FOMC Preview Minutes of the March 19-20 Meeting: The logic of projection

- Fed Funds target range of 2.25%-2.50% unchanged at the March meeting by unanimous vote

- Slower economic activity, household spending and business investment noted in the FOMC statement

- Markets will be looking for elaboration on the extent and depth of the slippage in US economic growth

The Federal Reserve will release the edited minutes of the March 19th-20th Federal Open Market Committee (FOMC) on Wednesday April10th at 2:00 pm EDT 18:00 GMT.

FOMC Policy Analysis

The change in the Fed's assessment of the US economy that began with the reduction in the growth, inflation and rate estimates in the December Projection Materials, introduced patience "as it [the FOMC] determines what future adjustments to the target range for the federal funds may be appropriate..." in the January statement and continued in March where "economic activity has slowed from its solid rate in the fourth quarter", will be the main point of interest in the record of the discussions at the first Fed meeting of this year.

Federal Reserve rate policy is not in question. The vote to maintain the 2.25%-2.50% target range, extant after the 25 basis point hike in December was unanimous at the January and March meetings.

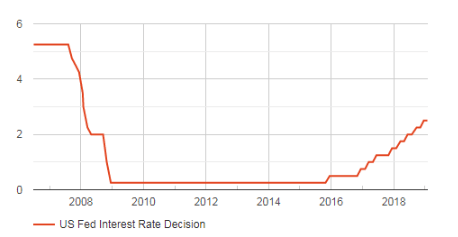

Fed Funds Rate Upper Target

FXStreet

Since Chairman Powell's press conference after the December 19th meeting where he stressed the external risks to the healthy US economy, hints of a wider condition have crept into the FOMC statement. In January household spending was said to have "continued to grow strongly" while "business fixed investment has moderated from its rapid pace earlier in the year.” Job creation has been, "strong, on average in recent months."

In the March statement six weeks later the labor market remained firm "job gains have been solid, on average in recent months...." But now "Recent indicators point to slower growth in household spending and business investment in the first quarter." Inflation which had been near 2% in the overall and core numbers in January was lower overall in March "largely as a result of lower energy prices", 'inflation for items other than food and energy remains near 2%."

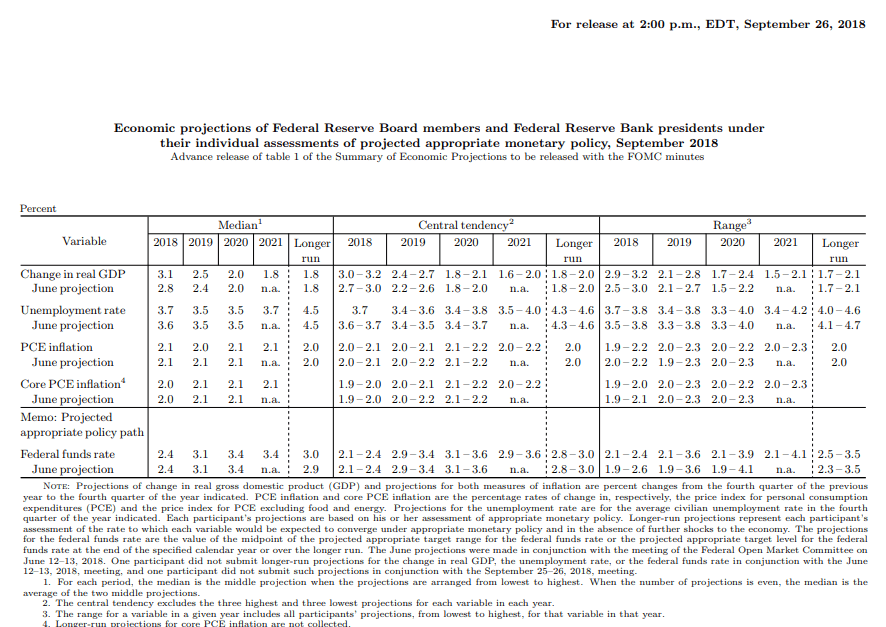

Federal Reserve Projection Materials

The outlook for the US economy in the Projection Materials has declined substantially in six months.

Last September the expectations for 2019 were GDP at 2.5%, core PCE at 2.1% and the year-end fed funds rate at 3.1%. By December those forecasts had dropped to 2.3% for GDP, 2.0% for core PCE and 2.9% in the fed funds rate. The slippage continued in March with 2.1% for GDP, 2.0% for core PCE and 2.4% for the Fed Funds rate at the end of 2019.

The Fed issues a new statistical assessment of the US economy four times a year in March, June, September and December. This incorporates the “Economic projections of Federal Reserve Board members and Federal Reserve Bank presidents.” The graphic representation of the projections for the fed funds rate is the source of the well-known ‘dot plot’ for future interest rate policy.

The change in the Fed’s estimate for interest rates has been rapid. It has dropped 0.7% in six months from 3.1% in September to 2.4% in March while the economy was expected to cool just 0.4% from 2.5% to 2.1%.

This change is, however, in line with previous policy projections that anticipated a halt to rate increases when GDP dropped to 2.0% annually.

In the September 2018 projections GDP was forecast to fall to 2.0% in 2020 from 2.3% in 2019 and then to 1.8% in 2021. As GDP fell to 2.0% in the out years the interest rate increases ceased. Both 2020 and 2021 were projected at 3.1% in the fed funds rate. The rate pause that began after the December FOMC was predicted by the September materials.

September 2018 Projection Materials

The Logic of Patience

The wording in the January and March FOMC statements around idea of rate patience and its conditions was identical. “In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes… This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

Chairman Powell has been at pains in his press conferences after the last two FOMC meetings to stress the health of the US economy. But despite its quoted strength Fed rate policy has undergone a drastic shift in the last half year.

The origins and opinions of the board members around this change and the potential for a further reduction in US economic prospects and perhaps a rate cut before the end of the year will be the main interest in the minutes. The more evident the concern the worse for the dollar.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)