Federal Reserve Chairman Powell House Testimony Preview: No drama Jerome

- Inflation is not key to Fed policy, it's about jobs and GDP

- Markets have fully priced a 25 basis point reduction this month

- Powell unlikely to offer many clues to July policy, stressing incoming data

Federal Reserve Chairman Jerome Powell will have a perfect opportunity to explain and predict interest rate policy when he appears before Congress this week. He will certainly do the former and just as certainly skip the latter.

Mr. Powell’s testimony at the House Financial Services committee and the Senate Banking Committee on Thursday in the Fed’s twice yearly Monetary Policy Report comes when expectations for a 25 basis point cut at the July 31st FOMC meeting approach near unanimity even though the excellent June payrolls report removed some of the economic urgency.

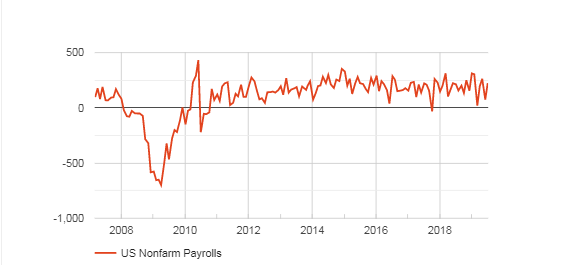

The US added 224,000 workers last month, far more than the 160,000 forecast and the unemployment rate of 3.7% was a five decade low.

The unexpected strength of the labor market helped to alleviate concerns that two NFP months below 100,000, February and May, combined with ADP’s 27,000 May and 102,000 June payrolls indicated that job creation was following estimated GDP lower.

FXStreet

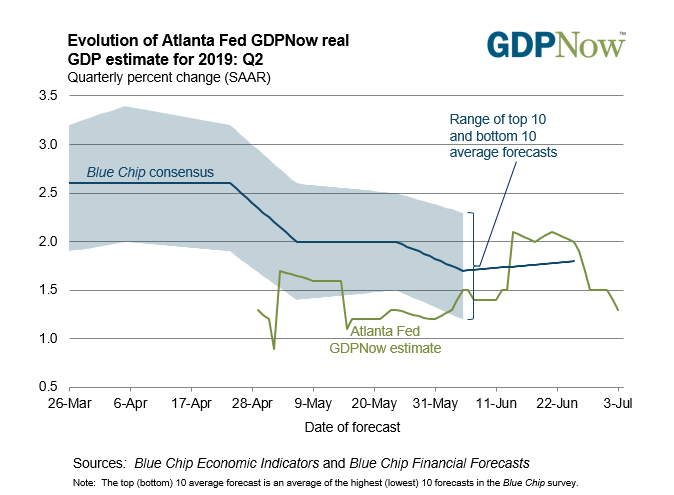

The economy expanded at a 3.1% annual rate in the first quarter but the Atlanta Fed GDPNow current forecast for the second quarter is just 1.3% and has been below 2% for most of the past two months.

Atlanta Federal Reserve

Treasury yields jumped after the Friday jobs report with the 10-year moving back above 2% and the dollar rallied against all majors.

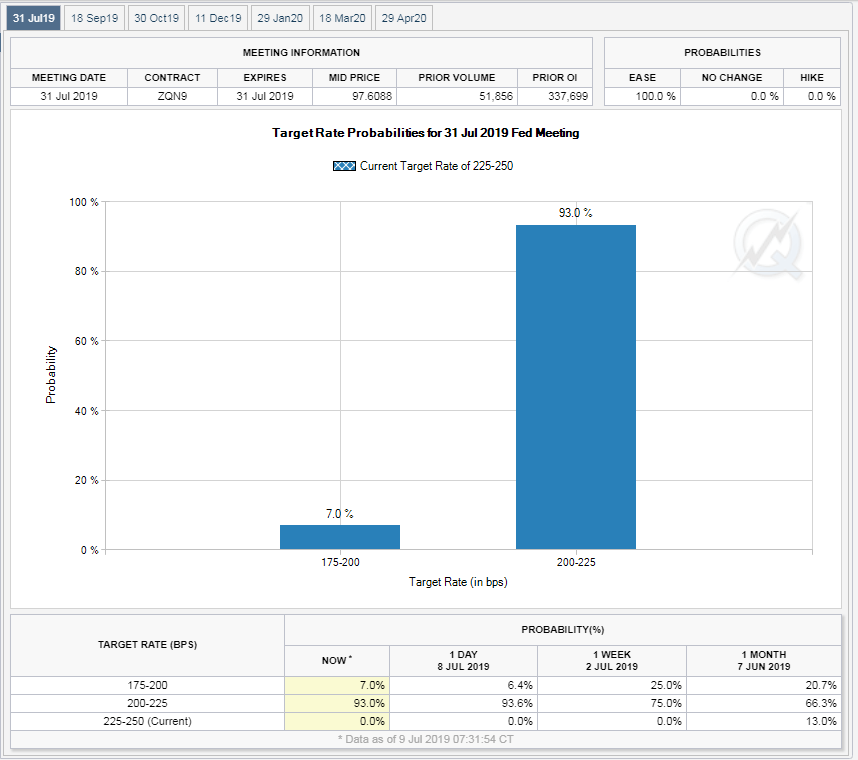

Powell could reinforce market expectations for a July and subsequent interest rate cuts, dial back the possibility of any reductions at all or reaffirm this month’s decrease and douse speculation for future cuts. But with the fed funds futures listing the chance of a 0.25% cut at 93% and the odds of a 0.50% reduction at 7% any substantive rate comment by the Fed chairman could offer unnecessary complications.

CME Group

The chairman’s economic analysis will present sufficient target for speculation as comments underlining US economic strength and prosperity will tend to support the case for few or no rate cuts and those outlining American problems or global tensions will back the argument for once and future rate reductions.

There will be several other indicators this week on Fed policy. On Wednesday afternoon the edited minutes of the June 18-19th FOMC meeting will be released. Mr. Powell had suggested in his June news conference that the central bank could cut rates if necessary.

On Thursday the consumer price index for June will be released with the annual core index expected to be stable at 2% and headline falling to 1.5% from 1.8%. The producer price index will be out on Friday with the core rate forecast to be unchanged at 2.3% on the year.

Stable prices are one of the Fed’s twin Congressional mandates, the other is full employment but inflation is unlikely to make either case for a Fed rate move.

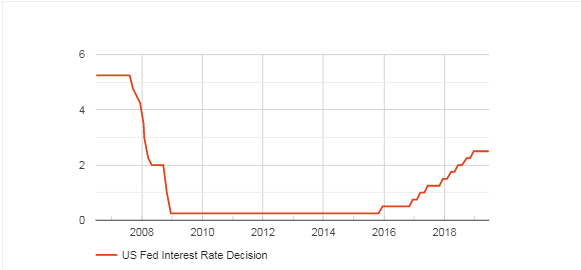

For most of the last decade inflation has resisted Fed policies to bring it to the bank’s 2% target. During the three year effort beginning in December 2015 to raise the fed funds stubbornly low inflation did not dissuade the governors from normalizing interest rates.

Powell’s major concern in his two days of testimony will be to not upset market expectations. The equity, credit and currency markets would react violently to a perceived change in Fed thinking on interest rates.

Having set the markets on the path the Fed is not going to toss over the interest rate cart now.

FXStreet

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.