Fed funds forecast: Getting back to “neutral” will require aggressive easing

Summary

-

The FOMC has largely succeeded in its mission to return inflation to its target of 2%. However, recent data suggest the risks to the "full employment" part of the Fed's dual mandate are rising. Payroll growth has slowed and unemployment is rising.

-

As measured by the real fed funds rate, the stance of monetary policy is quite restrictive at present. In our view, the FOMC needs to get back to a "neutral" stance of policy quickly or else it risks a vicious circle of labor market weakness leading to sluggish spending, leading to further labor market weakness, etc.

-

We now look for the FOMC to cut rates by 50 bps at its meeting on September 18 with another 50 bps rate cut on November 7. We forecast the Committee will reduce its target range for the federal funds rate to 3.25–3.50% by the middle of next year, which is in the vicinity of what many observers, including us and numerous members of the FOMC, consider to be neutral.

-

We continue to forecast that the economic expansion, which has been in place since mid-2020, will remain intact due, at least in part, to aggressive Fed easing. We will be releasing a full forecast update later this week in our August U.S. Monthly Outlook.

Recent signs of labor market weakness prompt changes to our Fed funds forecast

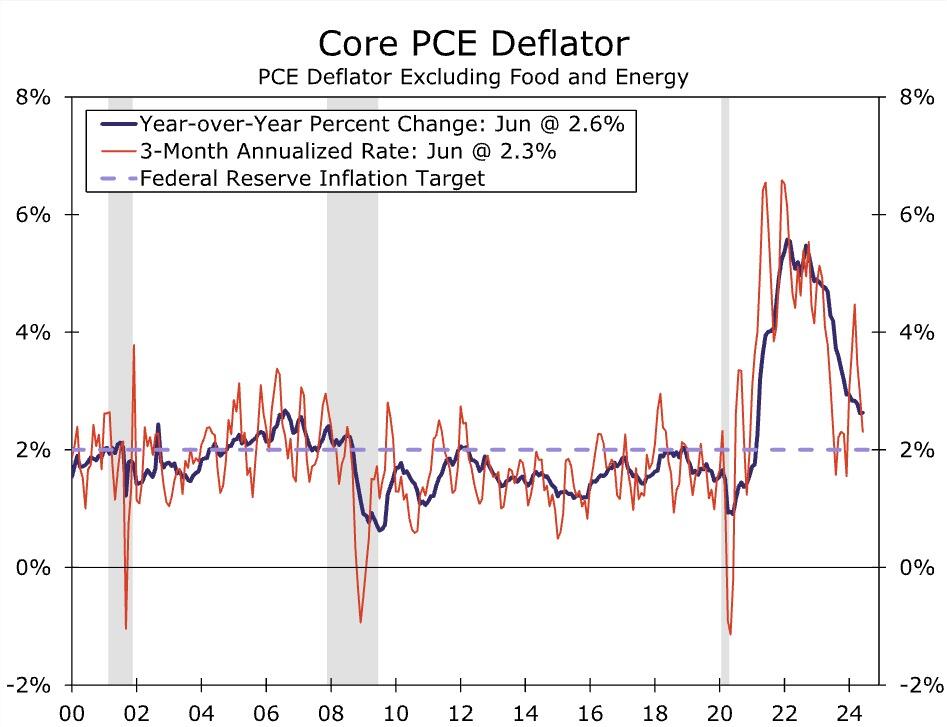

Recent economic data, especially those related to the labor market, have convinced us that Federal Reserve policymakers will soon be changing policy in a meaningful way. The Federal Open Market Committee (FOMC) had been focused almost entirely on bringing inflation back to its 2% target, an endeavor that has largely been successful. The core rate of PCE inflation, which Fed officials believe is the best measure of the underlying rate of consumer price inflation, has retreated from 5.5% (year-over-year) in September 2022 to 2.6% in June. Moreover, the core PCE price index rose at an annualized rate of only 2.3% between March and June. As we wrote in a report describing the July 31 FOMC meeting, the Committee is now "attentive to risks to both sides of its duel mandate" (i.e., “price stability” and “full employment”) rather than only emphasizing the “price stability” part of its mandate.

The risks to the labor market have become even more apparent in recent days. For starters, the number of initial jobless claims (i.e., the number of individuals filing for unemployment insurance for the first time) rose during the week ending on July 26 to its highest level in nearly a year. The number of individuals who remain jobless and therefore continue to file for unemployment compensation, which has been trending higher since late May, has risen to its highest level since November 2021 when the jobs market was still recovering from its pandemic-induced swoon. The number of respondents describing jobs as "hard to get" in the most recent Conference Board survey of Consumer Confidence edged up to its highest level since early 2021.

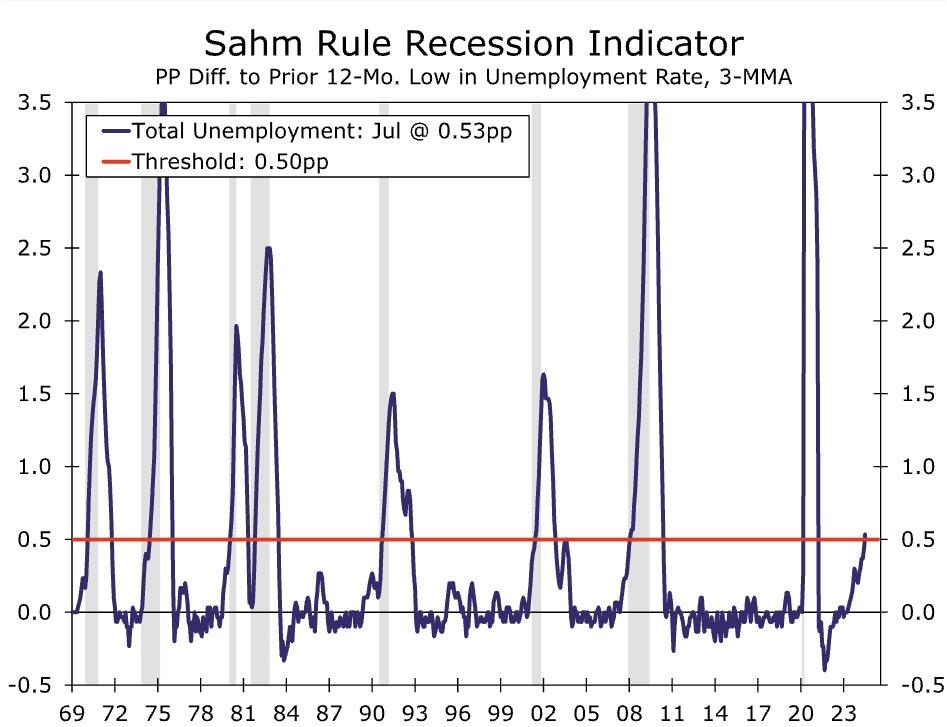

Data released on Friday showed that nonfarm payrolls rose by only 114K in July, well below the average monthly increase of 168K in the second quarter. Moreover, that gain was narrowly based with healthcare, government and leisure & hospitality accounting for most of the rise in payrolls last month. The unemployment rate jumped up from 4.1% in June to 4.3% in July, thereby surpassing the so-called “Sahm Rule” threshold, which has been a perfect indicator of recession over the past 60 years.

Source: U.S. Department of Commerce and Wells Fargo Economics

Source: U.S. Department of Commerce and Wells Fargo Economics

Author

Wells Fargo Research Team

Wells Fargo