Fed Survey Points to Slowing Loan Demand

The Fed's Senior Loan Officer and Opinion Survey showed cooling loan demand for businesses and consumers in Q1. Citing uncertainty and lower risk tolerance, banks continued to tighten standards for CRE loans.

Business Loan Demand Tails Off

The Federal Reserve's April 2017 Senior Loan Officer Opinion Survey (SLOOS), which roughly corresponds to Q1 2017, points to a general slowdown in loan demand for businesses and consumers. Reports of tightening lending standards varied across loan categories, however.

As shown in the top chart, large and small businesses demand for loans has been moderating since the start of 2016. Domestic and foreign banks reported weaker loan demand on net over the first quarter. Notably, the slowdown in commercial & industrial (C&I) loan growth does not appear to be due to stricter lending standards, as banks reported no significant net tightening. The survey showed a modest net easing for C&I loans by domestic banks, but a slight tightening by foreign banks.

The SLOOS C&I lending data are contrary to the details within the GDP release. While the survey data point to a slowdown in business loan demand in Q1, the GDP report indicated a strong pickup in business fixed investment with outlays rising at a solid 9.4 percent annualized rate. The strength in business investment may reflect firms' use of other sources of funding, such as bond issuance and stronger profits.

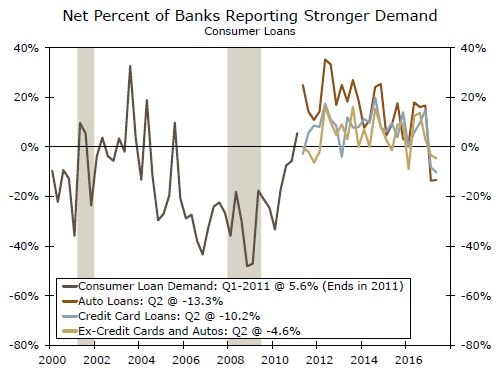

Consumer Loan Demand Cools

The Fed survey also showed a cooling in consumer loan demand, a finding consistent with the weaker pace of consumer spending in Q1. Lenders reported reduced demand for most consumer loan categories over the quarter, with particular softness in demand for credit card and auto loans (middle chart). A moderate share of banks reportedly tightened auto loan standards in Q1, marking the fourth consecutive quarter of net tightening. Banks stated widening spreads of loan rates over their cost of funds and raised the minimum credit score threshold over the quarter. For credit card loans, a modest share of banks reported easing lending standards, while terms on other consumer loans remained unchanged on balance. We do not take the softer consumer lending report as the start of a new trend and look for consumption to re-emerge in Q2.

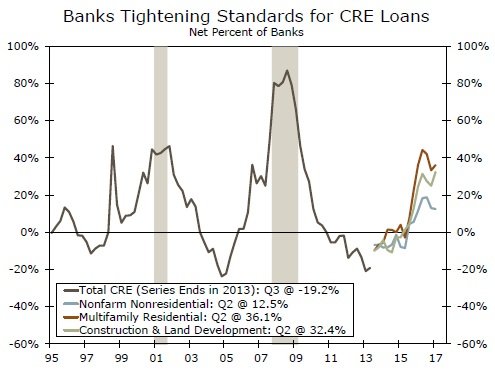

CRE Lending: Continued Tightening

The April SLOOS showed that lenders are continuing to monitor pockets of risk in the commercial real estate (CRE) sector, as a significant net share of banks reported further tightening in most CRE loan policies (bottom chart). In fact, a major share of banks cited a more uncertain outlook for CRE property prices, vacancy rates and other fundamentals, and reduced risk tolerance as reasons for tightening credit standards. In a recent speech, Boston Fed President Eric Rosengren noted that while a handful of favorable factors have helped support CRE valuations, "positive trends can sometimes evolve into prices that increase more than fundamentals justify."1 Banks' continued tightening of CRE credit should help ease financial regulators concerns of elevated pricing.

Author

Wells Fargo Research Team

Wells Fargo