EUR/PLN 4.60 is last intermediate support

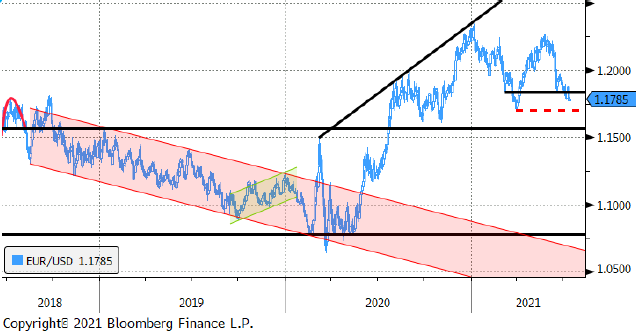

The Fed’s dot plot launched US short term yields and propelled the dollar in lockstep. Even though the Fed is not in a hurry, it will still outpace the ECB in terms of policy normalisation. This monetary divergence along with a more general fragile risk climate tilted the EUR/USD balance in favour of the greenback. 1.1704 is the key technical reference to the downside.

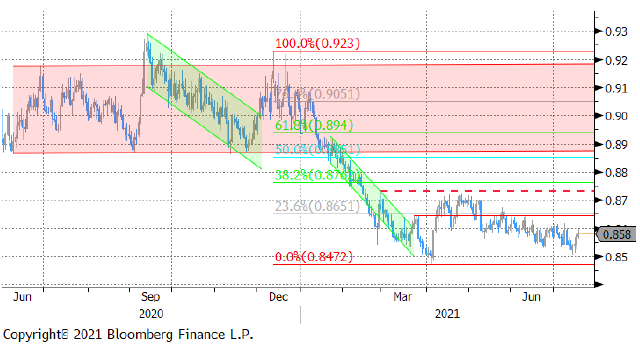

Sterling is strengthening only very gradually. The Bank of England prefers to err on the side of caution even though inflation and the economy is running hot. A few MPC members are having second thoughts on the “temporary” nature of inflation but that view isn’t shared by the rest of the MPC nor by markets.

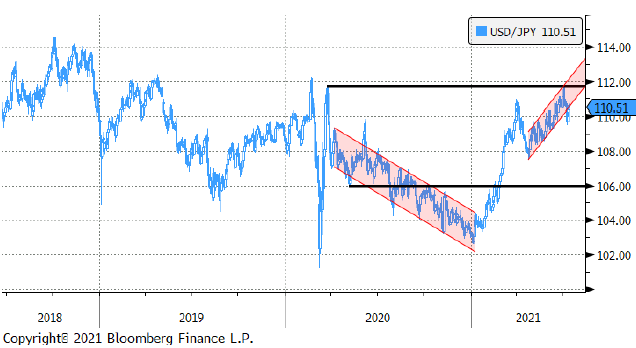

The Chinese government proposing to ease monetary policy turned lingering growth fears into outright risk-off early July. USD/JPY fell out the upward sloping trend channel and is having difficulties re-entering as cautiousness dominates.

After attacking but failing to breach support at EUR/CZK 25.45, the Czech krone fell prey to a modest profit-taking move. Markets are currently weighing the (discounted) upcoming tightening cycle against the shaky risk sentiment that could ease some pressure on the CNB for fast tightening.

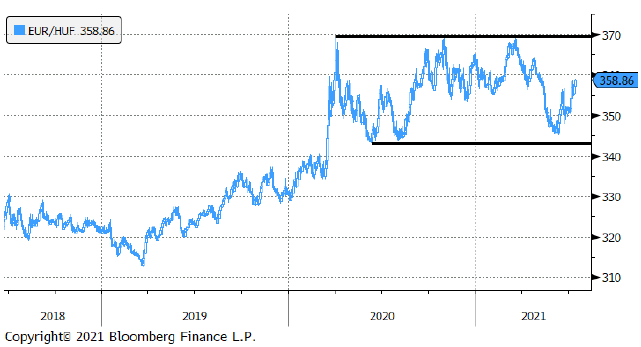

The MNB made very clear it will act against rising inflation by hiking policy rates at the next meetings. This didn’t prevent the HUF from being dragged in a broader CE currency sell-off that’s also spurred by legal woes with the EU. We’re closely watching the MNB reaction function: will it double down on rate hikes to prevent “a weaker HUF, stronger inflation” doom loop or back down due to increased growth uncertainty?

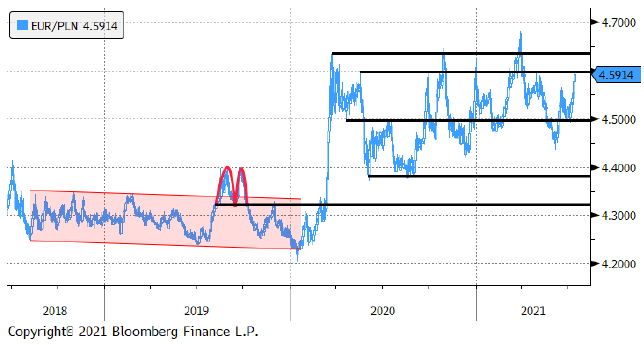

The zloty faces the same issues as the HUF: growth uncertainty and a legal dispute with the European Commission. Additionally, the NBP pushed back against any market speculation on rate hikes. With inflation remaining elevated as well (4.4% y/y), it risks triggering the vicious circle described above. EUR/PLN 4.60 is last intermediate support (for the zloty) before the pandemic lows. The zloty faces the same issues as the HUF: growth uncertainty and a legal dispute with the European Commission. Additionally, the NBP pushed back against any market speculation on rate hikes. With inflation remaining elevated as well (4.4% y/y), it risks triggering the vicious circle described above. EUR/PLN 4.60 is last intermediate support (for the zloty) before the pandemic lows.

Author

KBC Market Research Desk

KBC Bank