Fed split widens as market loses its compass

The week began with markets still trying to digest the Federal Reserve’s September cut and ended with policymakers openly contradicting one another about what comes next. In less than forty-eight hours, at least six Fed officials spoke in public, delivering messages that ranged from “further easing is appropriate” to “we may have gone too far.” The result has been a surge in uncertainty: traders are no longer debating if rates will fall again, but who inside the Fed still believes they should.

A divided central bank

Governor Michelle Bowman argued that inflation progress remains “uneven” and that another rate cut could “risk reigniting price pressures.” San Francisco’s Mary Daly countered that policy should remain “adaptive and flexible,” hinting that growth indicators are slowing faster than expected. New York’s John Williams added a careful middle ground, “data-dependent” language that in practice means little when official data flows are frozen by the government shutdown.

These conflicting tones reveal something deeper: a Fed that is internally split between credibility and caution. Some members fear losing inflation-fighting credentials; others fear tightening into a slowdown. In normal times, the Chair’s guidance would smooth the message, but Powell’s latest remarks did little more than repeat the September statement. The market, left without a compass, has turned every speech into a micro-event.

Markets price what the Fed won’t say

Futures on Fed funds now discount three additional cuts before year-end — roughly 75 basis points of easing that no official has confirmed. Two-year Treasury yields dropped below 3.90%, while ten-year yields held near 4.05%, flattening the curve again. Equity traders initially celebrated the softer yields, but enthusiasm quickly faded: without clarity on policy trajectory, risk appetite can’t gain traction.

The dollar mirrored that indecision. After bouncing early in the week, the DXY slipped back toward 101, pressured by expectations of lower real rates but supported by periodic safe-haven flows. In short, the greenback is being pulled in opposite directions, exactly like the institution that issues it.

Gold, meanwhile, paused near record territory after last week’s breakout. The metal’s consolidation around $4,000 shows how investors have already priced the dovish narrative; only a decisive shift in Fed tone could ignite a new leg higher. Silver trades sideways, reflecting the same paralysis across macro assets.

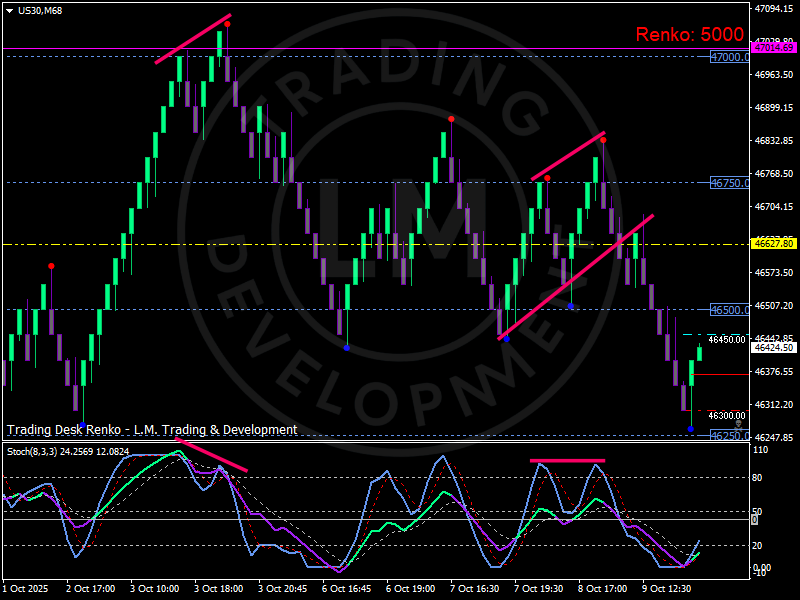

A technical mirror of hesitation

The Dow Jones (US30) encapsulates this indecision perfectly. After an early-October rebound, momentum failed to extend; bearish divergences multiplied on intraday frames, and the index slipped back into its previous range. The Renko chart highlights two failed bullish attempts and lower highs that mirror the Fed’s mixed guidance.

Dow Jones (US30) Renko chart shows repeated bearish divergences and a failed breakout pattern, illustrating how traders hesitate amid the Fed’s mixed signals and a market in search of direction.

From a technical standpoint, support sits near 46,300–46,350, while resistance remains capped around 46,750–47,000. Until one of those zones breaks convincingly, volatility will stay compressed — a visual metaphor for a central bank talking in circles while markets wait for leadership.

Bond markets: The pause after the sprint

The bond market, normally the Fed’s most faithful barometer, has fallen into a similar pattern of hesitation. After an intense rally through late September that sent two-year yields plunging, the move has now stalled. Traders are reluctant to add duration until they know whether the next policy step will be another cut or a strategic pause.

This holding pattern is visible in the Treasury futures curve, where open interest has flattened and volume has dropped nearly 15% from last week’s peak. Liquidity is thinner, volatility is compressed, and the price action looks more like indecision than conviction. In short, bonds have entered the same range-bound limbo as equities — a market waiting for confirmation that never comes.

A blackout that amplifies confusion

Under normal circumstances, data would act as the referee in the debate between hawks and doves. But the US government shutdown has darkened that scoreboard. Without BLS or BEA updates, the Fed is effectively flying blind; private data sets like ADP and ISM surveys have become stand-ins for official releases. That shift has amplified uncertainty, because private indicators rarely move in sync with official numbers.

Investors now face an environment where macro noise exceeds macro signal. Each speech by a Fed official gets overinterpreted, and each market move gets exaggerated in turn. This feedback loop — less data → more speculation → higher volatility — is eroding the clarity that normally anchors expectations.

The irony is striking: the more transparent the Fed tries to be, the more fragmented its message becomes when every voice speaks separately.

The Dollar and Gold: Opposite symptoms of the same disease

The dollar’s struggle for direction has left it oscillating between 101 and 102 on the DXY. Short-covering rallies are immediately met by sellers, while dips invite safe-haven buying. That tug-of-war reflects the same indecision visible in Treasuries and equities.

Gold, by contrast, has stabilized above $3,980, holding onto the gains from its record run. The absence of new upside momentum is not weakness; it’s equilibrium. In a world where neither inflation data nor Fed guidance provides certainty, gold has become the quiet constant — an asset that traders don’t need to trust a policy statement to understand.

Risk sentiment: Suspended animation

Equity traders describe the current market as “fat-tailed calm”; volatility is low, but every move feels potentially explosive. Indices like the US30 illustrate that paradox perfectly: multiple bearish divergences, but no full breakdown; soft bids, but no real conviction. Investors are unwilling to commit until the Fed itself shows internal cohesion.

This explains why global risk sentiment remains in suspended animation. The S&P and Nasdaq mirror the same behavior: sideways patterns that compress until something (a speech, a data point, or political headline) breaks the tension.

The wider message: The Fed is no longer leading

At its core, the story of this market isn’t about rates or inflation; it’s about credibility. For the first time in years, the Federal Reserve is not steering the market — it’s chasing it. Each dovish whisper moves futures more than official guidance, and each hawkish warning is ignored until traders see proof in the data.

This inversion of leadership is dangerous. When policy communication loses coherence, markets start creating their own narrative, and once that happens, volatility ceases to be noise; it becomes governance.

If the Fed cannot regain message discipline, the gap between policy and pricing will widen further, forcing the central bank to react rather than guide. For now, both sides — policymakers and traders — are stuck in the same narrow band as the US30 chart itself: oscillating, hesitant, and waiting for clarity that may not arrive until data returns.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)