Firm US bond yields lifts DXY, Euro stays anaemic, Aussie bounces

Dollar Soars vs JPY, CHF; Stocks Rebound as Omicron Fears Ease

Summary: A weaker than expected read on the Eurozone Sentix Investor Confidence, a diffusion index which is a leading indicator of economic health weighed on the already anaemic Euro. The shared currency slid 0.22% against the US Dollar to 1.1280 (1.1307 yesterday). This lifted the Dollar Index (DXY), where the Euro has almost 60% of the weight, to 96.30 from 96.17, up 0.15%. In the bond markets, interest rate traders bolstered bets on a faster pace of Fed rate increases by pushing US treasury yields higher. The benchmark US 10-year bond rate rebounded 8 basis points to 1.42%. Other global treasury yields were little changed, or even lower. The Dollar Yen pair (USD/JPY), most sensitive to moves of the USD 10-year yield, soared 0.74% to 113.45 from 112.75 yesterday. Against the other low yielder, the Swiss Franc, the Greenback (USD/CHF) rose 1.18% to 0.9258 (0.9180)

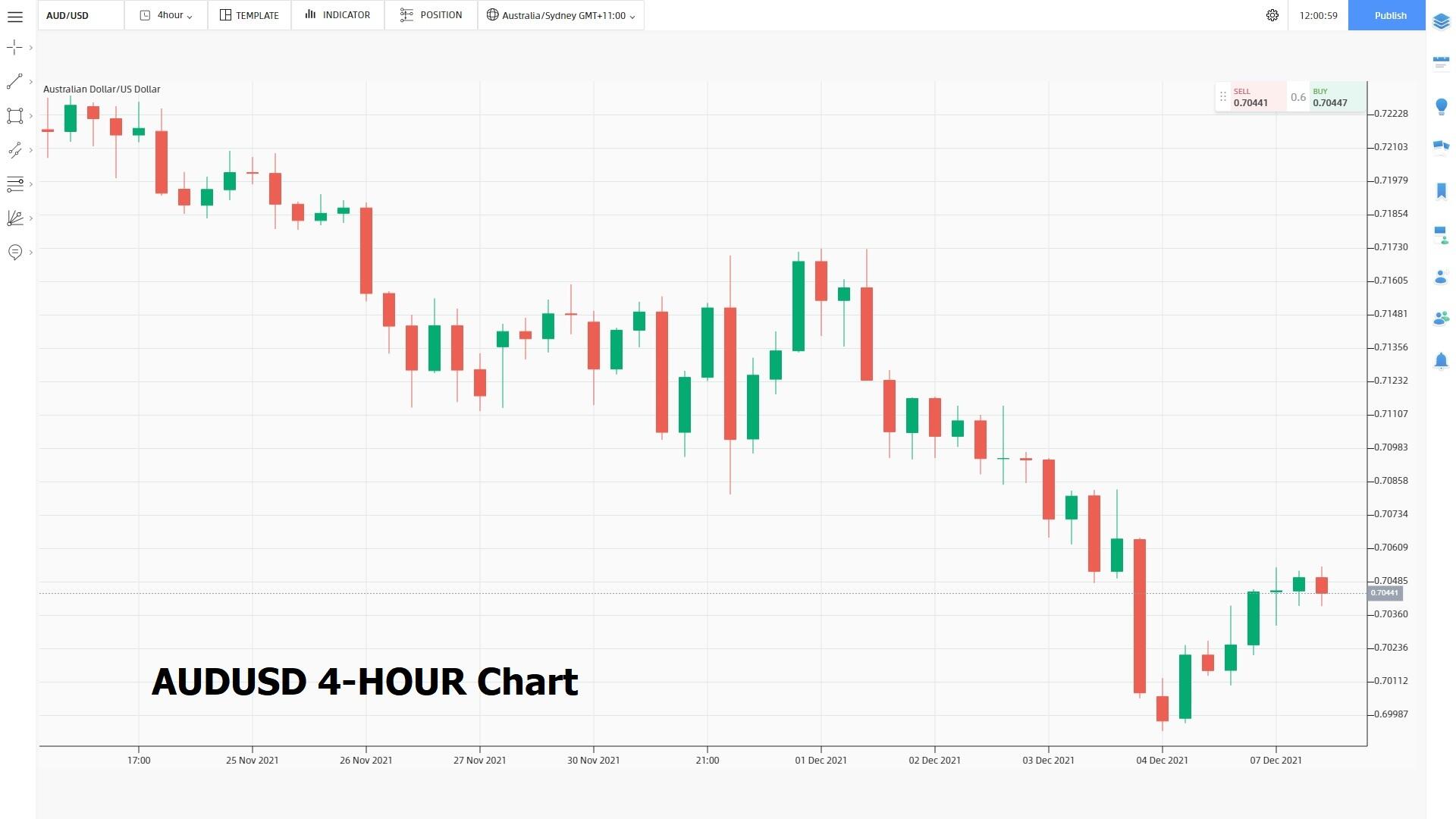

However, the Greenback’s rally was not uniform. The Aussie Dollar (AUD/USD) bounced off the psychological 0.70 cent level after China’s central bank (People’s Bank of China) cut its reserve requirement ratio (RRR) for banks by 50 basis points (weighted rate to 8.4%). Commodity prices rose and the AUD/USD pair settled at 0.7040 (0.7000 yesterday). Aussie short bets were also forced to cover ahead of today’s RBA interest rate policy meeting (2.30 pm Sydney). Higher Oil prices saw the USD/CAD (US Dollar-Canadian Dollar) ease 0.37% to 1.2771 (1.2837). Elsewhere, the British Pound (GBP/USD) rallied 0.39% to 1.3253 from 1.3235. The Greenback was mixed against the Asian and EMFX pairs. USD/SGD (US Dollar-Singapore Dollar) dipped to 1.3695 (1.3705), while USD/CNH (US Dollar-Offshore Chinese Yuan) edged up top 6.3757 from 6.3735.

Wall Street stocks rebounded as fears on the Omicron variant eased following reports from South Africa (where it originated) of only mild symptoms. The Dow soared 1.87% to 35,212 (34,550) while the S&P 500 settled at 4,592 from 4,532, up 1.27%.

Data released yesterday saw Germany’s Factory Orders fall to -6.9%, missing forecasts at -0.2%. The Eurozone Sentix Investor Confidence Index eased to 13.5 for December from 18.3 in November, and lower than estimates at 14.5. UK Construction PMI rose to 55.0 in November, up from October’s 54.6, and bettering median expectations at 53.0.

- EUR/USD – The shared currency extended is anaemic performance sliding to 1.1280 at the close of trading in New York (1.1307 open yesterday). Overnight the EUR/USD pair slumped to a low at 1.1266 before stabilising. Overnight high traded was at 1.1311.

- AUD/USD – The Aussie Battler bounced off its overnight low traded at 0.6993 after the People’s Bank of China cut its RRR by 50 basis points. A rebound in commodities also lifted the AUD/USD pair to finish at 0.7040 from 0.7000 yesterday.

- USD/JPY – against the Japanese Yen, the Greenback surged to an overnight high at 113.55 from its 112.75 opening yesterday. The eight-basis point rally in the benchmark US 10-year treasury yield boosted the Greenback against the yield sensitive Japanese Yen. Japan’s 10-year JGB rate was unchanged, at 0.04%.

- GBP/USD – unlike the Euro, the British Pound finished stronger against the Greenback. Sterling was last at 1.3253 from yesterday’s 1.3235 opening. Overnight the GBP/USD pair traded to a high at 1.3286 on short covering and position adjustment.

On the Lookout: Today’s economic calendar picks up with the focus on the RBA’s monetary policy meeting (2.30 pm Sydney), which is today’s main event. Data releases kicked off earlier today with Australia’s AIG Services Index, up to 49.6 for November from a previous 47.6. The Aussie Dollar rallied 10 points to its current 0.7050 after the number was released. Japan follows with its October Household Spending (m/m f/c 3.6% from 5.0%; y/y f/c -0.6% from -1.9% - ACY Finlogix). The US follows with its November Total Vehicle Sales (no f/c, previous was 12.99 million). The UK releases its BRC Retail Sales Monitor for November (y/y no f/c, previous was -0.2%).

Australia releases its Final October Building Permits (f/c -12.9% from -3.9% - ACY Finlogix), Australian House Price Index (q/q no f/c, previous was 6.7%; y/y no f/c, previous was 16.8%). China follows next with its Trade Balance (CNY 372.2 billion from CNY 545.98 billion; USD 82.75 billion from USD 54.54 billion). The RBA is not expected to change its Overnight Cash Rate of 0.1%. European data kicks off with Switzerland’s November Unemployment Rate (f/c 2.6% from 2.7% - FX Street), UK November Halifax House Prices (m/m f/c 0.6% from 0.9%, y/y f/c 9.4% from 8.1% - FX Street). Germany releases its October Industrial Production (m/m f/c 0.7% from -1.1% - ACY Finlogix), French October Trade Balance (no f/c, previous was -EUR 6.78 billion). The Eurozone releases its 3rd GDP Estimate (q/q f/c 2.2% from 2.1%, y/y f/c 3.7% from 14.2% - ACY Finlogix), Eurozone Employment Change (q/q f/c 0.9% from 0.9%; y/y f/c 1.8% from 2.0%), Eurozone Q3 GDP (q/q f/c 2.2% from 2.2%; y/y f/c 3.7% from 3.7% - FX Street), Eurozone December Sentix Index (no f/c previous was 25.9). Germany releases its December ZEW Economic Sentiment Index (f/c 27.1 from 31.7 -ACY Finlogix). Canada kicks off North American data with its October Balance of Trade (no f/c, previous was +CAD 1.86 billion – ACY Finlogix). The US rounds up today’s data releases with its October Balance of Trade (f/c -USD 66.8 billion from -USD 80.9 billion – ACY Finlogix) and US NonFarm Productivity (q/q f/c -5% from 2.4% - ACY Finlogix). Canada releases its November Ivey PMI (no f/c, previous was 59.3).

Trading Perspective: Despite a rise in the DXY to 96.3 (96.17 yesterday), the Dollar’s rise was not broad-based. In fact, the USD fell against its other rivals (AUD, CAD, NZD, SGD). The weaker currencies remain weak, led by the anaemic Euro. Yield sensitive Japanese Yen and Swiss Franc were also lower against the Greenback. The Fed is expected to taper, and hike interest rates quicker than the other global central banks and this will give the Greenback overall support. Market positioning will have more of an impact as we head into next week and into the Christmas holidays. It’s a time to be flexible and nimble.

- EUR/USD – Overnight the Euro stayed anaemic, slumping to a low at 1.1266 before stabilising to its 1.1280 New York close. Immediate support lies at 1.1260 followed by 1.1230 and 1.1200. Immediate resistance can be found at 1.1310 (overnight high traded was at 1.1311). The next resistance level lies at 1.1340. Look for the shared currency to consolidate in a likely range today between 1.1260-1.1320. Selling rallies still the way to go but beware of short covering.

- AUD/USD – The Aussie Battler managed to bounce thanks to higher commodity prices and the PBOC’s 50 bp easing in its RRR. Overnight the AUD/USD pair slid to a low at 0.6993, bouncing to finish at 0.7040 in New York. Immediate resistance today lies at 0.6990 followed by 0.6960. On the topside, immediate resistance is found at 0.7055 (overnight high traded was 0.7054). The next resistance lies at 0.7085. The RBA meets today on policy and further dovish speak from officials (due to the recent spread of Omicron) would heap more pressure on the Battler. Look for consolidation in a likely range of 0.6980-0.7080. While the Aussie remains soft, would be wary of a typical December short covering bounce.

(Source: Finlogix.com)

- USD/JPY – The strong rebound in the Greenback against the Yen by 0.74% appeared orderly which should not alarm Japan Inc. The USD/JPY pair was last at 113.45 (112.75 yesterday). Overnight high traded was at 113.55. Immediate resistance for today lies at 113.60, followed by 113.90. Immediate support can be found at 113.10 and 112.80 (overnight low traded was at 112.79). Expect a likely range today of 113.00-113.60. Just trade the range shag.

- GBP/USD – Sterling had a good day, finishing up 0.39% against the US Dollar to 1.3253 (1.3235 yesterday). Overnight, the GBP/USD pair hit a high at 1.3286. Immediate resistance for today lies at 1.3285 followed by 1.3305. Immediate support can be found at 1.3220 followed by 1.3200 (overnight low traded was at 1.3202). Look for Sterling to trade in likely range today of 1.3220-1.3320. More neutral on GBP/USD, preference is to buy dips.

Happy trading and Tuesday all.

Author

Michael Moran

ACY Securities

Michael has over 40 years’ FX experience, including running FX trading desks for some of the largest banks in the world.