European to start higher as Trump’s health improves

European bourses are opening on the front foot as President Trump’s condition improves. Speculation is growing that Trump could be discharged as early as today. We know that the markers hate uncertainty. The latest headlines are providing more clarity surrounding the health of the President and are easing the political uncertainty which has clouded over the markets since Trump was taken ill with covid last week. Risk appetite is on the rise meaning that risker assets such as stocks are well supported in early trade on Monday, whilst safe havens such as the US Dollar and Gold are out of favour.

Doctors are saying that they are pleased with Trump’s progress proving some relief to the financial markets. Trump contracted covid with just one month to go until the US Presidential elections adding another layer of uncertainty to elections which saw the two candidates, Jo Biden & Trump, close in the polls. Furthermore, Trump had raised doubts over whether he would accept the result of the elections.

News flow surrounding Trump’s health is expected to drive sentiment today. Signs of deterioration in his health will drag on risk appetite, pulling stocks lower. Whilst news that he has been released from hospital could lift stocks further.

Adding to the upbeat mood in the market, prospects of additional fiscal stimulus in the US have risen, according to House Speaker Nancy Pelosi

Services PMI data in focus

Today sees the release of global services PMIs. Whilst manufacturing has made an impressive recovery from the April’s contraction, service sectors, particularly in tourist destinations such as Spain and Italy are seeing the recovery wobble. Even France and German saw service sector activity back in contraction territory in the flash reading for September.

In the UK the service sector remains resilient for now. The dominant service sector saw activity expand quickly in August hitting 58.1 The more recent flash September reading printed at 55.1, slightly down from August’s peak but still a very strong number. Should Thursday’s print confirm 55.1 then Q3 will have seen an impressive expansion. However, there is a chance that the government’s most recently announced tightening of lockdown restrictions, including a curfew and new social distancing rules could knock confidence, hitting the PMI index.

Brexit talks to continue

Brexit optimism is underpinning the Pound and could provide support to the more domestically focused FTSE 250. Boris Johnson holding talks with EC President Ursula von der Leyen appears to have injected at least a bit more political momentum into talks, which will now continue this week, after little progress last week. As the clock continues to tick towards the government’s self imposed October 15th deadline ther is a growing sense of urgency between the two sides, which could be the key ingredient to a trade deal actually being done.

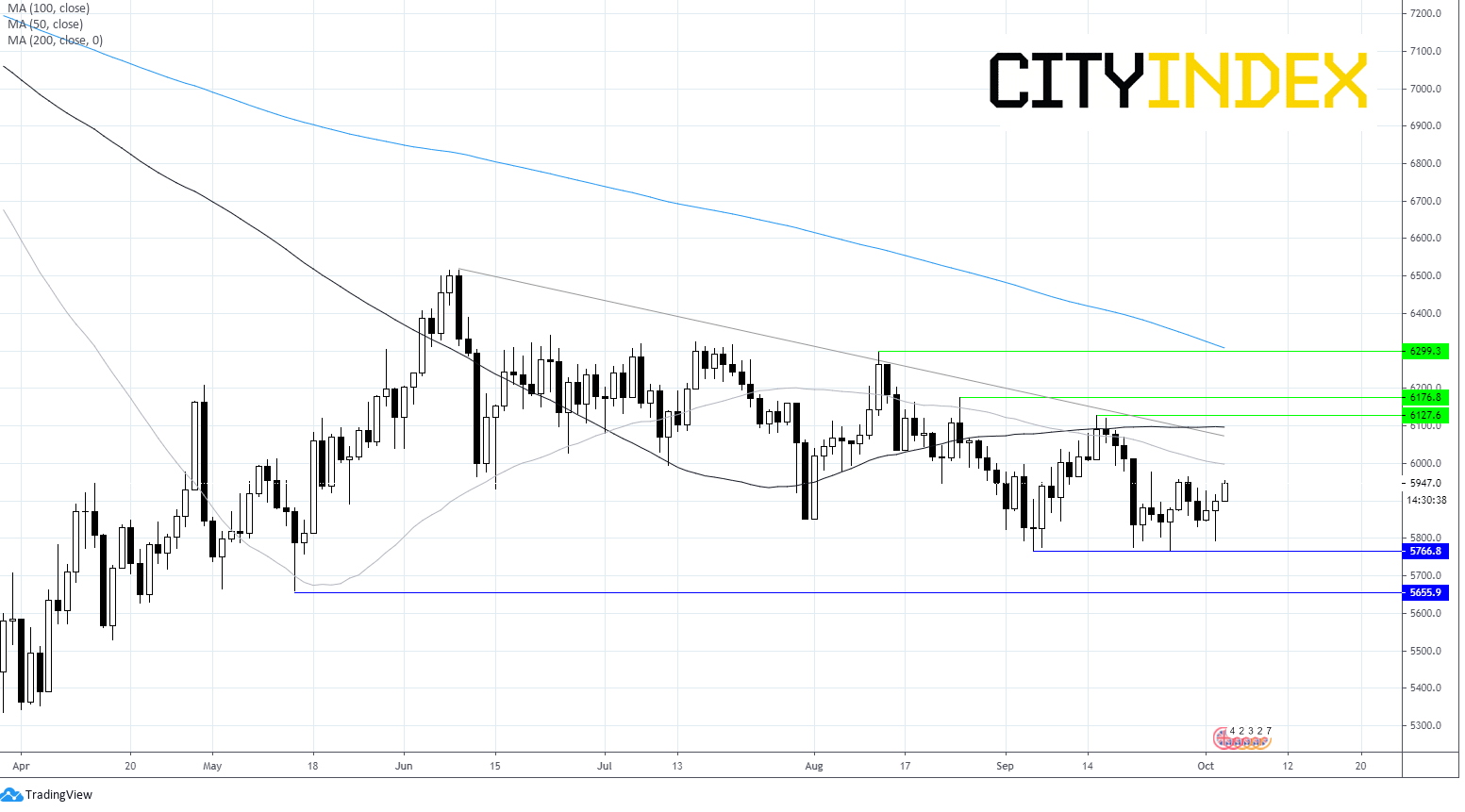

FTSE Chart

Author

Fiona Cincotta

CityIndex