EUR/USD Weekly Forecast: Bulls fight back as chances of a Fed hike remain subdued

- Signs of a resilient US labor market spurred concerns among speculative interest.

- ECB President Christine Lagarde maintained the Euro afloat with her hawkish words.

- EUR/USD battles to regain its longer-term bullish strength ahead of central banks’ decisions.

The EUR/USD pair fell throughout the first half of the week, changing course on Thursday after bottoming on Wednesday at 1.0634, its lowest in more than two months. The US Dollar benefited from a risk-averse environment, mostly due to fears over the possibility of the United States (US) falling into default. As these concerns faded, EUR/USD recovered, ending the week little changed at around 1.0720.

Debt-ceiling deal done

Financial markets remained concerned even after US President Joe Biden and House Speaker Kevin McCarthy announced they reached an agreement on the debt ceiling on Sunday. At that point, however, the deal was pending Congressional approval. Yet as the days went by and the bill passed different stages, the mood began improving. Finally, on Thursday, the US Senate voted to pass the bill that suspends the debt-ceiling limit until January 2025. The bipartisan deal includes military spending up to $886 billion in 2024, with a 1% increase in the next year and $704 billion of discretionary spending. Given that planned increases are below inflation, the difference will be a spending cut.

Meanwhile, the Euro got boosted by comments from European Central Bank (ECB) President Christine Lagarde. In a conference at the German Savings Banks on Thursday, Lagarde said that inflation is too high and is set to remain so for too long, adding there is no clear evidence underlying inflation has peaked. She then noted that policymakers still have ground to cover on rates, hinting at least two more hikes in the docket.

On a positive note, the Eurozone Harmonized Index of Consumer Prices (HICP) rose by 6.1% YoY in May, according to preliminary estimates, easing from 7% in April. The core HICP was up 5.3% in the same period, easing from the previous 5.6%.

Resilient US job market

US data introduced some noise by the end of the week amid signs of a still strong labor market. Challenger Job Cuts showed that US-based employers announced 80,089 cuts in May, a 20% increase from the 66,995 cuts the previous month. Also, the ADP survey showed the private sector added 278K new jobs, much higher than the 170K expected.

Additionally, Initial Jobless Claims rose by 232K in the week ended May 26, while Q1 Nonfarm Productivity improved to -2.1%. On the contrary, Unit Labor Costs in the three-month to March were up by 4.2%, slowing from the previous 6.3%. Finally, the country released the May ISM Manufacturing PMI, which contracted by more than anticipated to 46.9 from 47.1 in April.

Stock markets initially fell on speculation the Federal Reserve (Fed) may proceed with more rate hikes, but easing wages pressures on inflation finally boosted the mood and equities. The US Dollar fell the most on Thursday after employment-related data and the approval of the debt-ceiling bill. Also, the poor outcome of the Manufacturing PMI limits the Fed’s ability to hike rates. Early on Friday, the CME FedWatch Tool showed market participants were pricing in less than 30% chances of a June hike.

Speculative interest was shocked again on Friday, following the release of the US May Nonfarm Payrolls report. The country added 339K new jobs, much more than the 190K expected. The Unemployment Rate jumped to 3.7%, while the Labour Force Participation Rate held steady at 62.6%. Finally, Average Hourly Earnings increased by 4.3% YoY, slightly below the previous 4.4%. The US Dollar surged following the release, with EUR/USD retreating from a weekly high of 1.0778 but retaining modest weekly gains.

A resilient labor market is not good news for the Fed. It could result in higher wage pressures, which can push inflation back up. At the same time, if the central bank decides to go for more rate hikes, it also lifts the risk of a recession and even unwinds a steeper banking crisis.

As the week comes to an end, the CME FedWatch Tool shows roughly a 68% chance of no rate hikes in June and a 32% chance of a 25 basis points (bps) hike.

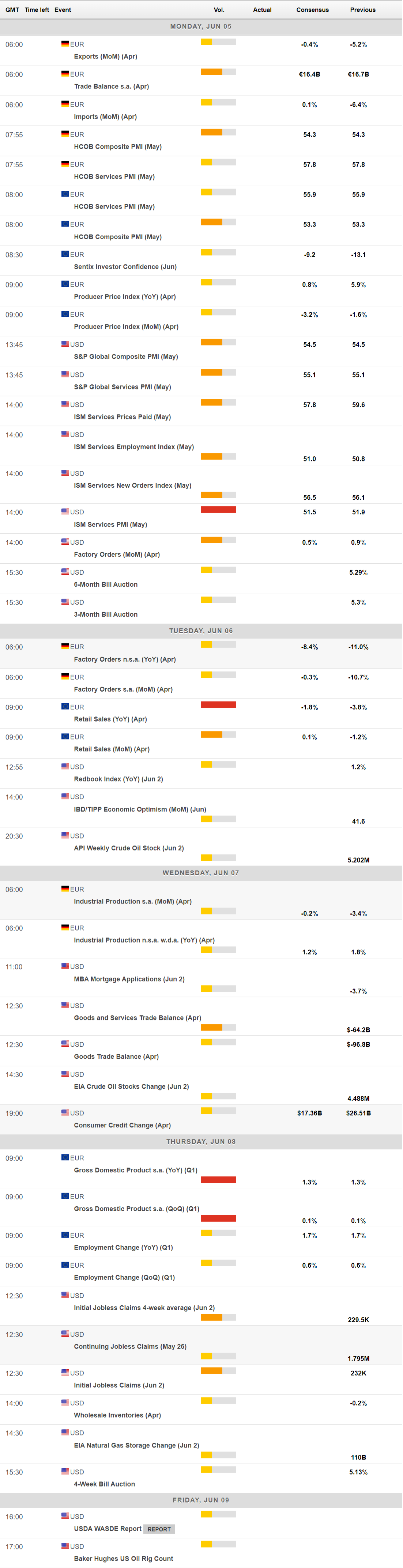

The upcoming week will bring the US May ISM Services PMI, foreseen at 51.5, down from 51.9 previously. The EU will publish April Retail Sales and the final estimate of the Q1 Gross Domestic Product (GDP). Ahead of the central banks’ meetings in mid-June, European and American policymakers will enter a blackout period.

EUR/USD technical outlook

The EUR/USD pair trades just below the 61.8% retracement of its 2022 yearly slump at 1.0745. At the same time, the weekly chart shows that technical indicators are bouncing modestly from their midlines, supporting an upward continuation. Nevertheless, the pair stays under all its moving averages, with the 20 Simple Moving Average (SMA) flat at around 1.0800, while below the longer ones, which somehow limits the chances of a steeper recovery.

The daily chart, on the contrary, shows that bears are still in control of EUR/USD. The Momentum indicator is retreating from around its 100 level, while the Relative Strength Index (RSI) indicator consolidates at around 42, maintaining the risk skewed to the downside. Furthermore, a firmly bearish 20 SMA is crossing below a directionless 100 SMA, both in the 1.0810 region, anticipating additional selling pressure.

EUR/USD needs to clear the 1.0810 region to regain its bullish traction, with room to extend its recovery towards the 1.0900 price zone. Gains beyond the latter seem unclear at this point, although the next relevant resistance area comes at 1.0940/60.

Renewed selling pressure below 1.0700 should push the pair towards the multi-week low posted last Thursday at 1.0634, while further declines should expose 1.0507, the 50% Fibonacci retracement of the 2022 yearly slump.

EUR/USD sentiment poll

EUR/USD sentiment poll

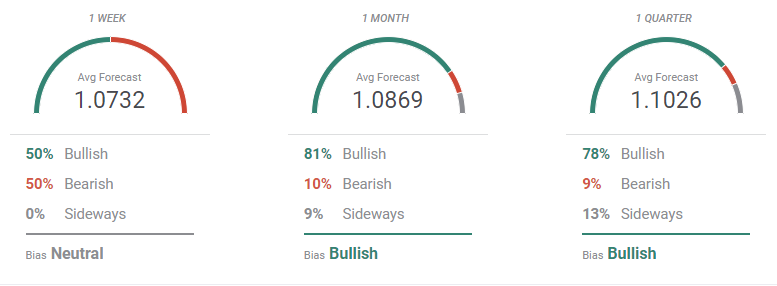

According to the FXStreet Forecast Poll, EUR/USD is likely to regain its bullish bias. The pair is expected to remain neutral in the near term, as on a weekly basis, it is averaging 1.0732. However, bulls take over in the monthly perspective accounting for 81% of the polled experts and with an average target of 1.0869. Bulls are also a large majority in the quarterly view, with only 9% of the polled experts betting on a slide and the pair is seen recovering the 1.1000 mark.

The Overview chart also hints at a potential recovery. The three moving averages have lost their bearish slopes, and while the shorter one remains flat, the longer ones are slowly recovering their upward strength near multi-month highs. Bulls seem to hesitate in the near term, as most targets accumulate between 1.0600 and 1.1000 in the monthly perspective but the range in the quarterly view is up to 1.0900/1.1200.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.