Fed study shows the ECB made a huge mistake with negative rates

ECB punishes banks with negative interest rates

please consider Commercial Banks under Persistent Negative Rates by the Federal Reserve Bank of San Francisco.

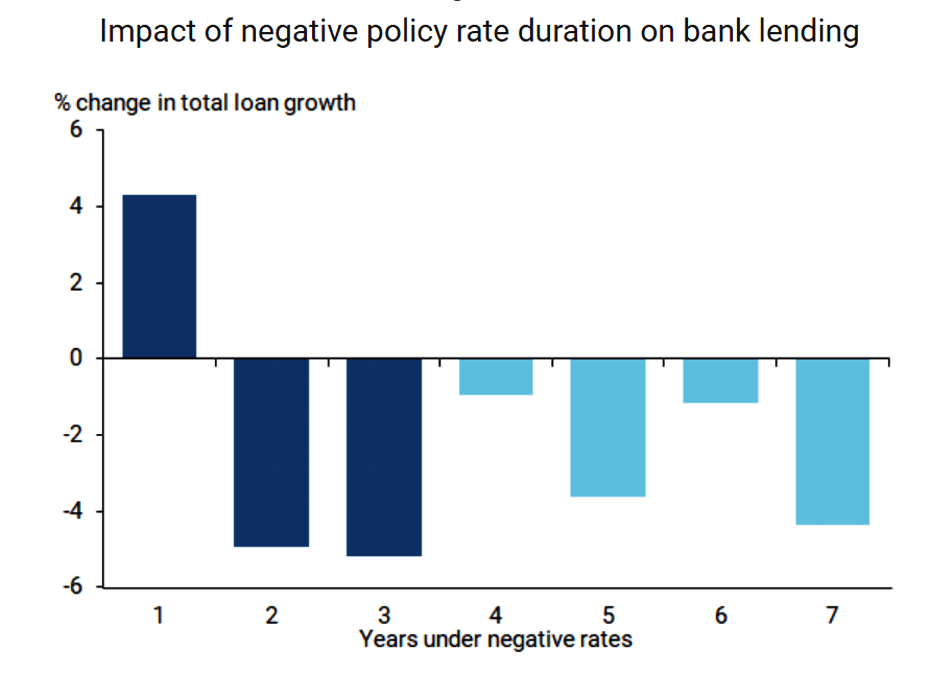

Do extended periods of negative policy interest rates continue to encourage commercial bank lending? A large panel of European and Japanese banks provides evidence on the impact of negative rates over different lengths of time.

Analysis suggests that both bank profitability and bank lending activity erode more the longer such negative policy rates continue, primarily due to banks’ reluctance to pass negative rates along to retail depositors. This appears to negate one of the main arguments for moving policy rates below the zero bound.

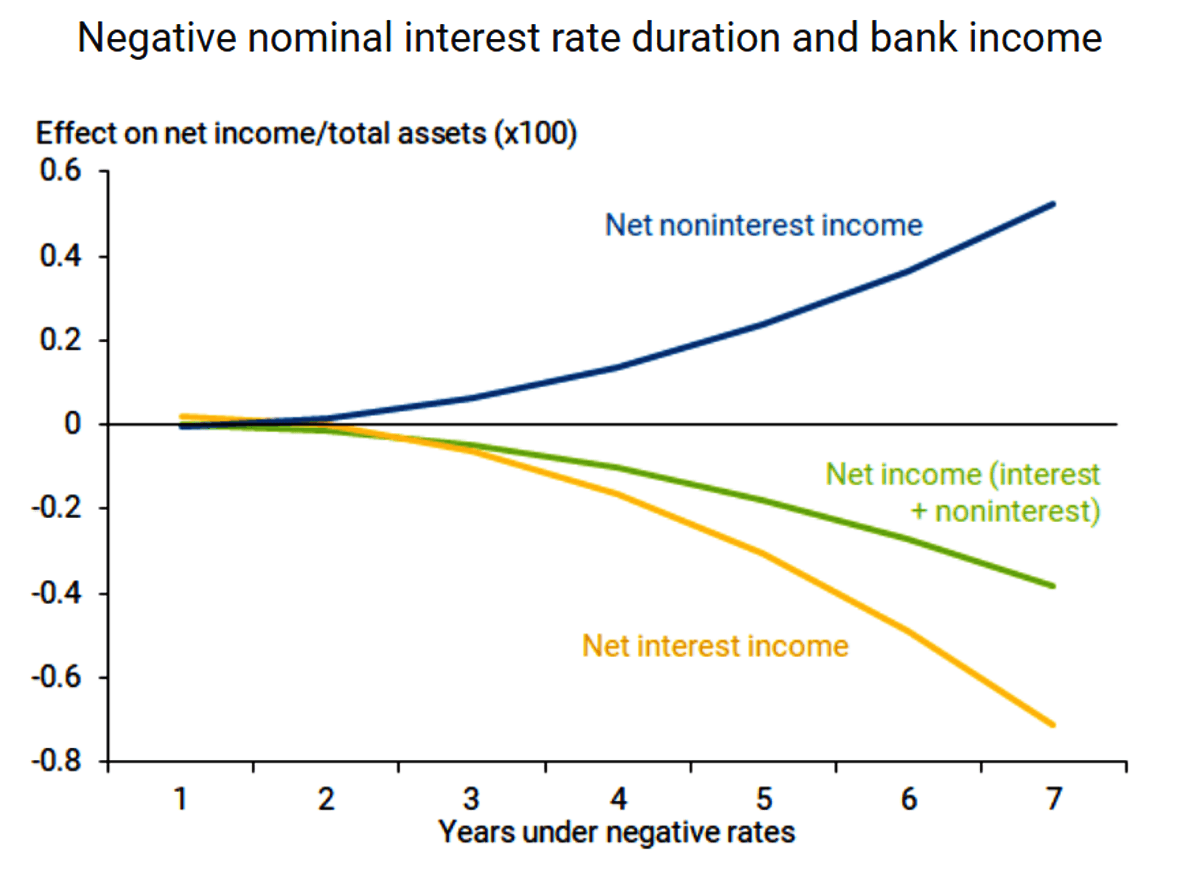

Our results suggest that banks can only mitigate losses on interest income through charging fees on deposits and enjoying capital gains on securities holdings for short periods of negative interest rates. As durations of negative policy rates lengthen, the gains from these adjustments become increasingly inadequate to offset the growing losses on interest income due to banks’ limited abilities to pass along negative rates to depositors. The result is that, as negative rates persist, they drag on bank profitability even more.

The data clearly show that losses on interest income accelerate over time and begin to outweigh the gains from noninterest income. As a result, the impact on overall profitability falls below zero. Our regression analysis for the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates.

No surprise

I talked about this six years ago when the ECB first went to negative rates.

Statements I made then still apply,

- The Fed paid interest on excess reserves slowly recapitalizing banks over time.

- The ECB charged interest on excess reserves draining already stressed banks of capital.

I question the study's statement "the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates."

Indeed, their own chart shows negative impacts after a year.

Lose-lose setup

In short bank lending suffers after one year and profitability suffers at increasing rates over time.

It is for this reason I have often stated the Fed would not be stupid enough to opt for negative rates.

The effective lower bound is at least somewhat above zero.

Effective lower bound

Please see my September 25, 2019 post In Search of the Effective Lower Bound

The Fed is no longer talking about zero-bound but effective lower bound. What's the difference? Where is it?

Effective Lower Bound is the point beyond which further monetary policy in the same direction is counterproductive.

I propose the Bank of Japan and the ECB are already below ELB. I further propose the ELB can never be negative but it can be well above zero.

Negative interest rate policy can never work as it violates basic economic principles on time preference and the time value of money.

Moreover, a dive below the ELB supports the position I presented on September 23, 2019: Negative Interest Rates Are Social Political Poison

Deeper Down the Rabbit Hole

Yesterday, I noted Draghi Open to MMT and a People's QE

Every attempt to fix the perceived problem of "too low inflation" goes deeper and deeper down the rabbit hole.

It's economic madness, yet, here we are.

It took a multi-year study for the San Francisco Fed to come to the right conclusion.

That's a step in the right direction. Many of these studies come to the wrong conclusion.

The solution is to let the free market set interest rates rather than a tail-chasing consortium of economic wizards who have never spotted a bubble or a recession in real time.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc