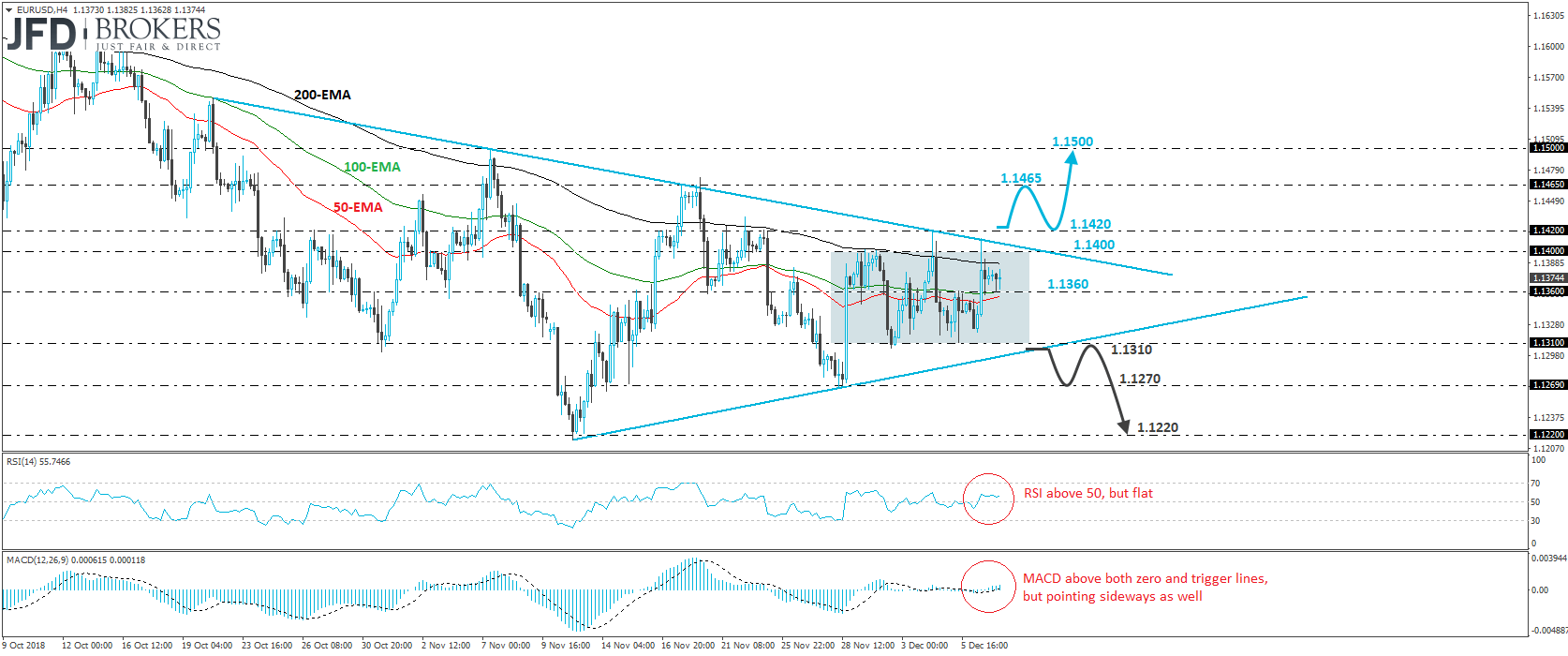

EUR/USD Stuck Within a Range

EUR/USD traded higher yesterday, breaking above the resistance (now turned into support) barrier of 1.1360. However, the recovery was rejected once again slightly above the 1.1400 zone, near the downside resistance line drawn from the peak of the 22nd of October. Then, the pair pulled back to challenge the 1.1360 zone as a support this time. The rate continues to trade within the sideways range that’s been containing most of the price action since the 28th of November, between 1.1310 and 1.1400, and thus, we will adopt a flat stance for now.

We would like to see a decisive break above 1.1420 before we start examining whether the near-term outlook has turned to positive. Such a break could confirm the upside exit out of the aforementioned range, as well as the break above the downside resistance line taken from the peak of the 22nd of October. The bulls could then decide to drive the battle towards the 1.1465 hurdle, the break of which could open the way towards the psychological zone of 1.1500, which is also marked by the peak of the 7th of November.

Taking a look at our short-term oscillators, we see that the RSI lies above its 50 line but points sideways. The MACD, although above both its zero and trigger lines, is flat as well. Both these indicators suggest weak momentum and corroborate our choice to stay sidelined for now.

On the downside, we prefer to wait for a dip below the 1.1310 barrier, or even better, below the tentative upside support line drawn from the low of the 12th of November before we start assuming that the bears have gained the upper hand. Such a dip could initially target the low of the 28th of November, at around 1.1270, the break of which could carry extensions towards the 1.1220 zone, near the low of the 12th of the month.

Author

JFD Team

JFD