EU sectors in 2026: Tech outperformance, manufacturing growth gaps, small consumer gains

Production in many sectors should grow between 1% and 1.5% in 2026. Construction and staffing should see the biggest gains versus 2025, but most EU firms won't notice big changes in the growth outlook. The tech sector could grow at the speed of light, but that still pales when compared to tech growth in the US and China.

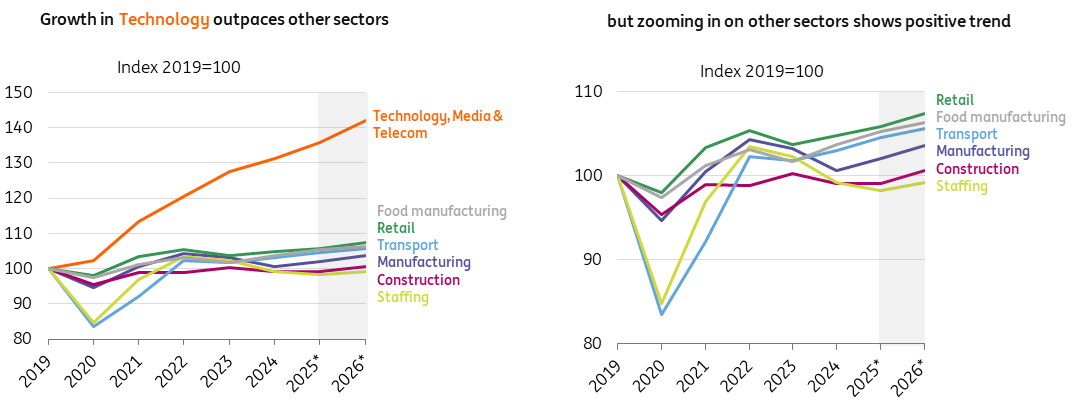

Positive growth for major sectors in 2026

Technology is an outperformer, compared to other EU sectors

Production growth in the tech sector is expanding rapidly at around 4.5% and clearly outpaces other sectors. Organisations keep investing in their digital capabilities with continued double-digit growth in IT spending, including on data centre systems such as AI-optimised servers.

Growth in the tech sector is also supported by a range of tech-related incentives at the EU level, such as Horizon Europe/EIC. However, overall growth for the industry lags the US and China. Investment growth for data centres, for instance, shows that the EU is not able to keep up the pace.

Mind the growth-gap between heavy and high-tech industries

In EU manufacturing, 2026 is expected to be the second consecutive year of production growth, despite the ongoing headwinds for the energy-intensive industry. In response to the US tariffs, tariff pass-through by EU exporters to US import prices is almost 100%. So, US companies and consumers are paying almost all direct tariff costs. Furthermore, EU companies started shifting some of their sourcing and production to local US factories and increased focus on other export markets.

The main contribution to growth in manufacturing is set to come more from high-tech sub-sectors profiting from investments in defence, AI and electrification, as well as from tech-driven industries like biotech, aerospace and pharmaceuticals. The EU’s Recovery and Resilience Fund (RRF) will continue to stimulate investments in the manufacturing sector.

For manufacturers of building materials, it’s a positive trend that the EU construction sector shifts from stagnation to growth in 2026. Prospects for residential construction look more promising, with the issuance of new permits growing steadily. Output in the infrastructure segment will be boosted by a final series of grants and loans out of the EU’s RRF, which still holds over €200 billion in non-committed funds. Besides that, we’ll likely see the first projects funded by Germany’s €500bn investment plan for infrastructure and climate by the end of 2026. Modest growth in manufacturing and construction is a positive signal for the staffing industry, for which we anticipate a gradual improvement in demand for temporary workers in 2026.

The competitive landscape for manufacturing will continue to be very volatile in 2026. Renewed trade tensions can quickly reduce competitiveness. The positive impulse from efforts to diversify trade, such as the Free Trade Agreements with Mercosur and India will only materialise over time. Meanwhile, the implementation of EU policies (and the possibility of last-minute changes) is another major factor influencing the competitive environment. This includes the further roll-out of the Carbon Border Adjustment Mechanism (CBAM) and measures on non-EU steel imports.

Consumer-oriented sectors: Expect marginal gains rather than big improvements

High inflation rates have turned shoppers into savers. Further improvements in purchasing power and a minor drop in inflation in the EU are favourable for consumer-oriented sectors in 2026. Companies are eagerly awaiting such a turnaround, given that the lack of demand is a major concern for many companies, including those in food manufacturing. That’s not surprising if you consider that sales volumes in EU food retail are only growing at a modest pace, and sales volumes in food service are trailing behind.

For non-food retail, there could be an uplift in categories like electronics and furniture as we move further away from the pandemic, when consumers overpurchased on (semi-) durable goods. One thing that consumers and business travellers do spend more on is on air travel, which lifts the growth rate for aviation above the average for the transport and logistics sector.

Read the original analysis here: 3 calls for EU sectors in 2026: Tech outperformance, manufacturing growth gaps, small consumer gains

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.