Fed Tapering: Could RBA be due for intervention?

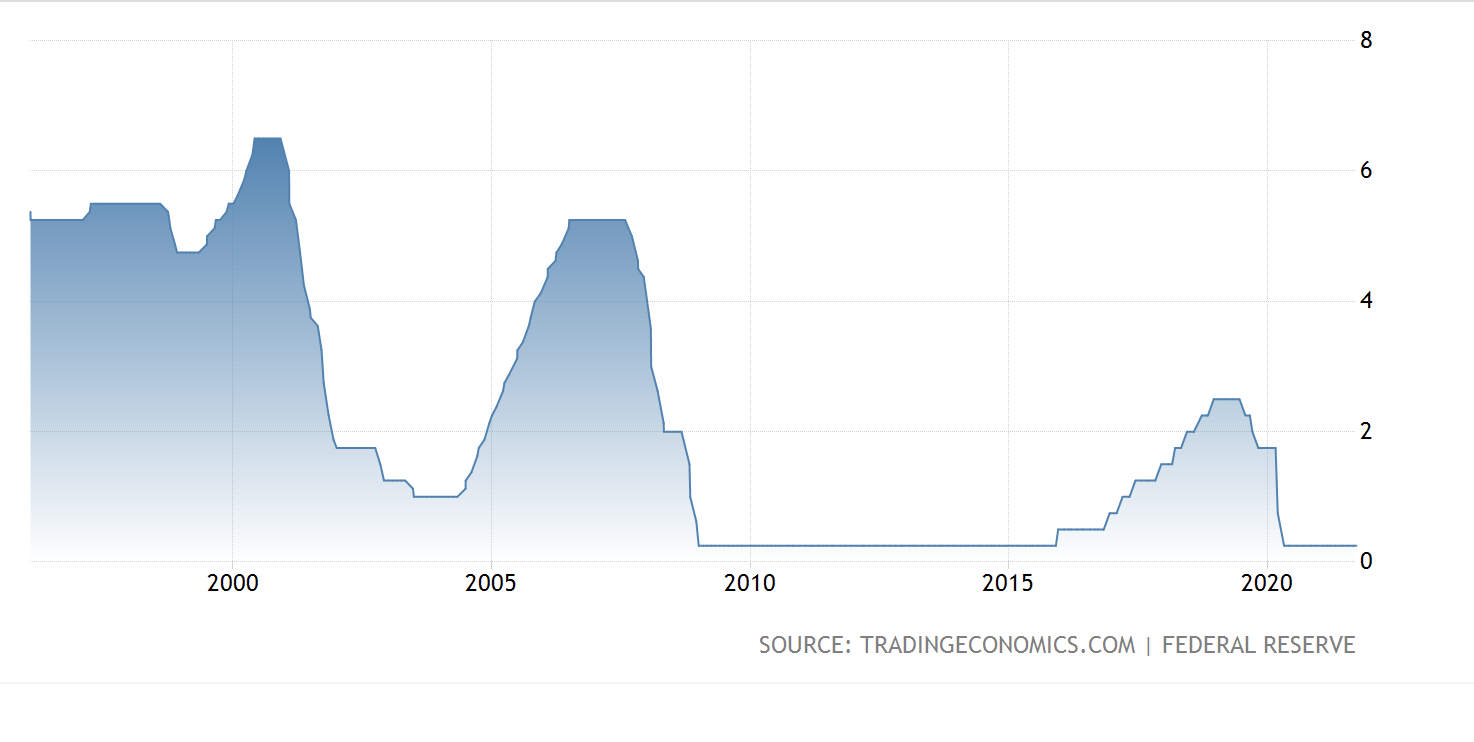

US Interest Rates, how long at so low?

Fed Chair Powell, hikes not yet.

While there is now a total green light on the tapering of bond purchases, US Federal Reserve Chairmen Powell also said it is too early for interest rate hikes.

The really interesting thing though, is to see how eagerly such an eventuality is now being discussed. Interest rate hikes are coming.

We have been right in forecasting tapering for this year, and we will be right in our forecast that the Federal Reserve will start raising rates in the first half of 2022. Both occurring, far earlier than the Fed itself had previously been forecasting.

It is great to see the Fed maintaining flexibility. Even if it is already behind the curve and has not yet fully grasp the true nature of the continuing inflationary pressures.

Unfortunately, as I highlighted rather aggressively last week, our own central bank remains at the bottom of the heap in this regard. To such a poor performance degree, that one wonders if the RBA Governor/Board may need to be replaced by political intervention in the coming year? This would be an extreme event indeed, but the performance in service of the people is what matters. Generating easy money property and asset bubbles, doing so persistently and stubbornly, even massively interfering in normal markets on Friday purchasing a billion dollars of 3 year bonds, just to prove itself right about keeping rates abnormally low, is not part of the Reserve Bank charter. This is extreme and aberrant behaviour, that is overdue for external review and intervention. Stay tuned.

US stocks fell back in on themselves a little on Friday, and the New York closes were not particularly strong. There could be some vulnerability developing in global equities this week. Post the always Monday morning rally in Australia.

Note, both China and the UK are currently seeing worrying delta surges yet again. Serious lockdowns in the UK are highly unlikely, but their renewed discussion does go to show what has been clear all along, vaccinations wear off, and with the virus now widespread it is always ready to make a fresh surge. Some on-going supply chain disruption and subdued economic activity at both the national and global level remain likely.

Vaccinations do not equal strong economic performance. This is the Achilles-heel of equity market sentiment, that could quickly see markets unwind recent strong gains.

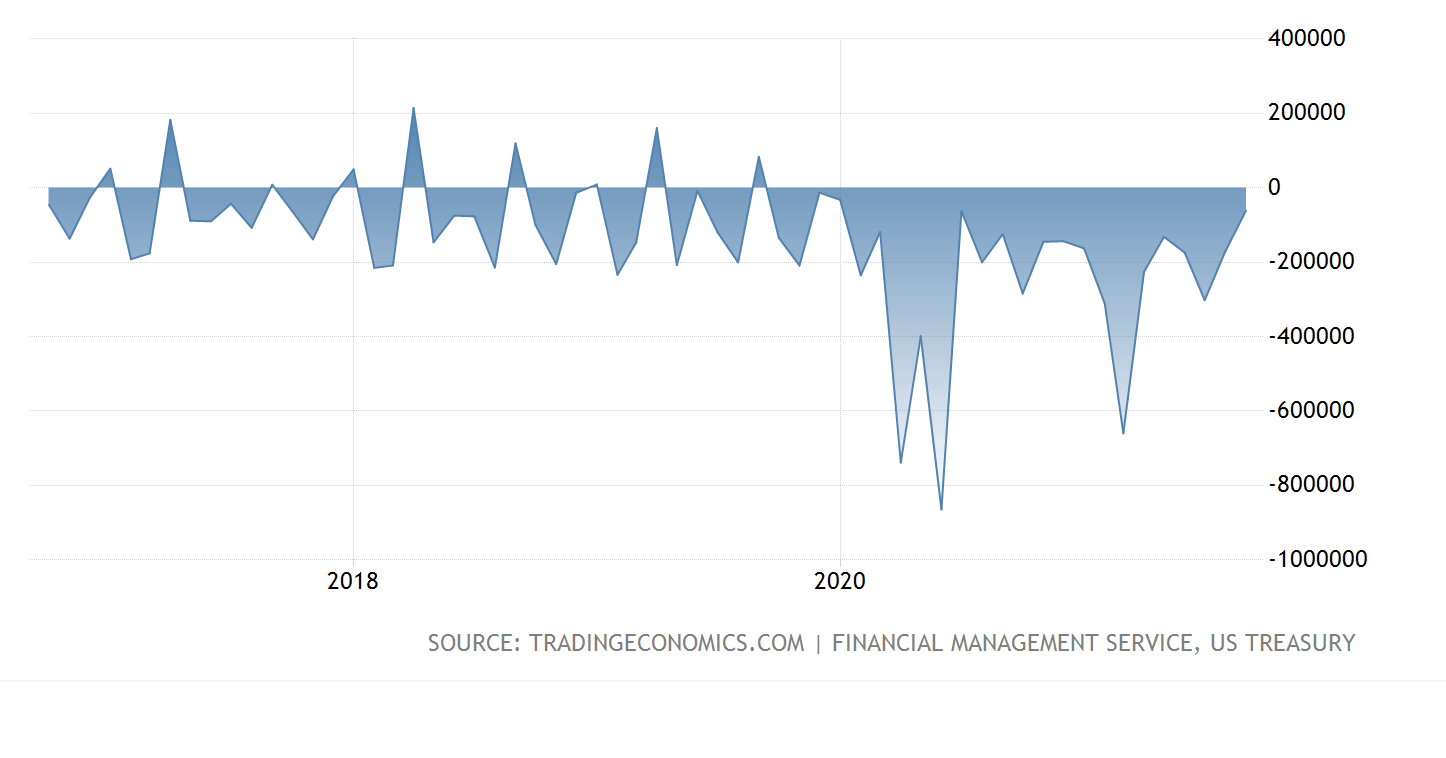

US Budget Deficit.

2021 has already achieved the second highest deficit in history, following the 2020 record. Government spending and stimulus has remained high, and one wonders what the real GDP level might be without this mask? For that is the real sustainable level of economic activity the US economy possesses.

US GDP would in fact be negative in the current period, without this massive fiscal deficit. Even with the spending, the next quarterly GDP release could well be very close to zero.

My forecast, is just 0.8% for US GDP in Q3. Consensus is 2.8%.

Either way, that is a big drop from 6.7% previously. Which at the time, the consensus expected to be maintained?

Subliminal Stocks.

Author

Clifford Bennett

Independent Analyst

With over 35 years of economic and market trading experience, Clifford Bennett (aka Big Call Bennett) is an internationally renowned predictor of the global financial markets, earning titles such as the “World’s most a