Fed Preview - Here's 3 Changes to Expect for July

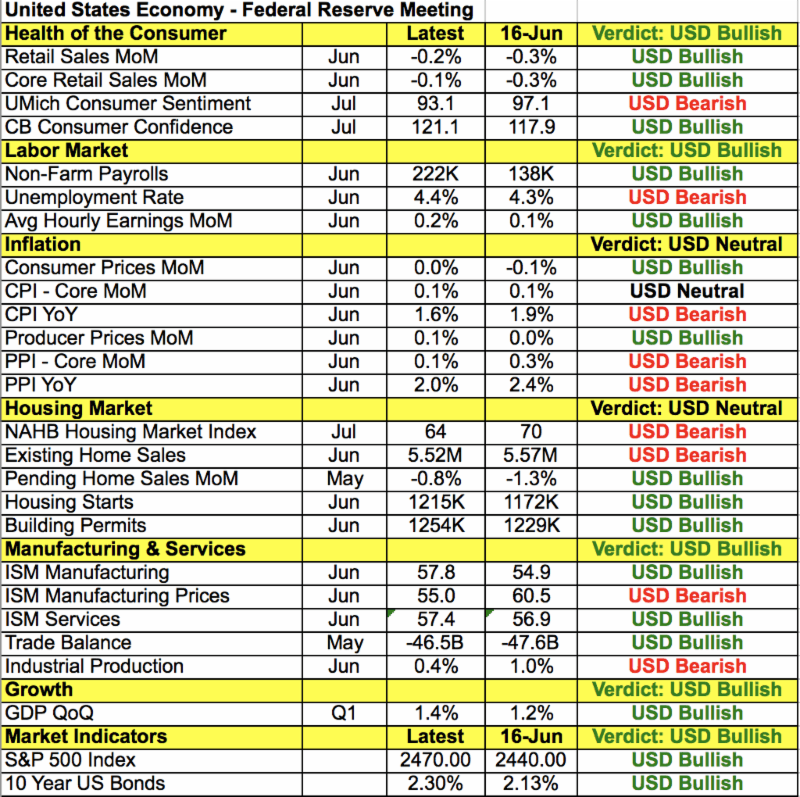

Investors continued to take off short USD/JPY positions ahead of Wednesday's Federal Reserve announcement and given the positive momentum in the greenback, it may not take much for the gains to spillover to currencies that have resisted the dollar's rise like euro, sterling and the Australian dollar. With U.S. stocks climbing to fresh record highs, there's very little reason for the Fed to change its tune. Taking a look at the table below, even though there have countless negative surprises in U.S. data, the U.S. economy has still seen more improvement than deterioration since the last FOMC meeting. Yet we can't ignore the fact that inflation has fallen on a year over year basis as spending and wage growth remains weak. So even if the Fed remains committed to normalizing monetary policy, investors will continue to doubt their optimism until there's a consistent stream of positive data. Today's rally in the greenback is supported by a sharp rise in yields, the Senate's vote to debate Obamacare, stronger than expected consumer confidence and an uptick in manufacturing activity in the Richmond region.

Looking ahead to Wednesday's Federal Reserve announcement, we anticipate 3 changes to the July FOMC statement.

1. No Rate Hike - First the Federal Reserve won't be raising interest rates like they did in June. They've been under the habit of tightening only at quarterly meetings and that seems to be the game plan going forward.

2. Signal Reduction in Asset Purchases "Relatively Soon" - The Fed is in no position to raise interest rates in September but NY Fed President Dudley previously suggested they could shrink the balance sheet in between rate cuts. Reducing asset purchases could begin as early as September, which would make this meeting the perfect opportunity to pre-announce the change.

3. Acknowledge Downtick in Inflation - The biggest problem for the Fed is the decline in annualized consumer and producer price growth. They may be forced to recognize the slowdown in price growth and the impact it has on reaching their 2% inflation target.

The positives will probably outweigh the negatives, causing the dollar to extend higher post FOMC but the gains won't last as investors still question the firmness of U.S. data. The next big report will be non-farm payrolls so between FOMC and NFP, we could see another round of U.S. dollar weakness especially as traders step in to fade Congress after the rate decision. Resistance in USD/JPY is at 112.65, the 20-day SMA while support sits at 110.60.

Stronger than expected German business confidence helped prevent further losses in euro although the currency still ended the day off its highs against the greenback. Despite the prospect of a rate hike and the consequence of a stronger euro, businesses remain confident that the recovery will strengthen. The resilience of the euro and the central bank's positive outlook makes the euro a particularly attractive buy on dip post FOMC. Between now and the rate decision, anyone interested in buying euros should look at EUR/JPY. Sterling raced to a high of 1.3084 versus the U.S. dollar before tumbling on the back of U.S. dollar strength. U.K. GDP numbers are scheduled for release tomorrow and while growth is subdued, we anticipate a small uptick due to the rise in retail sales.

One of the best performing currencies today was the Australian dollar. Aside from the rise in commodity prices, there was very little catalyst for the move. The most important event risk for AUD this week is consumer prices and the second quarter data is due this evening. Like in many major economies, inflation is low and even if the quarterly rate increases, the year over year rate could decline or vice versa. RBA Governor Lowe will also be speaking and chances are with AUD/USD up 10% year to date, he'll take this opportunity to complain about the strong currency. So if CPI falls short of expectations and Lowe talks down the currency, it would be the perfect catalyst for a top in AUD. The New Zealand dollar on the other hand spent most of the day in negative territory versus the U.S. dollar. For the past few weeks, NZD defied fundamentals trading higher despite weaker data but reports of a deadly cow disease affecting one of the herds finally did in the currency. USD/CAD on the other hand weaved above/below 1.25. The sharp rise in Canadian bond yields and 2% increase in oil prices kept the currency pair under pressure throughout the North American trading session. Until data or oil prices reverse course, the uptrend in USD/CAD will remain intact but the pair is close to a bottom.

Author

Kathy Lien

BKTraders and Prop Traders Edge

Having graduated New York University’s Stern School of Business at the age of 18, Ms. Kathy Lien has more than 13 years of experience in the financial markets with a specific focus on currencies.