Fed Preview: Dollar’s fate hinges on Powell’s policy guidance

- The US Federal Reserve is set for another 75 bps rate hike on July 27.

- Fed Chair Powell's pledge to fight persistenly high inflation and policy guidance hold the key.

- The US dollar is basing to kickstart a fresh rally towards a two-decade high.

Despite an imminent technical recession in the US, the Federal Reserve (Fed) is determined to deliver another super-sized rate hike when it concludes its two-day policy meeting on July 27. Fed Chair Jerome Powell’s response to fighting inflation will be closely examined alongside the policy guidance for the September meeting.

Inflation peaking, not so far

After announcing the largest rate hike since 1994 in June, the Fed is set for the second consecutive 75 bps rate hike at its July policy meeting, lifting the federal funds rate range to between 2.25% and 2.5%. In doing so, the world’s most powerful central bank will be effectively ending the pandemic-era support for the US economy.

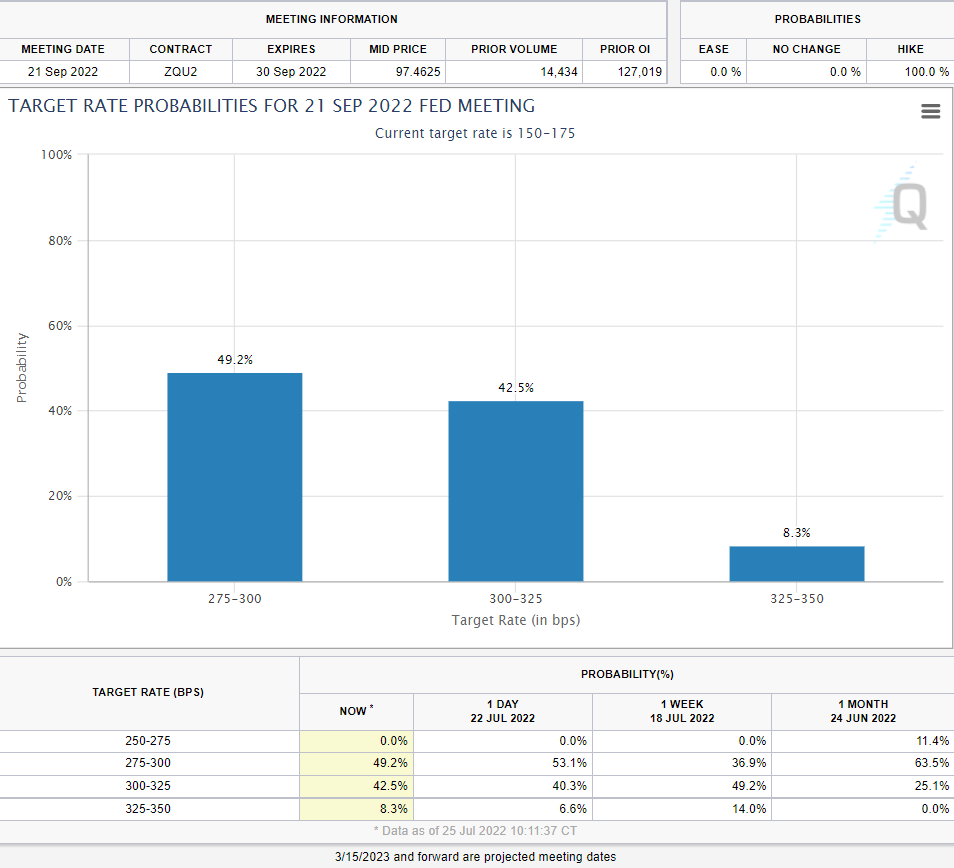

Markets are wagering a roughly 80% chance of another 75 bps rate hike by the Fed this month when compared to a 20% likelihood of a full percentage-point rise, per CME’s Fed Watch Tool. The odds of a 100 bps rate hike at the July meeting had jacked up to over 95% after the US inflation came in hotter than expected in June.

Surging gas, food and rent costs catapulted US inflation to a new four-decade peak in June, which arrived at 9.1% YoY, much higher than May’s 8.6% jump. On a monthly basis, prices rose 1.3% from May to June, another substantial increase, after prices had jumped 1% from April to May. The inflation scorcher squashed expectations of peaking consumer prices and bolstered the bets for a 1% hike in rates.

At the June post-policy meeting press conference, Powell acknowledged that the rise in the University of Michigan’s five year ahead five-year inflation expectations from 3.0% in May to 3.3% in June was the main reason behind the central bank’s bigger rate hike.

However, the June number was revised down to 3.1%, while the Fed’s closely-watched inflation measure fell to 2.8% in July, its lowest in one year. Further, Fed Governor Christopher Waller and Atlanta Fed President Raphael Bostic said that they favor a 75 bps rate hike at the upcoming July meeting. For a potential 100 bps Fed lift-off, Waller said the market is “getting ahead of itself.” These factors, subsequently, watered down expectations for a full percentage point increase.

With a 75 bps rate hike fully baked in, all eyes remain on Powell’s commitment to curbing inflation even with an increased risk of tipping the economy into a mild recession.

That said, Powell’s rate hike guidance for the September meeting and beyond will hold utmost significance, in absence of any updated projections at the July meeting.

Source: CMEGroup

The CME FedWatch Tool now shows the probability of a 75 bps September rate increase at a coin flip level while that of a 50 bps move stands at 49%. Meanwhile, money markets are pricing in an 83.4% chance that the target rate range will climb to between 3.25% and 3.5%, or higher by the end of 2022.

Powell could afford to pre-commit a 75 bps rate hike for September, given that the US labor market remains in a healthy condition. The US economy added 372,000 jobs in June, exceeding economists’ estimates for 250,000 jobs. The US unemployment rate held steady at 3.6%, while the labor participation rate ticked slightly down to 62.2%.

However, signs of peaking inflation could be the only risk, at the moment, which could dissuade the Fed from committing to larger rate hikes going forward. The Fed is ready to tolerate a weaker growth outlook so long as the inflation monster is controlled.

Trading the US dollar with the Fed announcement

The US dollar index is trying to find a base just above the 106.00 level after the recent correction from a two-decade top of 109.29. The benchmark 10-year US Treasury yields are holding near two-month lows, as a recession and a 75 bps July rate hike are fully priced in by the market.

Therefore, the dollar, as well as, the yields need Powell to leave doors open towards a bigger than 50 bps rate hike for September to keep its commitment to fighting rising prices. Technically, the dollar gauge (DXY) has been gathering support just above the 61.8% Fibonacci Retracement level of the latest upsurge to over twenty-year highs, which is aligned at 105.90.

Hawkish policy guidance from Powell will revive the bullish interest in the dollar, breaking the index from its previous week’s range to recapture the 107.50 barrier.

The abovementioned critical 61.8% Fibo support could cave in if the Fed acknowledges signs of peak inflation and/or hints at slowing down on its tightening path in the face of the economic downturn. The next downside cushion for the dollar index aligns at the ascending 50-Daily Moving Average (DMA) at 104.67.

US dollar index: Daily chart

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.