Forex alert: Fed on hold, March in play, tariffs the wild card

With the Fed's policy meeting expected to hold no surprises this week, attention has already shifted to March. Despite perceptions by some that this week's gathering is a "Nothing Burger," the implications are far from trivial, especially considering the market's heavy lean into long-duration positions. While the Fed is cognizant of these dynamics, even a hint of a hawkish tilt in their commentary could rattle bonds significantly. Moreover, looming tariffs could disrupt the Treasury rally and propel the dollar, adding another layer of complexity to the Fed's calculations. The stakes are high, and even subtle shifts in tone or emphasis from the Fed could have outsized effects on the financial market.

Swaps signal a 30% probability of a Fed rate cut in March, but the overwhelming expectation is that rates will hold steady this week. As inflation continues to grip the financial world tightly, the financial world is eager for any hint of policy shifts on the horizon, and it will be watching every word from Fed Chair Jerome Powell during his upcoming press conference.

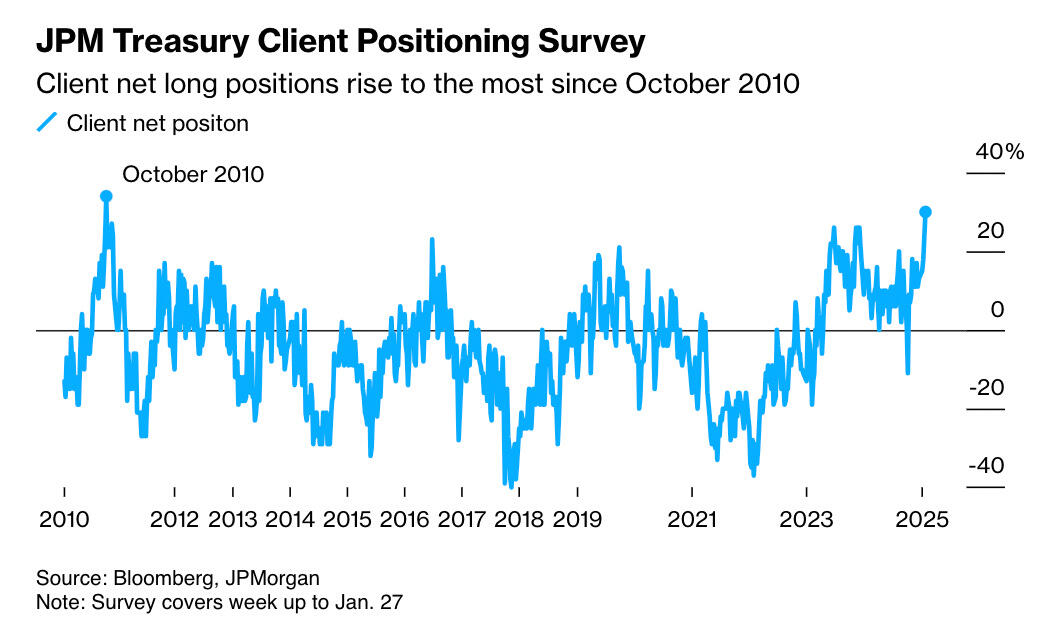

The atmosphere in the markets is tense, spurred by a tech-sector nosedive and a flight to the safety of Treasuries, which has pushed yields to their lowest in weeks. This nervous energy has fueled a historic rally in government bonds, with JPMorgan Chase & Co.'s client survey revealing the most aggressive net long position in 15 years.

Amid these turbulent currents, Fed Governor Christopher Waller's suggestion of possible mid-year easing—post a milder inflation report for December—makes the case for a strategic March rate cut hedge compelling. However, the variable that remains hardest to predict is President Donald Trump’s mercurial tariff policy. His preference for a staggered rollout complicates the economic forecast, especially for FX traders trying to parse the potential impacts.

Tariffs loom large as a wildcard, pivotal in shaping Fed strategy and market dynamics due to their potential to skew business and consumer inflation expectations. Reflecting on 2019, when Trump's trade war escalations prompted preemptive rate cuts by the Fed, this time could be different. With the economy freshly scarred by intense inflation, businesses and consumers are now hyper-aware of price pressures, suggesting the Fed might tread more cautiously in response to new tariff implementations. The stakes are high, and the economic narrative is poised on a knife-edge, ready to sway with each policy and market sentiment development.

The currency market is echoing the stabilization seen in tech stocks, and today, attention is shifting towards central bank meetings. While markets are beginning to lean toward this direction, it isn't easy to see that the conditions for a dovish shift in guidance by the Fed have been met, especially given the recent robust payroll report suggesting strong economic conditions. Instead, the greater risk for dovish repricing in the market, say March to coin flip, now stems more from a potential sharp, tech-led equity selloff rather than a change in the Fed’s communication.

The intertwined relationship between the dollar and U.S. tech stocks, mainly through the lens of U.S. exceptionalism, suggests that another tech downturn may not necessarily fuel safe-haven demand for the dollar. Instead, opting for long positions in the yen against a basket of risk currencies and betting on its strength against the dollar could be a more strategic move for those anticipating further tech market volatility.

US events, including tech developments and tariff threats, are heavily influencing the Euro this week. Given the tariff inflation risk, I don’t see the Fed threatening the short EURUSD position.

Currently, a 2% tariff risk premium is embedded in EUR/USD, reflecting an undervaluation due to the looming threat of universal tariffs and Trump's hawkish stance on the matter. This premium suggests the euro would be undervalued if tariffs were not in play. However, the ongoing risk of not just the introduction but a potential escalation of tariffs means this risk premium gap is unlikely to close soon.

Given the tariff risks and the implied policy divergence between the ECB and the Fed, I see the risk of EUR/USD dropping to 1.03 significantly higher than the risk of rebounding to 1.06. While we continue to hold a short position on the euro, we've taken some profits ahead of this high-risk event to manage our exposure.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.