Five reasons why Trump’s trade war is likely to escalate

Buoyant markets, a resilient US economy, rising customs revenues, appeasement by trading partners and conducive politics point to further escalation in US trade tensions, already set to cut global output by an estimated 0.7pps in the medium term.

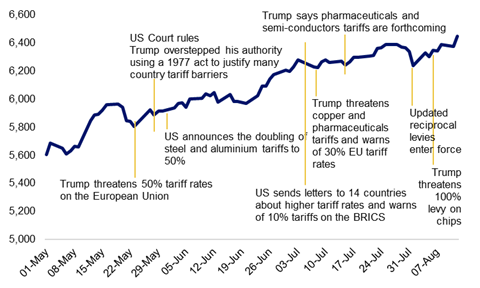

1. Markets encourage risk taking. With US equities at or near record highs, there is space for President Donald Trump to risk some unpopularity. One of the primary checks on his presidency is the stress his policies place on the capital markets. Market sell-offs are inevitably met with exercise of the “Trump put”. Markets are growing complacent to US trade escalations and de-escalations and are increasingly sanguine around the economic consequences.

Loosening the market straitjacket raises the risk of escalations in trade conflicts. Financial market volatility is near multi-year lows, suggesting markets no longer view the 15%-20% blanket duties floated recently by Trump as a penalty but as the new normal.

Investors in US equities take recent trade announcements, threats in their stride

S&P 500 Index, price

Source: S&P Global, Scope Ratings

2. US economy resilient. Second quarter GDP rebounded 0.7% quarter-on-quarter and the normally dependable GDPNow model suggests positive US growth in Q3. While Scope Ratings (Scope) has reduced its 2025 growth forecast on the US to 1.8%, this is higher than growth across most advanced economies. Scope has raised 2026 US growth to 2.1%. Although current tariffs are much higher than in recent decades, they are not high enough to impose effective embargoes on imports or cause severe economic losses. In addition, price rises from higher trade barriers have taken longer than anticipated to meaningfully lift inflation.

3. Rising customs revenues are helping to trim the US budget deficit. US Treasury data point to customs duties increasing to a record USD 66bn in Q2, with a further USD 28bn collected in July. This compares with monthly averages of less than USD 7bn last year. This revenue helps trim the burgeoning US general government deficit, which Scope estimates at an elevated 5.4% of GDP this year.

4. Trading partners’ responses have been limited and bilateral. Despite the many threats of reprisals, only China and Canada have significantly countered US tariffs. Many other governments including the UK and those in the EU have been wary of harming multilateral trading rules and global supply chains as well as the weaker growth and higher prices from any escalation. Trading partners have responded rather by pledging more than USD 1trn of investment in the US to appease Trump and de-escalate, while slashing duties on US imports and facilitating market access for US goods.

Reliance on US security guarantees – and Washington’s willingness to withhold them – has compelled many countries, including in the EU, to give some ground. Trump’s preference for bilateral rather than multilateral negotiations has limited any reprisals and encouraged competition within regional clusters for preferential trading terms with the US. As long as the responses of trading partners remain bilateral rather than multilateral, a trade war favours the US.

The widening gap between tariffs imposed by the US and those imposed by trading partners on the US as well as on one another has created a two-tier global trading system that may strengthen relative trading terms for the US in the longer run – helping to curtail annual trade deficits.

5. Conducive domestic politics currently favour escalation. Republican Party concerns about major losses in 2026 mid-term elections have eased as the president’s approval rating remains around 90% with his party’s voters. The passage of the “Big Beautiful Bill” has bolstered the president’s political capital.

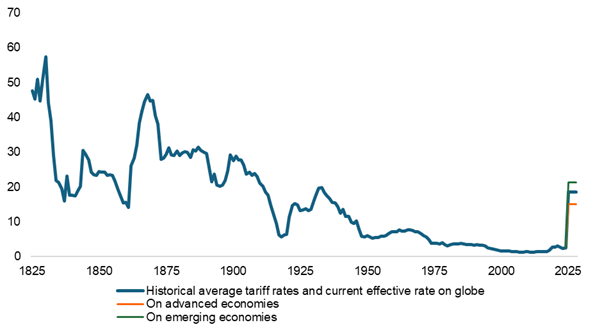

Average duties at multi-decade highs cut global output

Average US customs duties have risen sharply to 18.6%, up from the 2.5% at the end of 2024 and 1.5% in 2016 ahead of Trump’s first administration. While current tariffs remain off the “Liberation Day” highs of nearly 30%, they are still at their annual highs since the 1930s. This includes 15% average duties on advanced-economy trading partners and 21.4% on emerging economies.

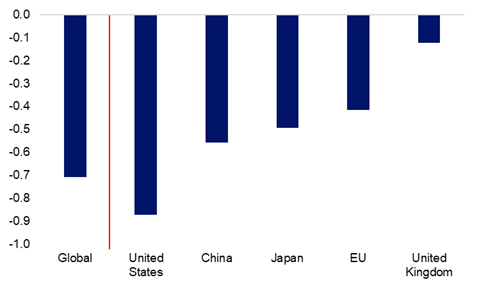

This has consequences for the global economy: Scope projects a cumulative medium-term reduction in global output of 0.7pps. The effects on the US economy are only slightly greater, at 0.9pps, as re-shoring gradually trims the cumulative costs. More modest consequences are estimated for the EU economy, at 0.4pps. Scope has reduced 2025 global growth by 0.4pps to 3.0%.

US average tariff rate on all imports (%)

Historical average tariff rates are from Tax Foundation. The 2025 current effective tariff rate is based on the Yale Budget Lab estimate assuming tariffs as of 7 August 2025. Weighted averages for advanced and emerging economies are based on Scope estimates. Average tariff rate estimates for 2025 are on pre-substitution bases not accounting for consumption shifts. Source: Tax Foundation, The Budget Lab at Yale University, Scope Ratings.

Trade tensions cause 0.7pp hit to the global economy

Cumulative impact on real output (percentage-point change) assuming current levies.

Note: this scenario for the effects of US levies on the global economy is based on the measures already in force or announced since the beginning of Trump’s second administration and the countermeasures from trading partners, including the agreements announced between the US and its trading partners. Source: Scope Ratings.

(Arne Platteau, analyst in credit policy at Scope Ratings, contributed to drafting this research)

Author

Dennis Shen

Scope Ratings

Dennis Shen is Chair of the Macroeconomic Council and Lead Global Economist of Scope Ratings, the European rating agency, based in Berlin, Germany.