Five fundamentals for the week: Nonfarm Payrolls return to the throne with a big buildup

- The US labor market returns to center stage after the Federal Reserve's pivot away from inflation.

- Friday's Nonfarm Payrolls are preceded by a full buildup of critical data points.

- Volatility is set to increase as traders return from their summer holidays.

"The King of Indicators" – for a couple of years, Nonfarm Payrolls (NFP) lost its claim to the throne as inflation was in the spotlight. After Jerome Powell, Chair of the Federal Reserve (Fed), basically declared victory on rising prices, the jobs report fully deserves the throne. This time, the intense buildup and the end of summer holidays means high volatility.

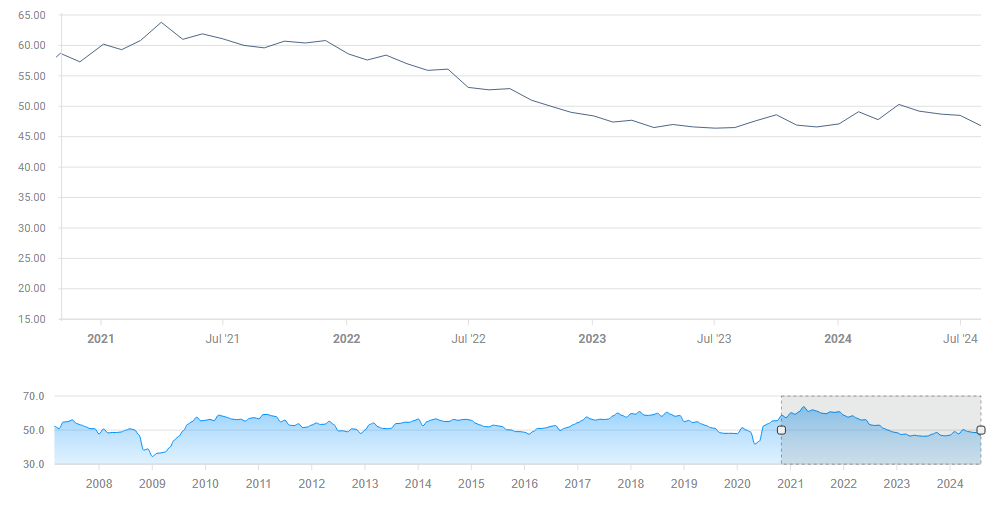

1) ISM Manufacturing PMI to trigger high volatility

Tuesday, 14:00 GMT. While this release is for the smaller industrial sector, the ISM Manufacturing Purchasing Managers Index (PMI) for August is the first significant release after the long Labor Day weekend, providing an initial indication of the market mood. Volatility will likely be high.

The economic calendar points to an improvement from July's poor 46.8 read, significantly below the 50-point threshold separating expansion and contraction. Stock markets need a "Goldilocks" number – not too hot nor too cold.

ISM Manufacturing PMI. Source: FXStreet.

A small improvement would boost stocks while shoring up the US Dollar (USD) and marginally weighing on Gold. The precious metal needs weak data to advance.

The market reaction to this figure – for instance, if stocks rally in any case, or if Gold remains capped – would serve as a hint for the next few days.

2) JOLTs gain more attention after Powell's speech

Wednesday, 14:00 GMT. Fed Chair Jerome Powell clearly said that the labor market matters – so even a data point for July rather than August is of high importance. Job openings stabilized at 8.18 million annualized in June, showing that the decline in hiring has come to a halt.

Economists see a fresh slide reported for July, and any big fall would scare investors, reviving recession fears.

I expect another upside surprise, cheering stocks and the US Dollar but weighing on Gold.

3) ADP NFP and Unemployment Claims to cause choppy trading

Thursday: ADP's private-sector jobs report at 12:15 GMT, initial jobless claims at 12:30 GMT. The long weekend of Labor Day has pushed ADP, America's largest payrolls provider, to publish its data on Thursday. That adds to market choppiness, as weekly jobless claims are published only 15 minutes afterward.

ADP's data is considered a leading indicator toward the official Nonfarm Payrolls report on Friday, but the correlation between the two is poor. Moreover, moves triggered by ADP are often reversed.

If both releases exceed estimates, they could have a positive effect on the US Dollar and an adverse one on Gold. Conversely, a double miss would do the opposite. However, there is a good chance that the outcomes are close to expectations – and that one is a beat and the other is a miss.

I think that trading around this time would be messy, but if a trade must be taken, I think it would be best to go against the initial move – a mean-reversion move.

4) ISM Services PMI serves as the last pre-NFP indicator

Thursday, 14:00 GMT. Less than 24 hours before the all-important jobs report hits the screens, this forward-looking gauge of the services sector – America's largest – will likely trigger significant price action.

The ISM Services PMI has been swinging above and below the 50-point threshold in recent months, reflecting uncertainty about the future of the economy. After hitting 51.4 points in July, it is expected to hold onto similar levels.

Apart from the headline, the employment component is also of high importance. Markets are set to respond to the headline first, then the employment component. In case they go in the opposite direction, a whipsaw is likely in markets.

It is essential to note that the focus is now on the labor market.

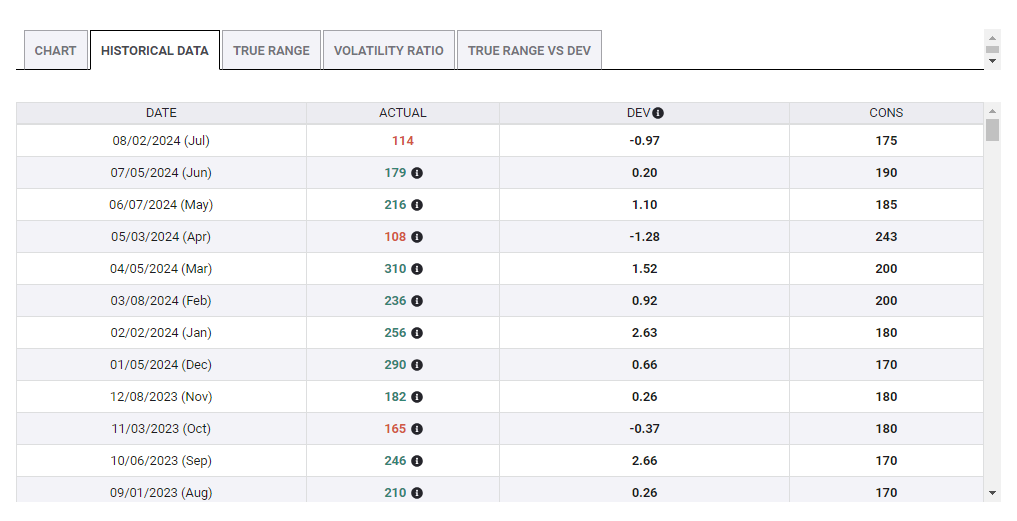

5) Nonfarm Payrolls carry more weight than usual

Friday, 12:30 GMT. Single or double shot? The Fed pledged to cut rates in September, but it left markets wondering if it will go for the standard 25 bps cut or a double dose of 50 bps. Chair Powell stressed that he will do whatever is necessary to support the labor market.

July's report was poor: only 114K jobs were gained in America. A bounce to above 150K is on the cards now – but these expectations may shift in response to the leading indicators mentioned above.

Nonfarm Payrolls. Source: FXStreet

Five Scenarios for the NFP

1. Investors desire an outcome of 150K-200K, which would allow rate cuts without recession fears. That would weigh on the US Dollar while boosting Gold and stocks.

2. An increase of 200K-250K jobs would lower expectations of a 50-bps cut, buoying the US Dollar and weighing on Gold but keeping strong support.

3. An outcome above 250K would already cause some to doubt the Fed will enter a consistent rate-cutting cycle, sending stocks and Gold lower, while supporting the US Dollar.

4. A disappointing 100K-150K figure would be somewhat disappointing, but it would increase the chances of a double-dose rate cut, boosting Gold and hurting the US Dollar. Stocks would skid, but not collapse.

5. Any sub-100K number would already cause recession worries. While Gold would benefit, the US Dollar could stage a rally triggered by safe-haven flows. Stocks would shiver.

Final thoughts

The fresh crowning of Nonfarm Payrolls as King does not imply orderly trading. Fresh from the long weekend – and summer vacations – investors could make conditions hazardous. Trade with care.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)