Five fundamentals: Fallout from the US election, inflation, and a timely speech from Powell stand out

- Control of the US House and the Middle East will likely send market shockwaves.

- US inflation and retail sales data are set to show the ongoing health of the US economy.

- Fed Chair Powell will speak and may comment on recent developments.

What a week – the US election lived up to their hype, at least when it comes to market volatility. There is no time to rest, with politics, geopolitics, and economic data promising more volatility ahead.

1) Control of the House matters for tax cuts

Donald Trump will return to the White House, and his Republican party clinched a clear majority in the Senate. However, votes in close races for the House of Representatives are still counted, and it is unclear if the Grand Old Party (GOP) will gain a majority there.

If a Republican sweep is confirmed, it will mean fresh tax cuts that benefit stocks and could mean more money sloshing around and chasing Gold.However, it would also imply higher interest rates, as the government's borrowing needs would rise. Elevated yields benefit the US Dollar (USD).

If Democrats claw onto the lower chamber, most of Trump's policy would be in tariffs – which markets dislike. It would be adverse for stocks and would weigh on Gold.

At the time of writing, Republicans have a better chance of winning the House.

2) Middle East cooldown or warmup?

Jared Kushner, President-elect Trump's son-in-law, served as an envoy to the Middle East in the previous administration. Kushner – a staunch supporter of Israel, is married to Ivanka Trump. The politician's other son-in-law is Michael Boulos, who married Tiffany Trump and is of Lebanese descent. Michal and his father, Massad Boulos, played a role in convincing some Arab Americans to vote for Trump.

Will these family connections help stabilize the Middle East? Hope boosts markets and weighs on the prices of Oil and Gold.

On the other hand, Qatar has recently suspended its mediating role between Israel and Hamas, accusing both sides of failing to negotiate in good faith. In addition, Iran has vowed revenge for Israel's attack on it in October. An escalation in the crisis would benefit commodities.

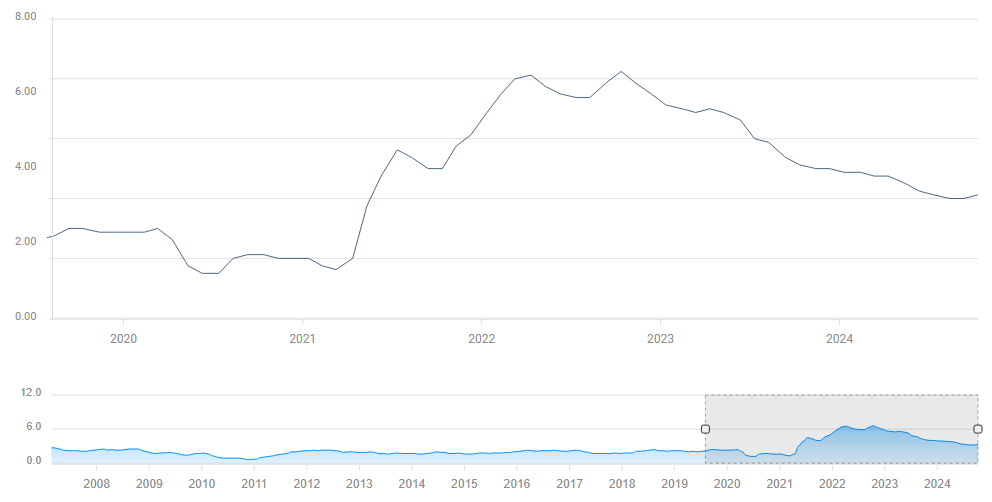

3) US inflation set to hold steady

Wednesday, 13:30 GMT. Close, but no cigar. US inflation has dropped significantly from its highs but has yet to hit 2%. The Consumer Price Index (CPI) report is the first release of hard inflation data, and it is set to show a small increase in headline prices, from 2.4% to 2.6% year-over-year (YoY) in October.

More importantly, core CPI – which excludes volatile food and energy prices – is projected to stick to the 3.3% recorded in September. The Federal Reserve (Fed) and investors watch this figure more closely, as underlying inflation impacts interest rate expectations.

US core CPI YoY. Source: FXStreet.

The monthly core CPI is the most market-moving figure, and a reading of 0.3% is on the cards. Weaker inflation would send US Treasury yields down, boosting Gold and stocks while weighing on the US Dollar. A hotter print would do the opposite.

4) Fed Chair Powell may comment on inflation

Thursday, 20:00 GMT. The biggest headlines from Fed Chair Jerome Powell's post-rate cut presser were related to politics – he said he would refuse to resign if the president asked him to. Powell was relatively tight-lipped on the economy, dodging any questions about the next move in December or the path in 2025.

In a panel discussion in Dallas, the Fed Chair may feel more relaxed to share fresh views, and he will have the chance to comment on the CPI report.

If Powell expresses worries about the labor market, it would weigh on stocks and the US Dollar while supporting Gold. Concerns about inflation would weigh on the precious metal and equities while buoying the currency. Stock investors need his confident message.

5) US Retail Sales will likely show shoppers on a roll before Black Friday

Friday, 13:30 GMT. Roughly two-thirds of the US economy is centered on consumption, making this report critical. Moreover, Fed Chair Jerome Powell highlighted this component as an engine of growth.

In the past few months, shoppers were on a roll. In September, the retail sales control group – which focuses on the most non-volatile items – shot up by 0.7%.

The economic calendar points to a moderate 0.3% expansion in headline sales in October, a tad below 0.4% recorded in the previous month. A better figure would add oomph to stocks and the US Dollar while weighing on Gold. A soft figure would do the opposite.

In the past few years, holiday season shopping – which begins with Black Friday – fell below estimates. A robust number now would provide a shield against relatively softer sales toward year-end.

Final thoughts

The election is over, but uncertainty about Trump's policies at home and abroad will likely remain high on the agenda before and also after his inauguration.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.