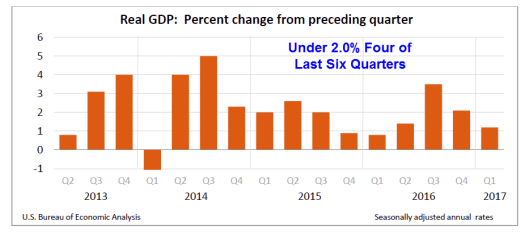

First Quarter GDP Second Estimate 1.2 Percent: Mish vs. Consensus

This morning, the BEA revised its estimate of first-quarter GDP to 1.2% from 0.7%. The Econoday consensus estimate was 0.8%, in a range of 0.7% to 1.0%.

I posted this tweet ahead of the report.

I was higher than any Econoday economist’s estimate, yet they call me a pessimist.

Econoday Comments

First-quarter GDP gets a small but much-needed upgrade, now at a 1.2 percent rate of annualized growth which is nearly double the advance estimate. The gain is centered where it is best, in consumer spending where the rate did double to 0.6 percent. This is still slow but is an improvement with durable goods, at minus 1.4 percent, showing less contraction and services showing greater growth, at 0.8 percent.

Boosted by strong and sudden acceleration in both structures and equipment, nonresidential fixed investment is also upgraded, to 11.4 percent for a 2 percentage point gain. Government purchases are also upgraded, down 1.1 percent for a 6 tenths improvement that pulls less on GDP. Other readings are stable with a slowing build in inventories still a major negative (a negative for GDP but not for the second-quarter outlook).

But the second-quarter outlook, which was once very positive, is mostly in question following a run of weak data for April including this morning’s durable goods report. And the first-quarter is a little less of an easy comparison now for the second quarter where early estimates, once as high as 3 and 4 percent, have been coming down to the 2 percent area.

GDP Second Estimate Revisions

Gross Domestic Income

Real gross domestic income (GDI) increased 0.9 percent in the first quarter, in contrast to a decrease of 1.4 percent (revised) in the fourth. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, increased 1.0 percent in the first quarter, compared with an increase of 0.3 percent in the fourth quarter.

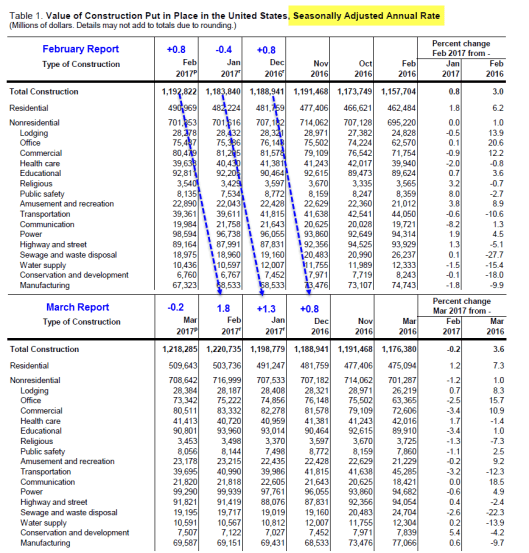

Construction Spending

On May 1, I commented on Weather-Related Effects on Construction Spending. Here is a snip I posted.

March Revisions vs February

Revision Synopsis

- December: Unrevised at 1,188,941 Hooray!

- January: Revised from 1,183,840 to 1,198,779

- February: Revised from 1,192,822 to 1,220,735

The January revision from -0.4 to +1.3 was even larger than the positive revision in February.

If we just compare February as reported in February to February as reported in March, the percentage increase is 2.3%, not reported 1.8% as the revisions build on each other.

Weather Effect?

This was a strong report and even stronger than it looks at the first glance. However, I caution everyone to not read too much into this strength.

December was unusually cold. January was unusually warm as was February. Seasonal adjustments do not factor in weather.

First Quarter Comments

I was quite confident that first quarter GDP was stronger than reported because of construction spending. I was also quite confident it would cause models for second quarter to go haywire.

Indeed, that is exactly what happened. The GDPNow model for second quarter jumped all the way to 4.2%, an extremely unrealistic estimate prompting my usual comment “I will take the under, way under.”

Curiously, it appears not a single economist factored in the massive upward revisions to construction spending in their second estimate for first-quarter GDP.

Second Quarter Reality

- Wholesale Inventories: Down 0.3% in April. March revised lower from 0.2% to 0.1%.

- Retail Inventories: Down 0.3% in April. March revised lower from 0.5% to 0.3%.

- Trade deficit in April widens by 3.8% with exports down and imports up: Trade Deficit Widens, Exports Weak: Economists Miss the Mark

- Tax Receipts: Federal Tax Receipts Running Below Expectations

- April New Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: Spring Housing Flop: Existing Home Sales Decline 2.3 Percent, Inventory Issues Persist

- April Housing Starts: About that Strong April Recovery: Housing Starts and Permits Flop, March Revised Lower

- April Empire State Manufacturing Survey: Empire State Manufacturing Survey Turns Negative: Welcome News?

- April Retail Sales: Sales were at least positive (+0.4%), but they were well under economists projections: Retail Sales Disappoint Again: Department Stores Clobbered in 2017

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc