Federal Reserve Preview: How Powell may drain the Dollar of any dot-related gains

- The Federal Reserve is widely expected to raise rates by 50 bps, slowing down its tightening pace.

- Fresh forecasts are set to show a higher peak interest rate for 2023, boosting the Dollar.

- A softer tone by Fed Chair Powell on the economy may grind the Greenback.

Less now, more later – that has been the talk by the Federal Reserve, and now it will walk the walk by raising rates at a slower pace of 50 bps, yet signaling a higher peak rate. With so much information already in the pipeline, will investors focus instead on the football? Not at all, there are more moving parts in this decision than the previous one, which are likely to trigger action.

The bank's final decision of 2022 has three pillars, each of growing complexity: the rate change, fresh forecasts, and Chairman of the Federal Reserve Jerome Powell's press conference. Here goes:

Rate decision – slow down to a 50 bps hike

"The time for moderating the pace of rate increases may come as soon as the December meeting" – Fed Chair Powell's words on November 30 were a clear signal that the bank will raise borrowing costs by 50 bps after four consecutive increases of 75 bps. Barring a massive surprise in Tuesday's inflation report, the world's most powerful central bank will deliver on that promise, meeting market expectations.

Flattening the rate curve:

Source: FXStreet

Why slow the pace of hikes? Inflation has seemed to peak. October's Consumer Price Index (CPI) report showed headline inflation dropping to 7.7% YoY, while Core CPI also slipped from a peak of 6.6% to 6.3%. The Fed watches underlying inflation – price rises excluding energy and food – as it has limited impact on factors set in global markets.

On a monthly basis, Core CPI rose by only 0.3% in October, half the rate of the previous two months, and Core PCE – another inflation gauge, preferred by the Fed – advanced by merely 0.2% in October. The latter figure reflects an annualized rise of roughly 2.5%, in line with the bank's 2% target.

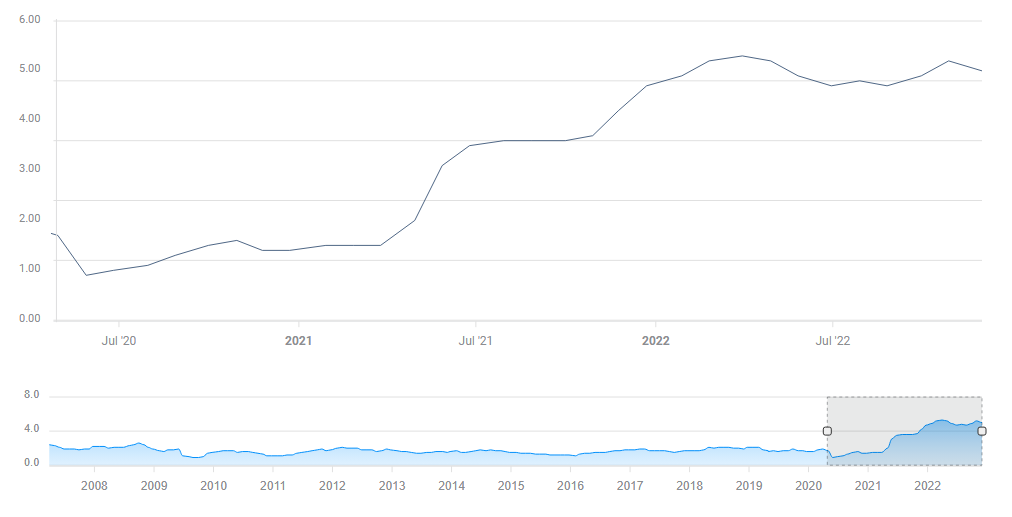

Core PCE set sets lower highs:

Source: FXStreet

Already in early November, before the promising CPI report was known, the Fed stated that monetary policy works with a lag. It wants to assess its cumulative increases of nearly 4% first rather than act aggressively again.

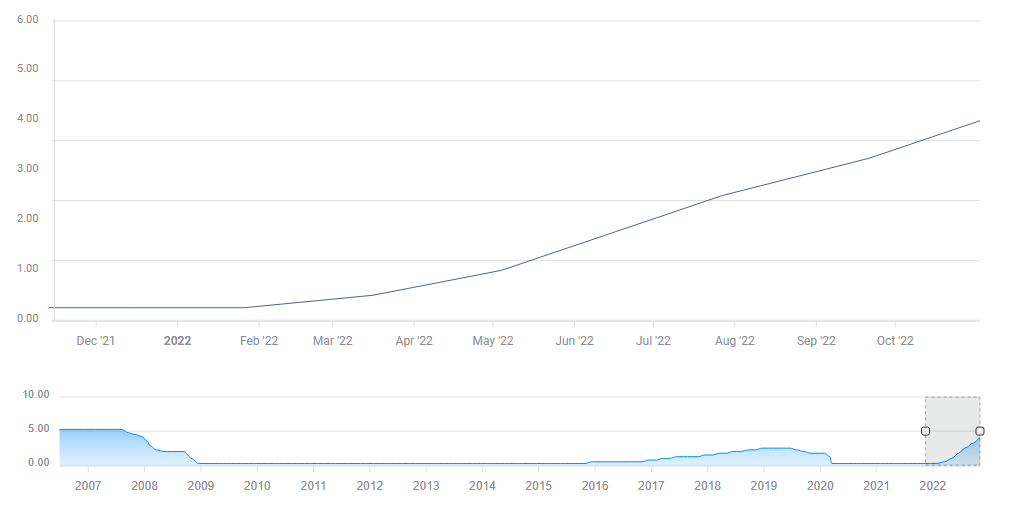

Moreover, there are some signs of a slowdown in the US economy, such as a cooling in the housing sector and a moderation in job growth. The bank's second mandate is full employment, and while America is still hiring, job openings are off their highs.

The peak in hiring has certainly been reached:

Source: FXStreet

I want to stress that there are also plenty of positive signs about the economy and inflation, such as robust Black Friday sales and upbeat wage growth. Nevertheless, lags in the effect of higher rates on economic dynamics call for caution.

The rate hike of 50 bps is unlikely to have any effect on markets as it is mostly priced in. What mattered last time was the statement, but this time, forecasts take center stage.

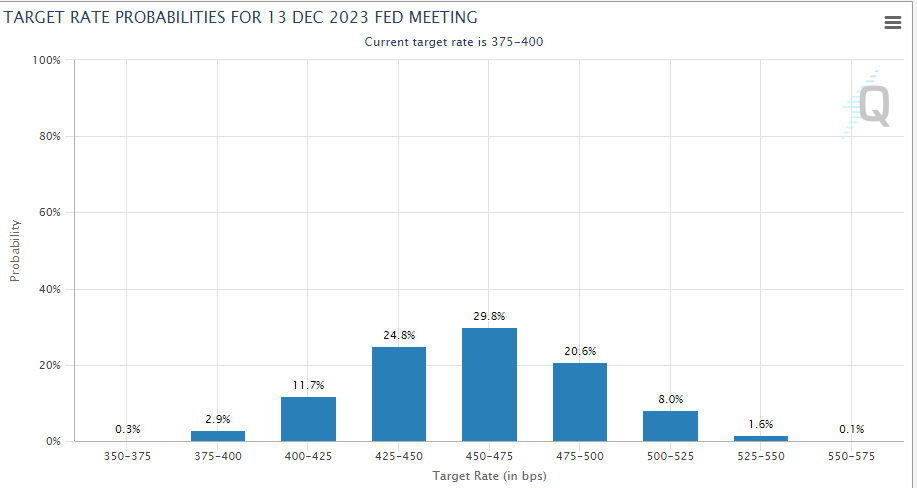

Dots drifting to 5% or above?

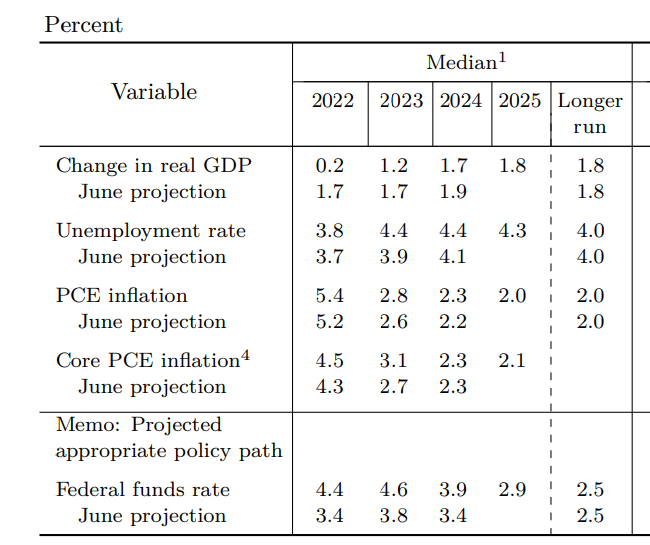

Powell promised rates would rise to a higher level than previously thought, but by how much? New projections by all FOMC members showed rates ending 2023 at 4.6%, and the number will surely rise. The round 5% level is critical.

The Fed's previous dot plot pointed to rates hitting 4.6% in 2023, 3.9% in 2024:

Source: Federal Reserve

While markets foresee rates rising above 5% by May 2023, a drop below that level is priced for the end of the year. That is inconsistent with the Fed's message – that rates will stay higher for longer, signaling no rate cuts next year.

The dot plot is where hawkish Fed members can make their mark, pushing the median rate above 5% and triggering a rise in the US Dollar.

Americans still have elevated savings from the pandemic era – via stimulus and inability to spend – while there are still two job vacancies for every worker. That means it would take more time to cool the economy and price pressures. That is the glass half-full of forecasts.

Investors see the glass half empty, and are becoming growingly wary of a recession triggered by the lagging effect of higher rates, China's twin COVID and property crises, and Russia's ongoing invasion of Ukraine.

Bond markets forecasting sub-5% rates for December 2023:

Source: CME Group

Apart from the peak rate for 2023, investors will also be looking at the final rate for 2024, which implies how much members see rates falling when they do finally start to lower them. Another disappointment could follow. Projections for growth, unemployment and inflation will probably be taken with a large grain of salt.

All in all, a substantial upgrade of 2023 rate forecasts are not fully priced by markets and could trigger a surge in the Dollar and a drop in stocks. The statement and the forecasts are out at 19:00 GMT, and the best and most complex is left for last.

Powell's presentation

At 19:30, the Fed Chair takes to the stage to provide more information about the bank's deliberations and to answer questions. In most previous events, the reaction to Powell was the opposite of the initial one. Back in November, comments about monetary policy working with lag implied slower rate hikes and boosted markets. Then came Powell and stated that the peak rate will be higher, sending stocks sinking.

Here is EUR/USD's performance around the Fed decision on November 2:

I expect a similar whipsaw but in the other direction: markets to suffer first, then cheer. Why? Powell has pivoted. In late August, he spoke for merely eight minutes, vowing to crush inflation without mentioning a soft landing. That was then.

Three months later, he replaced the hawkish message with a different tune – promising not to wreck the economy in the fight against inflation and not to "overtighten." In his press conference, Powell may opt for a more conciliatory tone, putting a greater emphasis on the ability to cut rates if the economy weakens too fast.

It may be subtler – the Fed Chair could focus on the signs of softness in the labor market, opening the door to reacting to job losses. There are some signs of weakness even within the recent upbeat Nonfarm Payrolls’ (NFP) report.

The NFP is based on two surveys, the Establishment survey, which provides the headline increase, and the Household survey, which is used for calculating the unemployment rate and other figures. According to the Household survey, America's labor force has squeezed in the past two months. While this may be a temporary statistical discrepancy, some see it as a warning sign.

If Powell mentions the Household survey as a reason to worry, he could spark hopes for rate cuts next year, boosting stocks and sending the Dollar up. Yet even if he only settles for a more cautious tone rather than one set on a quixotic battle against inflation, markets would see it as a rallying cry. In the season of giving, markets are looking for reasons to rally.

Final thoughts

Beyond the expected 50 bps hike, the Fed's projections may suggest higher rates for longer, weighing on markets and boosting the Greenback. That would change when Powell speaks up, repeating his more dovish tone, as recently heard at the Brookings Institute. That would reverse the picture. This potential whipsaw creates an opportunity, a mirror image of last month's rate decision price action.

I have referred to football at the beginning, and it is a factor that cannot be disregarded. The World Cup semi-final between France and Morocco will take place simultaneously, causing some European traders to opt for the match instead of the Fed. That may further lower liquidity and add to the action.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.