Footprints comparison

Paris, Gare de Lyon train station, April 2024. While waiting for his train to Marseille, a traveler wanders through the stores. As he has some time to spare, he lingers in one of them, which sells smartphones. A good opportunity to upgrade? After all, his current device is already four years old, the average age at which it is renewed in France; the latest version, which he has in front of him, incorporates more functionalities; and last but not least, it’s his birthday! He buys himself a present... and by doing so, multiplies the carbon footprint of his journey by twenty-five1.

Though it might appear trivial, this short story illustrates how difficult it could be for an open economy to achieve climate neutrality. For any country, carbon footprint is measured not only by what it produces (such as TGV travels), but also by what it imports (such as smartphones). Of the 9.2 tons of greenhouse gases (GHG) emitted annually by each French person, more than half (5.1 tons) are attributable to goods and services purchased abroad. Domestic production accounts for much less (2.5 tons per year and per inhabitant for its non-exported share), while direct emissions (1.6 tons per year and per inhabitant from fuel consumption) complete the picture2.

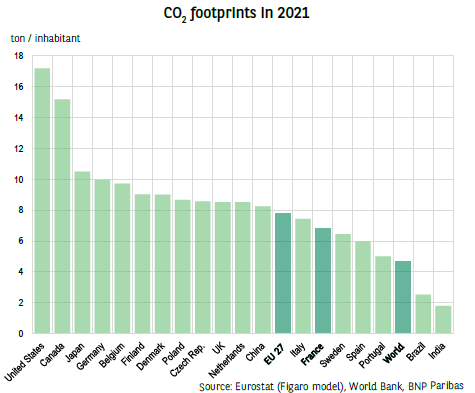

9.2 tons is still a long way from the 2 tons target set by 2050, that would comply with the Paris climate agreements. However, France is not the country with the longest way to go. Because it is service-oriented and relies on nuclear power (one-third of the energy mix, a world record), the carbon intensity of its production is relatively low3. Taking into account imported CO2 emissions does actually add to the balance sheet, but without relegating France to the bottom of the class. According to Eurostat estimates, the individual carbon footprint of the French remains one of the lowest in Europe (in terms of CO2 alone); it also lags far behind American standards (see Chart).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.