Feeling the squeeze [Video]

![Feeling the squeeze [Video]](https://editorial.fxstreet.com/images/Macroeconomics/EconomicIndicator/Prices/CPI/tablet-with-consumer-price-index-cpi-business-concept-gm499730392-80399281_XtraLarge.jpg)

The Day So Far

The hangover from last weeks decline in global indices appears to be lingering with equity markets in Europe following the lower close on Wall Street and negative session in Asia. At this point the pull back has been largely pinned on profit taking given the recent run to multi-year, if not record all-time highs, with some also noting long positions being closed as we head into the final few weeks of 2017. An interesting comment I saw yesterday in the BofAML global fund managers survey was that there are a record high percentage now saying that equities are overvalued, even as cash levels are falling, a sign of “irrational exuberance”. Certainly given the context of the importance of today’s US CPI and Retail Sales reports key downside levels in the US equity market will need to be watched closely and if broken may open up the potential for another run lower.

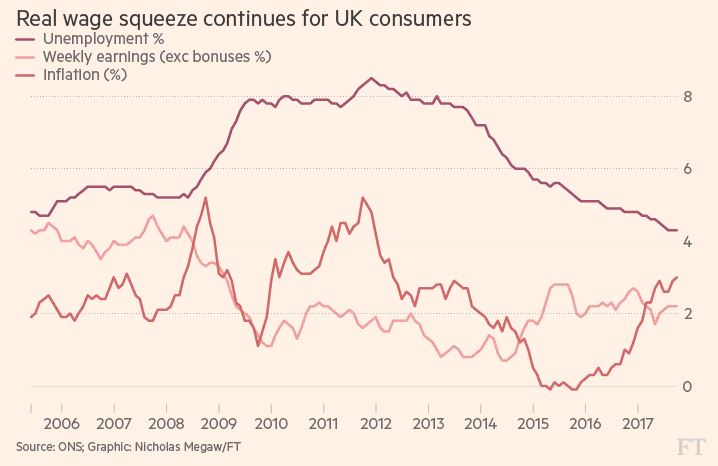

The other notable development from this morning was the latest wage data out of the UK which continues to reflect the on-going squeeze being felt by UK consumers. This of course comes one day after UK CPI printed at 3.0% Y/Y and in the backdrop of mounting political pressure on the governments ability to deliver a smooth exit from the European union. The rest of the week could now be telling for Cable with UK Retail Sales due tomorrow which if a disappointment would cement a growing bias towards negative themes gathering momentum in the UK economy.

The Day Ahead

This afternoon will be interesting as attention moves to US CPI and Retail Sales reports. The former is undoubtedly the main focus of US policy makers. Analysts at Deutsche Bank note that headline CPI in the US has missed expectations 6 of the last 7 releases and the only time it didn’t was an inline reading. Beyond this they highlight an interesting point in that over the last 20 years US inflation has lagged GDP by approximately five to six quarters. As such, if history holds true then in time the stronger growth seen post the 2H of 2016 should start to impact inflation soon. The question now is if this is going to occur as soon as today or as we head into 2018 with the bias being that Q1 will be when prices should start to move back to target in lockstep with further economic improvements.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.