Few signs of slowing activity in the services sector

Summary

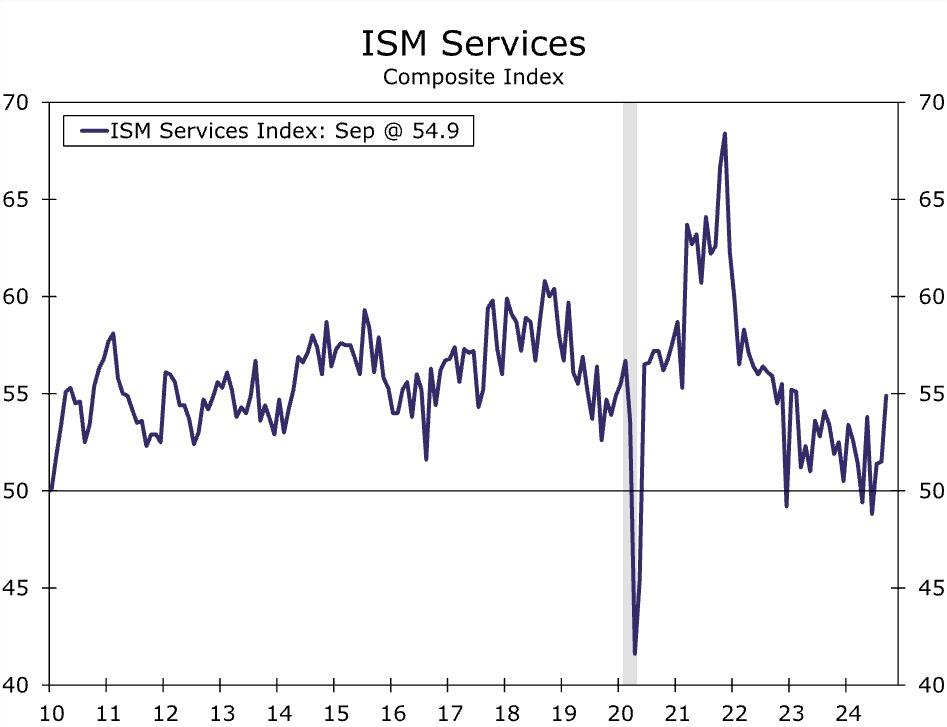

The ISM services index rebounded in September to the highest reading since February of last year. New orders and current activity signal steady conditions, but mixed messages from the jobs market will keep the Fed on high-alert.

Growth signs intact

The overall ISM services index rose to 54.9, the highest reading since February of last year (chart). The index was lifted by a few components, but the rise in the business activity and new orders components by over six points highlights that overall activity and demand conditions remain solid (chart). The three industries reporting declines in both of these components were the same (other services, agriculture and wholesale trade), signaling weakness remains relatively concentrated in the sector.

Select industry comments continued to reference stable growth conditions, but there was increased mention of uncertainty over the upcoming U.S. presidential election in November, similar to what we saw in the ISM manufacturing report earlier this week. Specifically, a respondent from the professional services industry said, “There is concern over the economy, and it feels like a lot of people are waiting to see which way the election goes in November before making a solid plan for 2025 and beyond.” This same industry last month made mention of challenges finding qualified labor saying, “...it is harder than ever to find talent, but less jobs available as well.”

Lower rates and the Fed's recent slash to the federal funds rate were also noted. A respondent from the finance & insurance industry cited lower rates starting to spur demand for housing and autos, while the construction industry was pleased to see rates cut but cited a need for rates to move much lower to spur sales growth.

In way of unfavorable developments was the rise in the prices paid measure and pullback in the employment component. Essentially both cuts of the Fed's mandate moved in the wrong direction, but not to a concerning degree. Price pressure still exists in the service sector even if it has eased. The prices paid metric rose to 59.4, and while that marks the highest in four months, it's well off pandemic-related highs and is roughly in line with the average index reading in the three years ahead of the pandemic (59.1). Still, 12 industries reported paying increased prices for inputs last month.

Perhaps the most mixed portion of this release continues to be the signal we get from the labor market. Most metrics of hiring are consistent with a jobs market that has fully normalized from pandemic-related distortions. Overall hiring has slowed and narrowed, job openings have eased, workers are not voluntarily departing from their jobs as much as they were and households don't feel there are nearly as many jobs as there were previously. The ISM employment components have teetered between expansion and contraction, and the employment component slipped below 50 again here in September, consistent with a contraction in service sector hiring (chart). But the release included the following comments: “Employees leaving, and it’s tough to find new ones” and “Head count, open positions and employee retention is about the same month over month.” There is no denying the labor market is moderating, but our read from the Services ISM is that it is not a uniform deterioration across industry. We get the full September employment report tomorrow, where we expect to see hiring holding up but continuing to show signs of moderation. While the service sector shows continued signs of growth, the Fed will remain on high-alert to any signs of more pronounced stress emanating from the jobs market and adjust policy accordingly.

Author

Wells Fargo Research Team

Wells Fargo