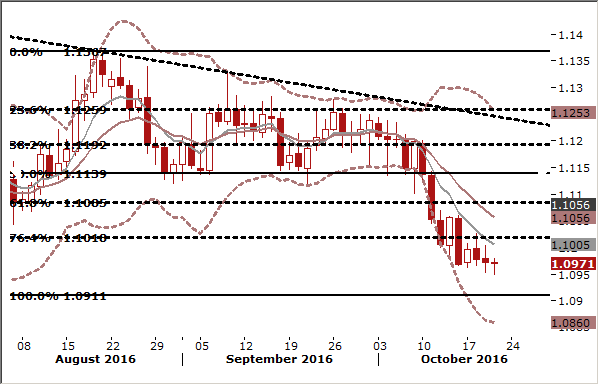

EUR/USD: Draghi Will Set A Direction

-

The EUR stood near a three-month low ahead of a European Central Bank decision (rate announcement: 11:45 GMT, press conference: 12:30 GMT). Today’s Q&A session will be closely scrutinized in the wake of recent tapering speculation. Top ECB officials denied the Governing Council discussed a possible tapering of asset purchases. Therefore, we cannot expect ECB President Mario Draghi to add much on this topic. We also doubt he will drop explicit hints about the Governing Council’s current thinking of additional stimulus: that would be premature without full information from the committees and before the updated projections. While a majority of the ECB likely favours an extension of QE beyond March 2017 there are a handful of hawks that are likely not convinced of the need to continue with QE. We think Draghi will just stress that the central bank remains committed to do whatever is needed to meet its price mandate.

-

If there is no hint on a possible extension of asset purchases beyond March 2017 at today’s ECB press conference, the EURUSD could find its way back to the area of 1.1085-1.1140. But if Draghi puts greater emphasis on the need for more stimulus, further drop in the EUR/USD is likely.

-

Daily low on October 19 at 1.0955 and daily low on July 25 at 1.0952 are the nearest support levels. We do not expect they will be broken before the ECB statement.

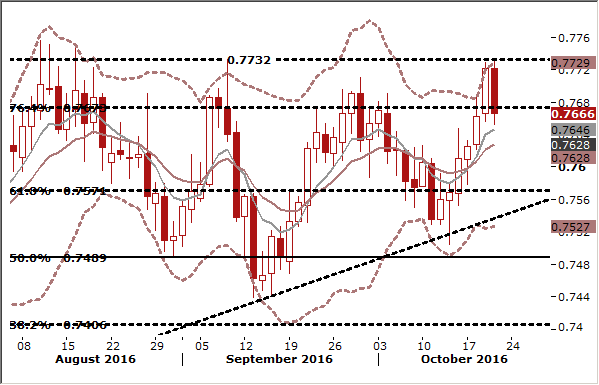

AUD/USD Rally Stopped By Jobs Data

-

Australian employment unexpectedly fell 9.8k in September as firms shed a huge 53k full-time jobs. Thursday's data from the Australian Bureau of Statistics showed the unemployment rate stayed at a three-year trough of 5.6%, but only because more people stopped looking for work. Indeed, the participation rate dropped to its lowest since May 2014 at 65.5%. The fall in employment in September was also the second straight month of declines and confounded market forecasts for a rise of 15k.

-

Just this week Reserve Bank of Australia Governor Philip Lowe emphasised that rising underemployment and weak hours worked meant there was a lot more slack in the labour market than the unemployment rate on its own might suggest.

-

Consumer price data for the third quarter due next week will be crucial. A very low reading for underlying inflation could make a case for an easing as early as the RBA's November 1 board meeting, but it is not our baseline scenario. Surprisingly low readings for inflation prompted the RBA to cut rates in August and May, taking them to a record low of 1.5%.

-

Interbank futures still imply a 16% probability of an easing in November, though the AUD did take a knock on the jobs report.

-

The AUD/USD rise was stopped near September high (0.7732), but the long-term outlook remains bullish. The nearest support level is 7-day ema at 0.7644.

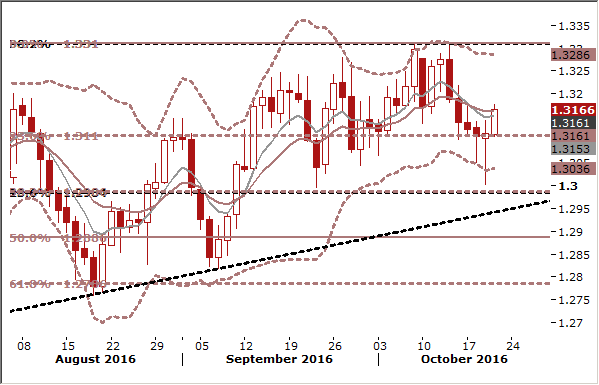

USD/CAD: Bank Of Canada Offsets Oil Surge

-

The Bank of Canada held its overnight rate at 0.5%, as widely expected. The bank cut its growth forecast and said it actively discussed adding more monetary stimulus to speed up the nation's economic recovery, surprising financial markets by shifting tone dramatically after its initial rate decision.

-

Citing a looming slowdown in Canada's long housing boom and a weaker outlook for exports, Bank of Canada Governor Stephen Poloz said the central bank had considered easing monetary policy. He said that uncertainty around the U.S. election and business investment, the Canadian housing market, and the commodity cycle kept the bank from adding stimulus.

-

Poloz revealed the stimulus discussion in his opening statement to reporters more than an hour after publication of the rate decision, wrong footing financial markets that were not expecting the dovish shift.

-

It was the second time in six months the central bank admitted it had considered adding more stimulus to the economy to counter persistent disappointments in growth and exports.

-

Poloz later told a Senate committee that the bank did not have a lot of traditional tools left to boost the economy, but could use unconventional measures like forward guidance, asset purchases, quantitative easing and negative interest rates.

-

The bank's comments cemented the belief that Canada will not raise rates in the foreseeable future, and could even cut rates, even with the U.S. Federal Reserve expected to hike further. Our economists do not expect further monetary easing in Canada in the coming months.

-

The CAD had strengthened to a nearly four-week high after a shock drop in U.S. crude inventories led to a surge in prices for oil yesterday. But those gains were erased after the central bank said it had considered to ease its policy.

-

In our opinion the long-term trend on the USD/CAD depends on trends in oil market. Oil prices fell on Thursday on profit-taking after markets rallied the previous day due to a draw in U.S. stocks and an expectation of an OPEC-led cut in production, but the overall market mood remains bullish. The OPEC plans to meet on November 30 and hopes to decide on a half a million to 1 million barrels per day oil production cut, and the producer cartel hopes that non-OPEC exporters, especially Russia, will cooperate. Saudi Arabia's Energy Minister Khalid al-Falih said that the cut will help reduce a huge overhang of supplies and stimulate new investments in the sector.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.