FOMC minutes dash hope for future rate cuts, trade deal worries send equities plunging

Federal Reserve officials appear to be unanimous that further rate cuts are unnecessary to support the economy.

The minutes of the October 29-30 Federal Reserve Open Market Committee (FOMC) meeting showed that most likely all eight members who voted in favor of the 0.25% cut thought it was sufficient to keep the expansion intact. Combined with the two members who voted against this and the two prior cuts that would mean that all ten voting members of the present board thought accommodation had run its course.

“With regard to monetary policy beyond this meeting, most participants judged that the stance of policy, after a 25 basis point reduction at this meeting, would be well calibrated to support the outlook of moderate growth, a strong labor market, and inflation near the Committee’s symmetric 2 percent objective and likely would remain so as long as incoming information about the economy did not result in a material reassessment of the economic outlook,” noted the minutes.

Not surprisingly these opinions match Chairman Jerome Powell’s remarks in Congressional testimony last week.

“We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook of moderate economic growth, a strong labor market, and inflation near ...our 2 percent objective,” Chairman Powell declared in his prepared statement.

“There is no reason this expansion can't continue and there is a lot of value in it...income gains are highest at the lowest end of the wage scale...there is a lot to like about this rare place in the 11th year of this expansion,” said Mr. Powell in his testimony.

On Monday Chairman Powell met with President Trump and Treasury Secretary Steven Mnuchin at the White House’s invitation in a discussion that the President described as “A good and cordial meeting.”

Mr. Trump has repeatedly criticized Mr. Powell and the Fed for not cutting rates more aggressively. In his speech to the Economic Club of New York he observed that the US is competing with nations who have negative interest rates.

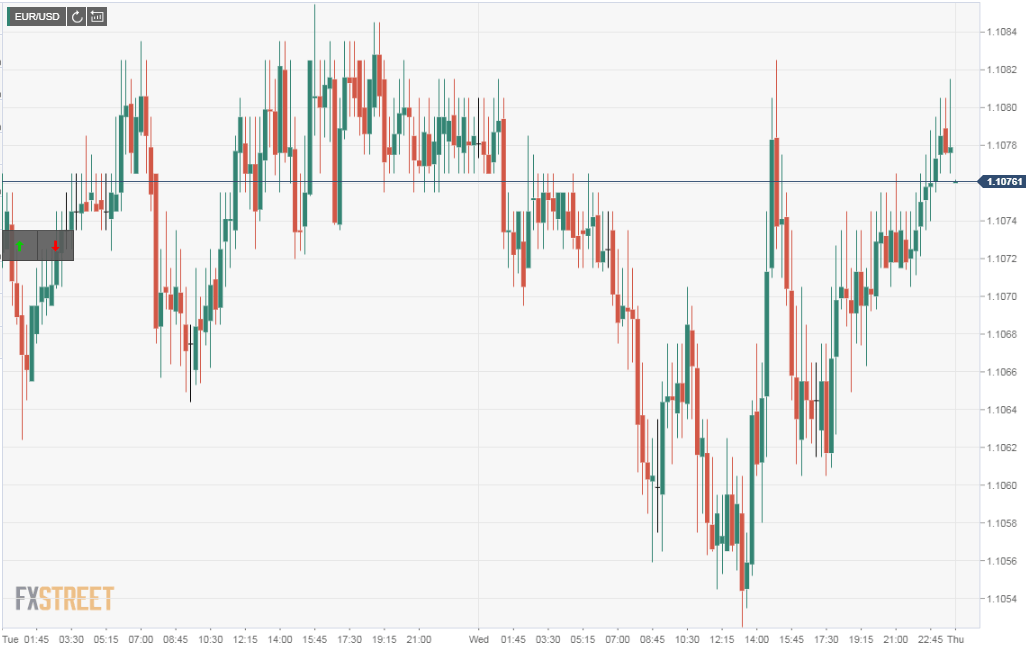

Currency markets did not respond to the elaboration of the Fed neutral policy with the euro closing on Wednesday at 1.1077 after a very tight 23 point range and just points from its Tuesday finish of 1.1074. The yen concluded at 108.57 on Wednesday and 108.55 on Tuesday.

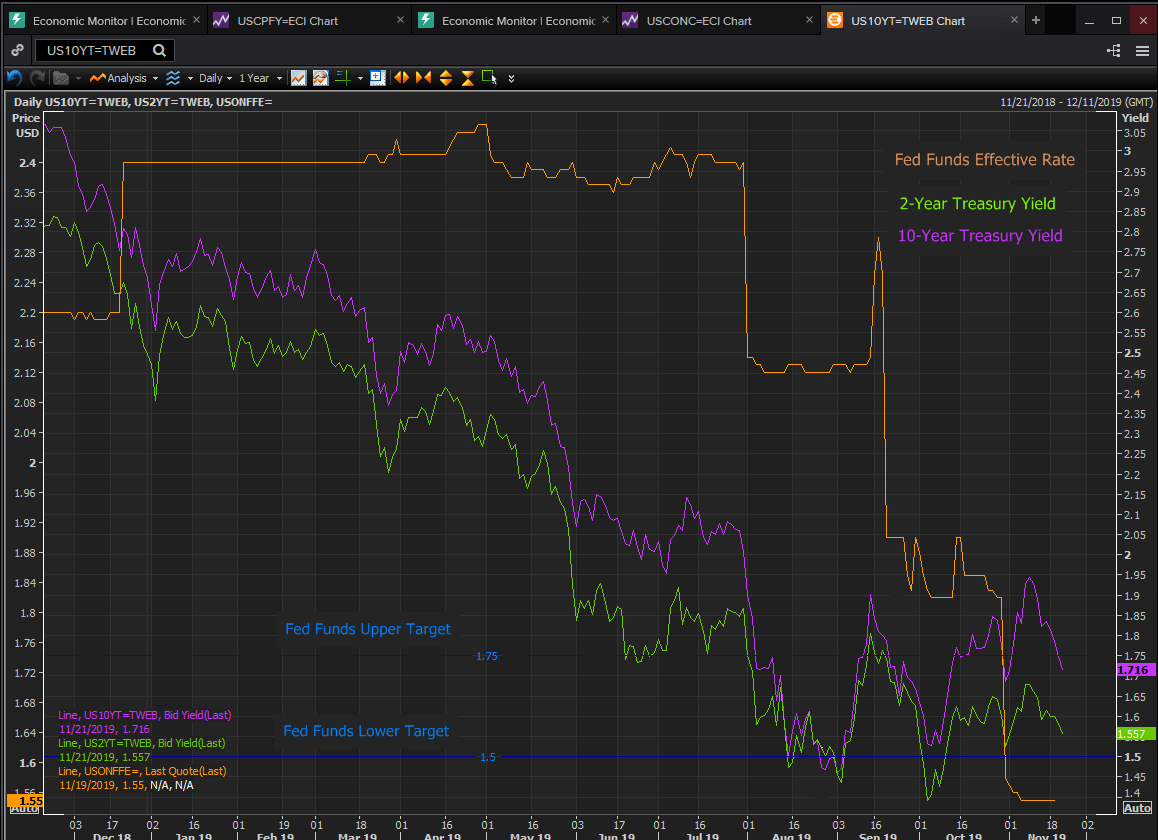

Credit markets were also becalmed with the yield on the generic 10-year Treasury shedding 2 points to 1.72% and the 2-year losing 2 points to 1.56%. Since its three month high of 1.94% on November 8th the yield on the 10-year benchmark has slipped 22 points and the 2-year yield has fallen 11 points.

Reuters

News reports that the US-China ‘phase one’ deal may not be completed this year sent equity markets sharply lower. At one point the Dow had lost over 250 points though the average closed with less than half that loss at 27,821.09 down -112.9, 0.40%. The S&P 500 lost 11. 72 points, 0.51%, to 3108.46.

Trade politics were further complicated by the U.S. Congress which passed a Hong Kong rights bill by a vote of 417-1 in the House and unanimously in the Senate. President Trump is expected to sign the bill.

Chinese officials said their government “firmly” opposes the bill calling it a grave violation of international law.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.