Fed chief Powell delivers a speech this afternoon and hope of any guidance will surely be dashed

Today we get the final manufacturing PMI’s for everybody—the UK, US, France, Germany and the eurozone. The composites come on Wednesday. PMI had become the top indicator among the high frequency indicators but has lost the crown to trade nonsense.

Fed chief Powell delivers a speech this afternoon and hope of any guidance will surely be dashed. Also this week we get JOLTS, of falling importance, and the Beige Book. But the big US data this week is payrolls on Friday, forecast down to 130,000, after 177,000 in April. Some traders fret that a high number will cause more delay at the Fed. We are not so sure. We still have a labor shortage and companies may be grabbing the small cohort of skilled workers before tariffs hit the fan.

As one economist put it, we are in limbo when it comes to forecasting anything because of the haphazard decision-making in the white House. There is no Plan, and as a result, nobody can make informed decisions.

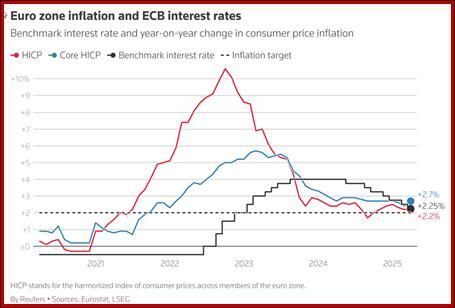

The ECB is expected to cut rates again at the policy meeting on Thursday, which will infuriate Trump, who wants the Fed to cut, too. We don’t buy the idea that the Supreme Court succeeded in warning him off firing Powell. It’s still very much on the agenda. Reuters has a killer set of sentences on the ECB rate cut: the “… nominal effective euro index is now at record highs, with the 'real' version at its strongest level in more than 10 years.

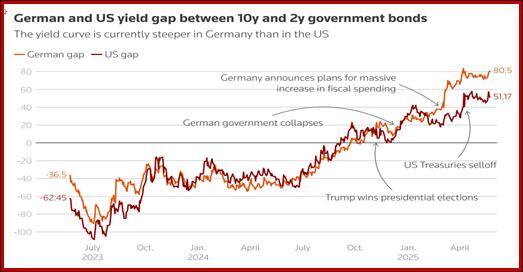

“The currency has surged even though there has been no net change in the gap between two-year government bond yields on either side of the Atlantic - usually a reliable indicator of shifts in the euro/dollar exchange rate.

“The culprits behind this trend are pretty clear: Donald Trump's tariff wars, fears of capital flight from dollar assets due to a host of concerns about U.S. policies and institutions, and Germany's historic fiscal boost that has transformed the continent's outlook.”

About that thesis that the US economy is so robust, not even Trump can wreck it: the latest Atlanta Fed GDPNpw is a jump from 2.2% on May 27 to 3.8% on Friday. Don’t get too excited—net export growth went from a negative to a positive, while consumption spending growth fell from 3.7% to 3.3% and domestic investment growth fell from -0.2% to -1.4%, So exports get all the credit, or rather, the drop in imports (yielding net exports) from tariff uncertainty gets all the credit. Imports of foreign goods are subtracted from GDP which does have the word “domestic” in its abbreviation.

Fed Gov Waller supported the idea that the tariffs will have a one-time inflationary effect and then abate, so that the Fed can cut rates later in the year.

We have a long list of worries that are damaging the dollar. One of them is the looming budget bill that includes a provision allowing Trump to tax companies and individuals from countries that have what Trump sees as “unfair taxes.” Trump does not understand taxation, of course, let alone that VAT is a sales tax on everything, not just imports from the US.

Bottom line—things are getting worse, not better.

Forecast

All markets except equities are dazed and confused by the on-again/off-again whiplash of tariff decisions. So far we are dodging the tariff bullet, as the WSJ puts it, but how long can that last? Another WSJ essay has it the US can probably muddle its way through the Trump crisis as long as he doesn’t do anything worse.

The current chapter involves the whiplash from both the EU and China over Trump’s erratic decision-making, false charges and insulting speech. The risk-off trade is back, as shown in gold and the two other safe-havens, the yen and Swiss franc.

Keep in mind that the dollar is down about 9% year-to-date but we face another futures rollover in June. Traders have to square up the old contract before entering new one, and you’d think the whole thing would be net neutral, but often the futures rollover gets hinky.

The continuing stock market bullishness is starting to be bothersome. What’s the matter with those traders and investors? We can only guess “wishful thinking.”

Tidbit: Someone just mentioned preparations for the 250th anniversary of the American revolution next year. Freedom from unfair taxation was a primary cause. The Boston Tea Party and other events took place because the citizens felt their interests and voices were not being heard in the king’s court, despite Benjamin Franklin’s best efforts. You have to wonder how many will express those same sentiments next year.

And that’s a year we have mid-term elections. Will the Dems prevail, as they did during the first Trump tenure? Maybe not. The public does like exporting illegals, and never mind that it’s immoral and almost certainly illegal to send them to prisons in foreign countries. The public likes the idea of getting rid of freeloaders on Medicaid and ridding the federal bureaucracy of fraud, waste and inefficiency, and never mind that doing it in the manner it's being done is immoral, hideously incompetently managed and partly illegal.

The Dems complain that the “savings” are going to tax breaks for the rich, but hey, this is America. We expect that.

Someone asked whether we will even have an election in 2028. Oh, yes. But two things: Trump will not agree to a peaceful transfer of power if the Dems win the White House, regardless of who is the Republican candidate. And the Dems won’t win the White House unless their candidate has an equal measure of machismo as Trump plus superb oratorical skill. The last two with those abilities were Reagan and Clinton. And oh, yeah—get rid of wokeness. You don’t have to go full-bore white supremacist like Trump to do that.

Third, we can hope that the cycle of authoritarianism will have run its course, but we have no evidence of how long these things last. The Economist magazine has a Democracy Index and Wikipedia has a good article on authoritarianism but nobody has dates for the “cycle.” Maybe we need an economic catastrophe to trigger a cycle shift. An economic catastrophe can trigger a financial markets catastrophe and surely that would lead to a political shift?

We know a cycle guy who is convinced Trump will drive away foreign ownership of US assets (you don’t have to like cycles to think that), and among other consequences, bring down the stock market. There is some merit in this argument (think Minsky) but again, what is the timeline? Trump keeps pushing it out with TACO and other desperate measures, but he is hanging on by his fingernails at the top of a very high cliff.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat