Evolving Credit Standards as the Economic Cycle Matures

As the economic cycle matures, so do credit standards and demand. Recent evidence indicates both consumer credit and business lending demand has slowed, signaling a more cautious outlook going forward.

Equity Market Highs, Not So For Credit

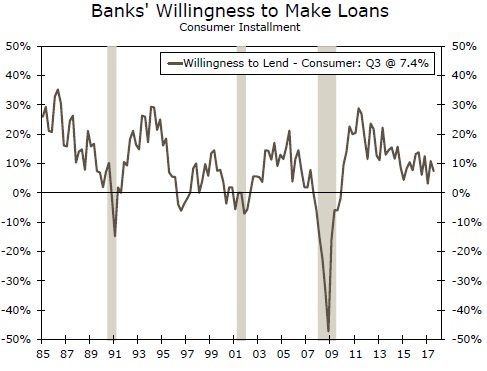

While the equity market has been recording new highs, the pattern on credit has signaled more caution on both the supply and demand side. On the supply side, the top graph illustrates that banks have been increasingly less willing to extend consumer installment credit over the past five years. The initial boom in credit willingness in 2011 has given way to caution.

This pattern repeats the trend we have witnessed in each of the prior economic cycles since the 1980s. As an economic recovery begins, banks appear very willing to extend credit. However, as the cycle matures, banks become less willing to extend credit. Apparently, banks have achieved some target level of consumer credit and, as the cycle matures, they become comfortable with that level of credit. At this stage of the current cycle, there is also a drift upward in auto loan and credit card delinquencies that may be increasing lender caution.

Consumer Demand Slows Despite Lower Unemployment

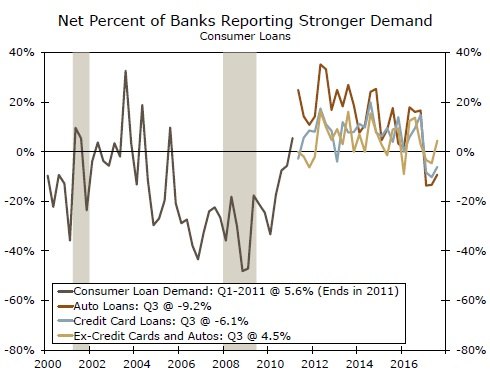

Another interesting signal of caution is that the net percent of banks reporting stronger demand on consumer loans (middle graph) has declined steadily since 2012, despite the fact that unemployment rates have fallen and job gains have been solid. In addition, home prices have risen and equity valuations have combined to boost household wealth.

One would anticipate that consumer credit demand rises with better/more jobs and household wealth, yet the Fed's survey does not show this result. The decline in demand for consumer loans intimates that households have adopted a more conservative attitude toward taking on debt. To confirm this view, the Fed's measure of household debt service as a share of household income remains at decade's level lows. In this environment, a pattern of interest rate hikes by the Fed does not appear likely to lead to a credit crunch in a way similar to the last decade's housing crunch.

Business Demand—Also Diminishing Since 2014

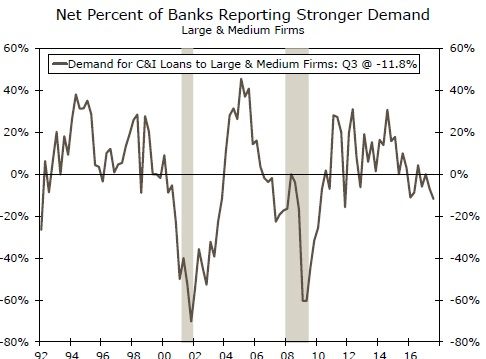

Since the peak in 2014, business loan demand by large and medium firms (bottom graph) has steadily declined so that now more banks report weaker demand.

This pattern is consistent with the view that the path of final sales in the economy has settled into the 2.0-2.5 percent range and therefore there is little need to add additional capital and thereby there is less demand for capital equipment finance. In addition, inventory change has slowed since early 2015. Since equipment finance is a derived demand from expected final demand, the steady final demand, along with a modest increase in short-term rates, is consistent with reduced quantity demanded for credit.

Author

Wells Fargo Research Team

Wells Fargo