FDIC Quarterly: C&I Loan Delinquencies Tick Higher

The most recent FDIC Quarterly Banking Profile showed a general improvement in noncurrent loan rates. By sector, however, delinquency rates have diverged, with commercial & industrial creeping higher.

Energy Loan Challenges Apparent in C&I Loan Delinquencies

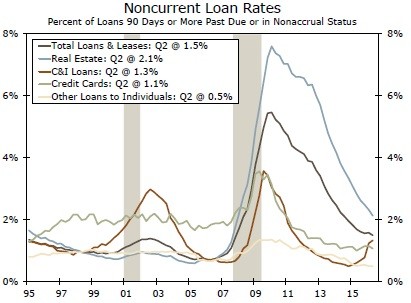

The Quarterly Banking Profile from the FDIC provides a comprehensive summary of the financial results for all FDIC-insured institutions. In the most recent report, the total amount of noncurrent loans (loans 90 days or more past due or in nonaccrual status) held by banks fell $4.8 billion, pushing the noncurrent loan rate down to 1.5 percent, the lowest level since year-end 2007. Despite this continued improvement, the noncurrent loan rate for commercial & industrial loans rose for the sixth consecutive quarter (top chart). Net loan and lease charge-offs also rose and were higher than the year before for the third consecutive quarter. Again, most of the increase was driven by C&I borrowers.

Ongoing challenges in the energy sector were the main culprit behind the continued deterioration. The energy effect is apparent when looking at noncurrent C&I loan rates by region. As the middle chart illustrates, loan delinquencies have risen the sharpest in areas with the largest exposure to the energy sector. That said, delinquencies have risen in all regions, suggesting the weakness is not solely confined to energy. Banks have responded by building reserves and have increased loan-loss provisions $3.6 billion over the past year.

Other reports corroborate these findings. The most recent Beige Book noted that "some oil and gas companies report challenges obtaining credit" in the Dallas and Kansas City districts, areas with rising delinquency rates according to FDIC data. In addition, the net percentage of banks reporting tighter standards for C&I loans to large & medium sized firms and small firms rose 15.5 and 13.1 percentage points, respectively, over the past year. With the factory sector still facing headwinds and oil prices still low relative to earlier in the expansion, we will continue to monitor conditions closely.

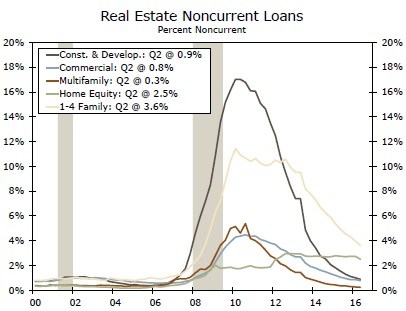

One encouraging development has been the continued decline in noncurrent loan rates in the real estate sector. Noncurrent loan rates in the multifamily space touched a post-recession low in the second quarter, as did construction & development (bottom chart).

Bank Lending Treks Higher

Unlike the divergence between sector-level delinquency rates, bank lending across the major loan categories has grown in lockstep recently. Total loan and lease balances rose 2 percent during the quarter, with all major loan categories increasing. Over the past year, total loans & leases are up 6.7 percent, with real estate, commercial & industrial and credit cards all growing north of 5 percent. Construction & development lending has risen 14.9 percent over the past year, the fastest pace of the expansion. The sluggish pace of economic growth in recent quarters does not seem to have slowed loan demand, at least thus far.

Author

Wells Fargo Research Team

Wells Fargo