $72.40 which is also above a 12 month uptrend. With the support also building in the wake of the OPEC meeting, this near to medium term correction within the longer term uptrend looks to be another chance to buy. The momentum indicators have stabilized from the corrective phase, with the RSI bouncing above 50, whilst the Stochastics have broken out to four week highs and the MACD lines are on the brink of a bull cross today. Yesterday’s bull candle broke the five week downtrend but also took the market above initial resistance at $75.85 which is a first lower high of the correction. This effectively completes a small base breakout implying around $3 of further recovery and means the June high at $77.60 comes back into play. There is now support around $75.85 with the post OPEC low of $73.75 adding further support.

EUR/USD

The prospective recovery on EUR/USD hit a setback yesterday as a negative candle cut 55 pips of the price and threatens the momentum of the rebound. If this is a range play between $1.1505/$1.1850 then it could easily turn out to be a market that develops intra-range noise. This means that the market could struggle to form trending moves and retracements could become frequent. Momentum indicators have been threatening recovery but have just tailed off with yesterday’s drop. For now there is a basis of a pivot around $1.1640 which needs to be watching, and this is especially prominent on the hourly chart. Hourly momentum is suggesting that this is a range play now, but a fall below support at $1.1600 would increase the pressure on the key support at $1.1505. Yesterday’s high at $1.1720 is now initial resistance.

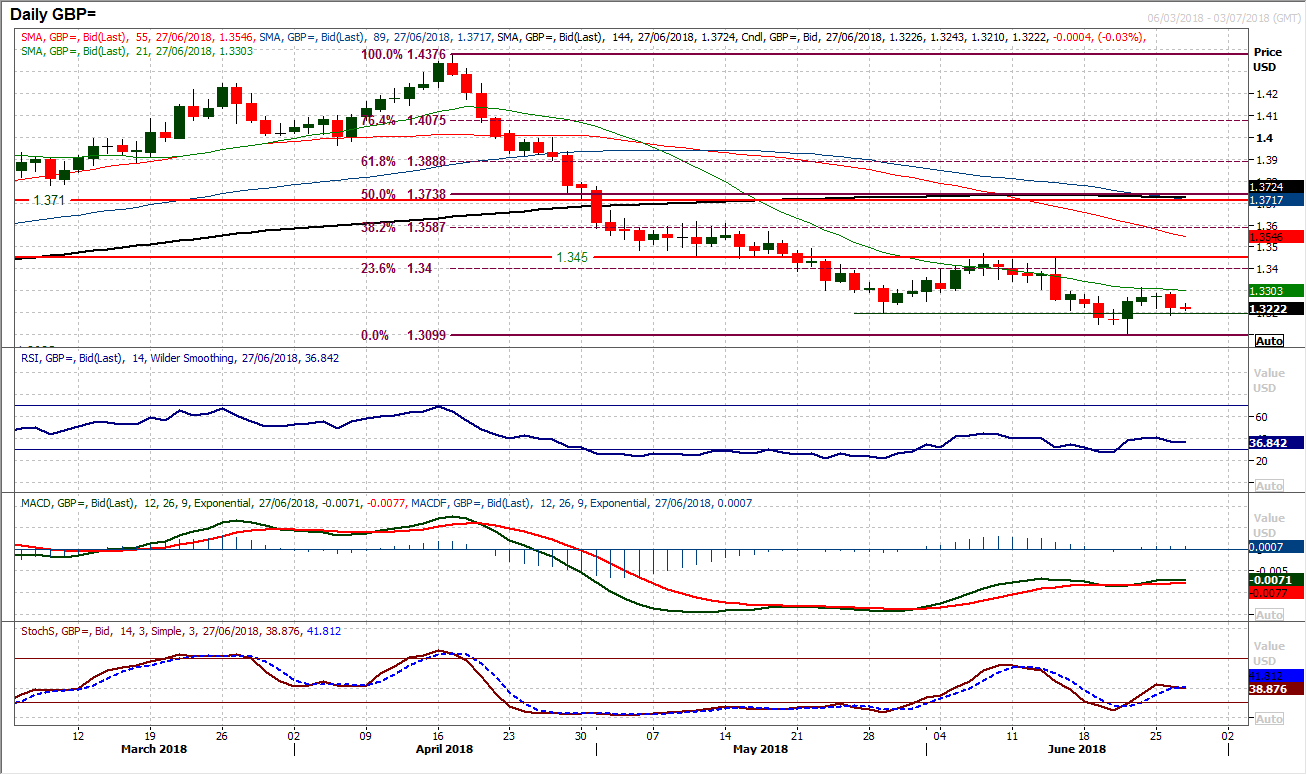

GBP/USD

A negative candle posted yesterday has questioned the prospect of a Cable rally. Pulling back to the support around the old $1.3200 low is now testing the resolve of the bulls. It now means that today’s candle could be key as to how the outlook develops over the coming days. A second consecutive bear candle that closes below $1.3200 would really begin to pull momentum back lower into more corrective configuration again. This would also then open the support at $1.3100 to be scrutinised again. Resistance at $1.3315 now also takes on a more important role too. The hourly chart shows the pressure on $1.3200 is mounting but for now the hourly momentum configuration is still relatively rangebound. This would change if the RSI begins to move decisively below 30. Yesterday’s high of $1.3290 is initial resistance.

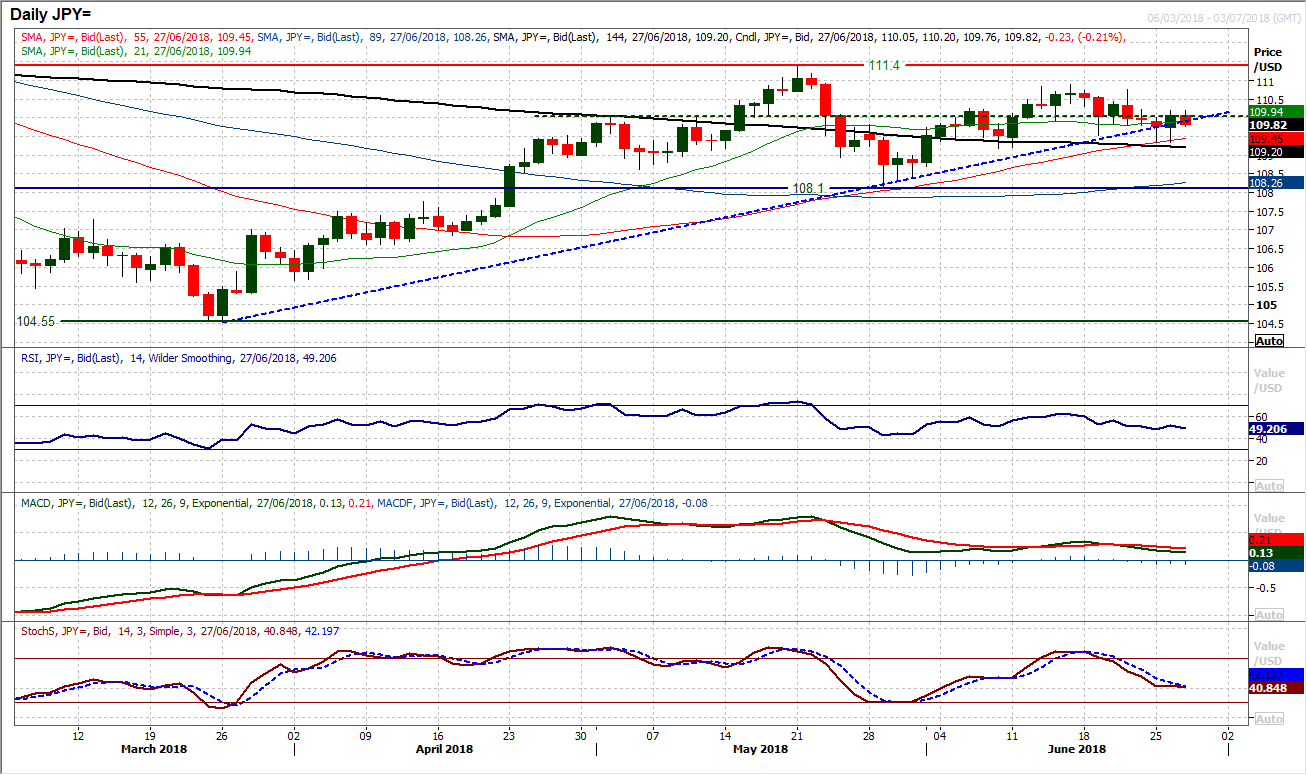

USD/JPY

Yesterday’s bullish candle has helped to prevent the market from turning increasingly corrective, with the support at 109.15 holding. However the support of the three month uptrend has been broken and the bulls do not trade with any real conviction now. What is possible is that the market may begin to chop higher and lower (presumably continued on/off newsflow on trade tariffs may have a part to play in this). Momentum indicators retain their positive bias (which bolsters the key near to medium term support at 108.10) but this is a market in search of conviction now. The hourly chart shows a basis of a pivot now around 110.25 which again capped the upside yesterday, with momentum indicators oscillating (RSI between 30/70) reflecting a range play. Above 110.20 opens 110.75 whilst a decisive move below 109.80 opens 109.15 again.

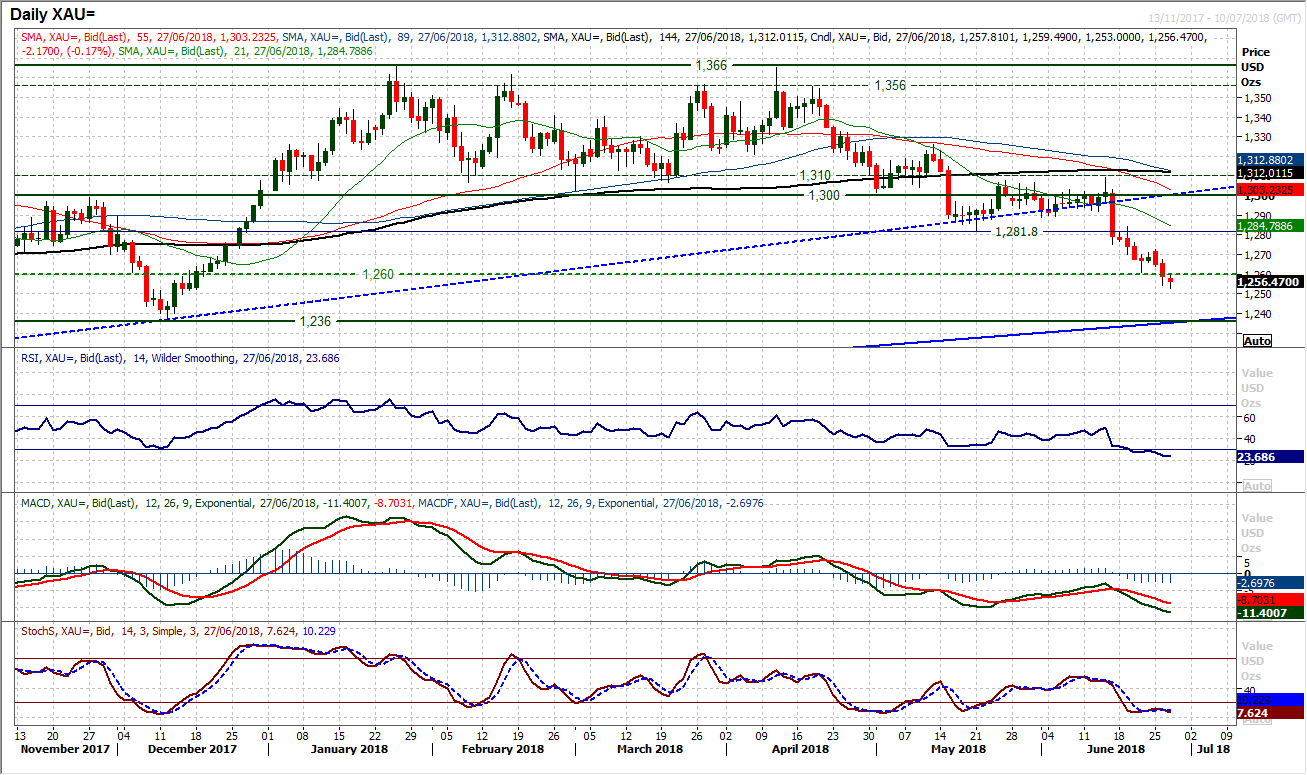

Gold

Another decisive negative candle simply looks to continue the medium term correction which eyes the key December low at $1236. A close below $1260 now means that the last real support that protects the December low has been removed. Momentum remains deeply negative, with the RSI falling towards the low 20s, MACD lines accelerating lower and Stochastics even turning back lower again. There is now a lower high at $1272.50 as resistance, whilst the old $1260 breakdown is an initial basis to work from today. The hourly chart shows anything that unwinds the momentum from oversold is being used as a chance to sell, with $1260/$1262 an initial sell zone.

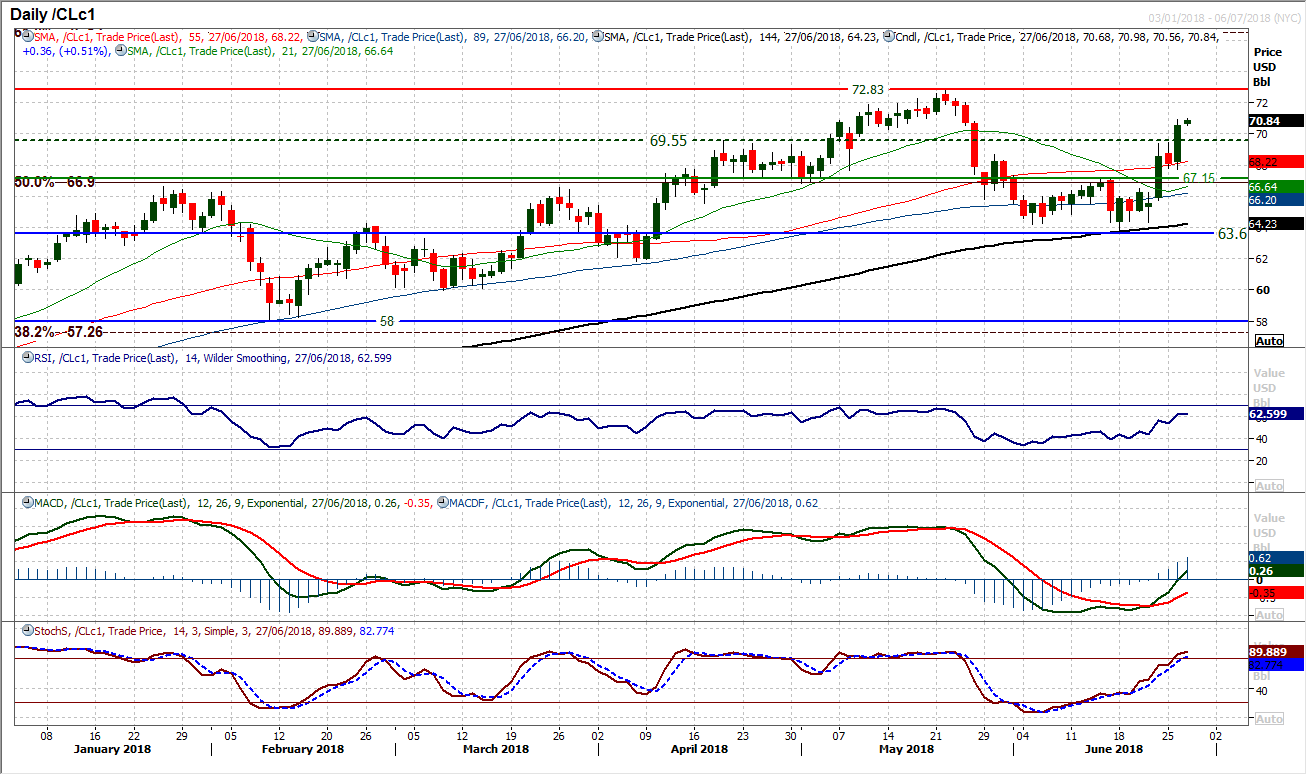

WTI Oil

The market initially consolidated the OPEC breakout on Monday, but the bulls have stormed back to prominence now as another strongly bullish candlestick formed yesterday. Having broken out above the near term resistance at $67.15 the market has now left a good basis of support between $67.15/$67.80 and has now achieved the $3 upside target of $70.15. This now leaves the $72.83 key May high as the next target area for the bulls. Momentum indicators are still decisively improving configuration with the RSI now above 60 and rising conditions for the MACD and Stochastics. The bulls will be noting the importance of breaking above Monday’s high at $69.45 which was around the old resistance at $69.55 and is now a basis of near term support for today’s session.

Dow Jones Industrial Average

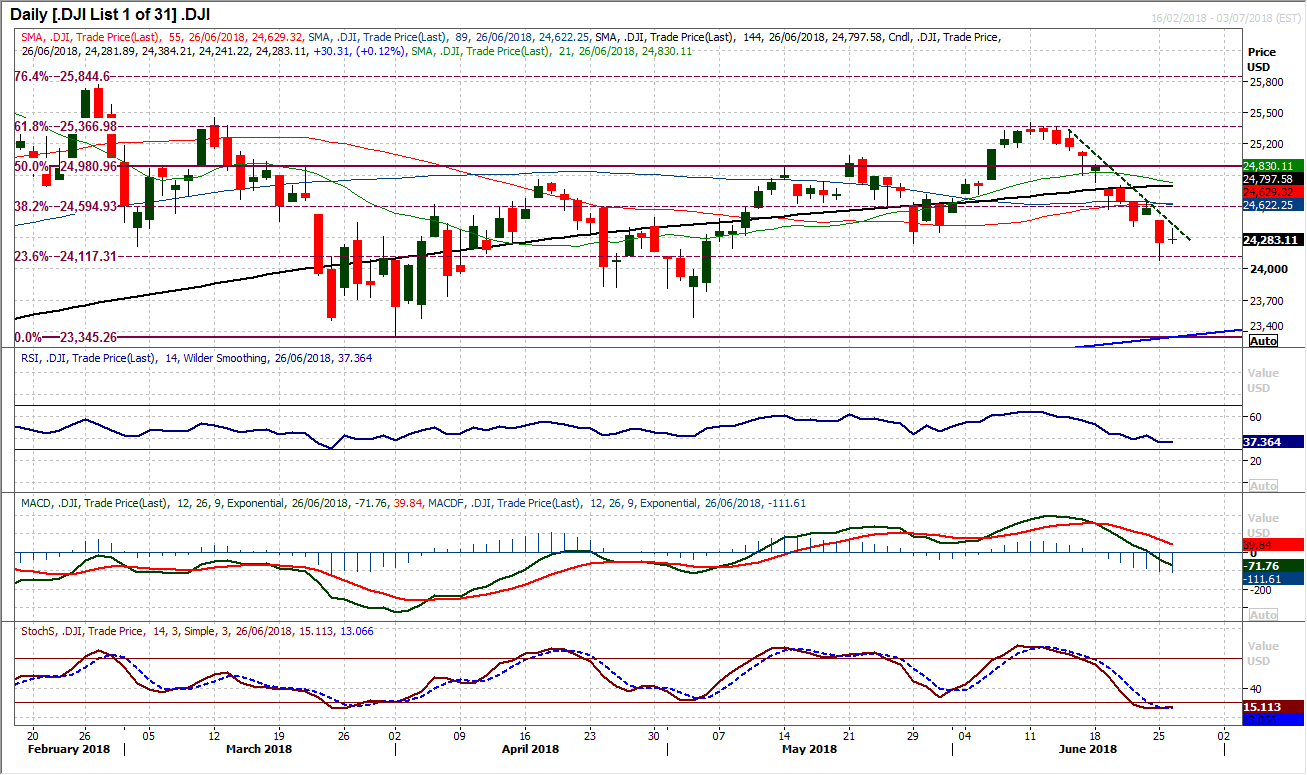

The tepid nature of the rebound yesterday (and subsequent doji candle) will not have helped to improve the outlook which continues on a path of deterioration within the resistance of a 9 day downtrend (which comes in today at 24,320). There is an ongoing negative outlook on momentum indicators with the RSI below 40, MACD lines accelerating lower (now increasingly close to both going negative) and Stochastics negatively configured. The sharp decline of the mini downtrend (which is falling at around 110 ticks per day) means that it is likely to be broken at some stage in the coming days, but there is a band of resistance now initially between 24,407 (old low within the correction) and 24,464. The 23.6% Fib level remains a target area near term at 24,117 whilst the 38.2% Fib at 24,595 is a basis of resistance too.

Author

Richard Perry

Independent Analyst

Richard Perry, Independent Market Analyst, has over 20 years of experience working in financial markets in London.