EUR/USD Price Forecast 2023: Control inflation or avoid recession? Is there a recipe for success?

- The US Federal Reserve and the European Central Bank ended 2022 with a bang.

- Financial markets will continue to depend on inflation and economic growth.

- The European energy crisis could easily turn into a global one next winter, affecting both Euro and US Dollar.

- EUR/USD long-term corrective advance will likely continue in the first quarter of 2023.

The EUR/USD pair kickstarted 2022 with a weak tone, but at the time, nobody would have imagined it would end up bottoming at 0.9535. Financial markets were generally optimistic about the post-pandemic economic comeback, despite some residual aftertaste mostly linked to putting back the global machine in motion.

The abrupt end of cheap-money-supported US Dollar

Cheering the post-pandemic economic comeback was short-lived, as global economies faced another unexpected hit: inflation. Running hot Consumer Price Index (CPI) became the new norm amid supply chain disruptions and soaring consumer demands, with inflation in major economies reaching multi-decade highs and catching government and policymakers off-guard. “Temporal” inflation from 2021 shifted to entrenched at the beginning of 2022.

As an immediate effect, demand for near-term United States government bonds soared. US Treasury bond yields jumped to multi-year highs, but more relevantly, the yield on the 2-year Treasury note surged beyond that of the 10-year note, usually read as an early sign of an upcoming recession. The US Dollar (USD) run alongside and reached multi-decade highs against most major rivals.

Central banks thought it was a good idea to shift from ultra-loose monetary policies to massive quantitative tightening to cool down inflation. The US Federal Reserve (Fed) kick-started hiking rates by modest 25 basis points (bps) in March 2022, to a range of 0.25%-0.50%, but it was quickly followed by five consecutive 75 bps hikes.

Inflation kept running stubbornly hot in the United States, although the first encouraging signs surged by the end of the third quarter. The United States Consumer Price Index rose at annual pace of 9.1% in June, its highest level in over forty years. The CPI rose at a slower pace from there on, and market participants rushed to price a slower pace of hiking, giving the Euro (EUR) a chance to recover part of the ground lost throughout the first nine months of the year.

Across the pond, the situation has been quite different. Well into the final quarter of the year, price pressures keep raising while European Central Bank (ECB) policymakers waited until December to take a more aggressive stance. The Euro Area annual CPI rose by 10.1% YoY in November, while that of the European Union was 11.1% in the same period. Eurozone inflation peaked at a multi-decade high of 10.6% in September.

The European Central Bank had been far more conservative throughout the first half of the year. ECB President Christine Lagarde and company pulled the trigger for the first time in July, hiking rates by 50 bps, followed by two-consecutive 75 bps hikes in September and October. As its United States counterpart, the ECB slowed the pace of tightening and hiked by 50 bps in December.

Federal Reserve and European Central Bank shift again

Central bank December announcements were seen as hawkish, and both Christine Lagarde and Fed Chair Jerome Powell provided volatility material. On the one hand, the Federal Reserve Chairman surprised market players with his tough words, as he noted that the Fed still has hikes under its sleeve. “Historical experience cautions strongly against prematurely loosening policy. I wouldn’t see us considering rate cuts until the committee is confident that inflation is moving down to 2% in a sustained way,” Powell added.

The Federal Reserve Summary of Economic Projections (SEP) foresees no rate cuts in 2023, while policymakers upwardly revised inflation forecasts while taking down growth prospects.

ECB President Christine Lagarde, on the other hand, said that policymakers expect to raise rates "significantly further" because inflation is far too high, adding that it is “obvious” that more 50 bps hikes should be expected for a period of time. Quite a hawkish shift to her usually moderated words.

So, the Fed and the ECB converged in slowing the pace of tightening but pledged for more hikes ahead, even at the risk of hurting economic growth. Powell and Lagarde also converge in putting inflation above growth. And it is logical. Central banks’ main target is to keep inflation under control, not to boost the economy.

Their monetary decisions will drain massive liquidity, clearly undermined economic progress. The risks of a downturn are high, while price pressures remain elevated heading into 2023.

Economic growth to keep slowing

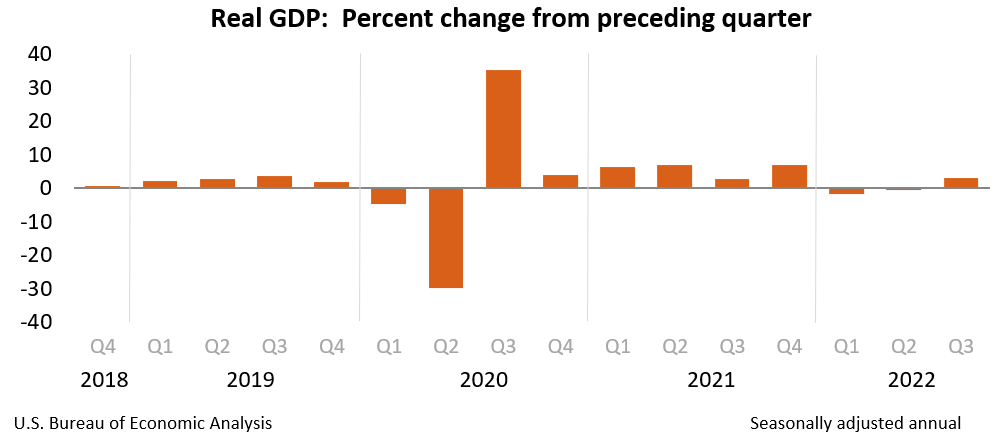

Let’s take a look at growth figures. In the United States, real Gross Domestic Product (GDP) increased at an annual rate of 2.9% in the third quarter of 2022, following a 0.6% contraction in the second quarter. The GDP also contracted in the first quarter of the year, down 1.4%, meaning the country technically fell into a recession. Panic arose, but the US Federal Reserve remained stubbornly committed to tame inflation. Equities plummeted on fears economic progress would soon stall, while bets on continued inflationary pressures pushed near-term US Treasury yields further up.

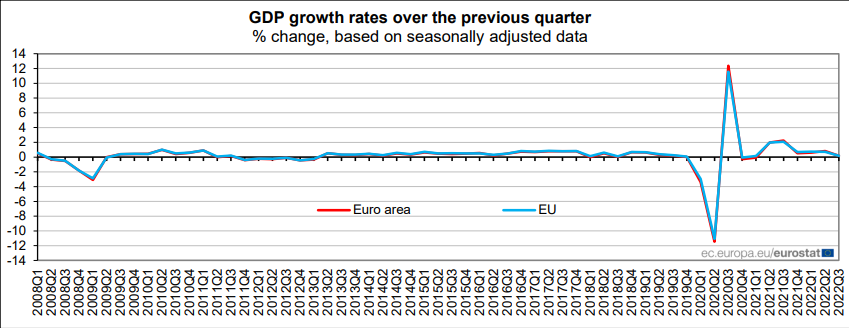

In the Euro Area, seasonally adjusted Gross Domestic Product increased by 0.3% compared to the previous quarter, according to Eurostat. In the second quarter of 2022, the GDP had grown by 0.8%, which followed a modest 0.6% uptick in the previous quarter.

But the European Union faces yet one more challenge. Russia decided to invade Ukraine. By the end of February, Russian President Vladimir Putin announced a special operation “aiming for the demilitarisation and denazification” of Ukraine. As a result, Western nations imposed unprecedented sanctions against Moscow, as the latter illegally annexed Ukraine's Donetsk, Luhansk, Zaporizhzhia and Kherson regions. As a result, the Kremlin hit Europe where it hurts the most: energy provision.

Sanctions from the European Council include “targeted restrictive measures (individual sanctions), economic sanctions and visa measures.” They also imply some import and export restrictions, among which, oil and derivatives became the Achilles heel of Europe.

Energy crisis about to worsen

In June 2022, the European Council adopted the sixth package of sanctions that, among others, prohibits the purchase, import or transfer of seaborne crude oil and certain petroleum products from Russia to the EU. The restrictions apply from 5 December 2022 for crude oil and from 5 February 2023 for other refined petroleum products. A temporary exception was made for imports of crude oil by pipeline, particularly for some EU member states that have no alternative options.

Moscow’s response to sanctions did not take long. The Kremlin started reducing and finally cut off its gas supply to Europe ahead of the winter, generating an energy crisis and further fueling price pressures. Energy shortages lead to skyrocketing household energy bills across the Old Continent, which further fueled inflationary pressures while forcing governments to take different measures to cool down prices.

Before the war started, Russian gas accounted for roughly 40% of European needs. By November 2022, the EU has succeeded in filling storage capacity to bare with the winter, but shortages for 2023 are on the docket, particularly if Russian pipeline gas flows stop completely and amid expectations global demand will continue to grow.

Hard landing, soft landing or what?

Heading into 2023, there is uncertainty over central banks succeeding in guiding economies into a soft landing. That is, controlling inflation without triggering recessions. As said, price pressures are still too high, with inflation running over three times faster than tolerable.

Grappling with global energy shortages will be the main challenge for the upcoming year, and not just for the European Union. As China moves away from its zero-covid policy, demand for fossil fuels in the country is expected to soar. If Russia persists in its war with Ukraine – and would likely be so if Vladimir Putin retains power – shortages of oil, natural gas and coal will increase, while prices will remain high. That will affect both the United States and the EU's ability to prepare for the 2023-2024 winter and maintain inflation far beyond policymakers’ comfort levels.

Persistent inflationary pressures should lead to additional rate hikes, which will end up curbing growth prospects among major economies.

Central banks have pledged more interest rate hikes throughout the first half of 2023, against the market’s belief the end of the tightening cycle is near. Potential rate cuts should be put in the freezer for the next year.

Europe will likely suffer much more than the United States amid its dependence on Russian energy. It will be tougher for the Union to find alternative sources/providers, particularly if Chinese demand resurges as expected. In such a scenario, production costs will likely raise, making local industries uncompetitive.

After years of working towards replacing energy sources with green ones, the EU may have no other choice but revive nuclear power. That would be another burden for local businesses that dedicated time and resources to shift towards renewable sources of energy.

The EUR/USD pair fell eight out of the twelve months of the year, recovering the most in November when market participants rushed to price in a slower pace of rate hikes in the United States, and the growing chance of a soon-to-come end of the tightening cycle. However, Fed Chairman Jerome Powell not only cooled down such expectations, but ECB President Christine Lagarde surprised with a hawkish stance.

The pair rose throughout the first half of December amid the former bullish momentum based on speculation about easing quantitative tightening and that rate cuts were around the corner. But that was not the actual scenario and EUR/USD actually trades below pre-central banks’ announcements, as the US Dollar has re-gained some footing.

EUR/USD technical outlook

Analyzing EUR/USD monthly chart, the roughly 1,100 pips recovery from the multi-year low at 0.9535 looks like a correction. Measuring the 2022 decline from 1.1494 to the mentioned low, the 61.8% Fibonacci retracement stands at around 1.0735, also the December monthly high.

Nevertheless and according to the same chart, technical indicators have lost their upward strength within negative levels after correcting extreme oversold readings, reflecting the long way to go before bulls actually take control. In the same chart, the 20 Simple Moving Average (SMA) maintains a firmly bearish slope below the longer ones which also head south, reflecting long-term bears´ dominance.

Down to the weekly perspective, the risk of an upcoming decline seems well limited. The 20 SMA is currently crossing above the 50% retracement of the year’s decline at around 1.0510, although the longer moving averages present neutral-to-bearish slopes far below the shorter one. The Relative Strength Index (RSI) consolidates above 60 without signs of upward exhaustion, maintaining the risk skewed to the upside. Finally, the Momentum indicator is bouncing from around its midline, after correcting overbought conditions reached mid-November.

Ever since the end of 2014, the 1.1460/80 price zone has been a tough bone to break one way or the other. With EUR/USD trading over 800 pips below the level, and with prospects of additional rate hikes at both shores of the Atlantic, the chances that the pair could reach such a price zone in the first quarter of 2023 are not much. However, if it manages to clear the aforementioned Fibonacci resistance, the pair can advance towards the 1.1060/1.1120 price zone. For the tie to chance and bulls to retake long-term control of the pair, a monthly close above 1.1500 would be required.

Euro bears could become more confident if the pair breaks below 1.0300, where EUR/USD also has the 38.2% Fibonacci retracement of the 2022 decline. Below the level, speculative interest will be looking to retest parity, although another slide below the psychological threshold will depend on growth imbalances, rather than central bank decisions. However, if the US Federal Reserve resumes aggressive quantitative tightening, the pair may well plunge towards 0.9500. This scenario seems more likely towards the second quarter of the year.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.