Fitch slashes FY23 India growth forecast to 8.5% on high energy prices

Global developments

Most Fed members, even the relatively more dovish ones seem to be in favour of a speedier increase in rates. Even a 50bps hike is on the table in forthcoming meetings. This has caused markets to run further ahead with its expectations of hikes after it seemed the Fed dots were aligned with markets after the Fed policy last week. The markets at this stage seem to be confident about the growth and the ability of the economy to withstand higher rates. Uncertainties to growth however persist as no resolution in the Russia-Ukraine conflict seems to be in sight. President Biden is to meet allies in Europe tomorrow and we may see fresh sanctions being imposed on Russia.

Price action across asset classes

The global bond sell-off continues. US yields have risen about 8bps in the 5-30y segment. The difference between the 30y and 5y US yields is the lowest since 2007. The difference between 2y US and German yields is the highest since mid-2019. Surging US yields has pushed USDJPY higher. It has now crossed the 121 mark. Commodity currencies continue to rally with the Australian Dollar now approaching 75 cents against the Dollar. The S&P500 ended 1.1% higher. Asian equities are trading with gains of anywhere between 0.5%-2%.

Domestic developments

Rating agency Fitch has lowered India's growth forecast for FY'23 to 8.1% from 10.3% on sharply higher energy prices. OECD estimate stands at 8.1%.

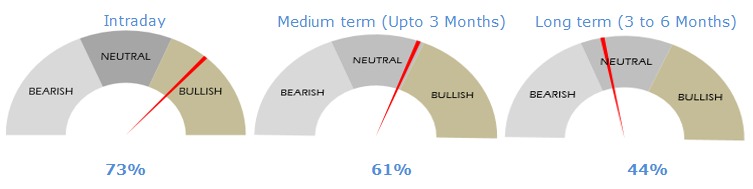

Equities

Domestic equities reversed intraday with Nifty managing to end 1.1% higher at 17315. We see the Nifty trading 16800-17600 range over the next few sessions.

Bonds and rates

The yield on the benchmark 10y rose 5bps to 6.83% yesterday, tracking the up move in US yields and higher crude prices. 10y SDL cutoffs were around 7.23%. 5y OIS ended 10bps higher at 6.01% on higher crude prices.

USD/INR

USD/INR opened higher on higher crude prices but got resisted in the 76.45-76.50 zone (despite aggressive buying at fix) as nationalized banks were likely selling Dollars there on behalf of RBI. Thereafter a PSU bond-related inflow caused USD/INR to come off. Reversal in equities too improved sentiment with Rupee finally ending at 76.18. 1y forward yield ended 5bps lower at 3.83% as interest differentials between US and India further compressed after a sharp up move in short term US rates. 3m ATMF implied vols ended at 6.07%.

Strategy

Exporters are suggested to cover only confirmed positions. For any extra covers based on expectation, we suggest keeping stoploss of 75.80 till the panic subsides. Importers cover through options or on dips. The 3M range for USDINR is 74.00–77.00 and the 6M range is 73.80–77.30.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.