Emerging markets: Which sovereign debts are most vulnerable to rising global financial volatility?

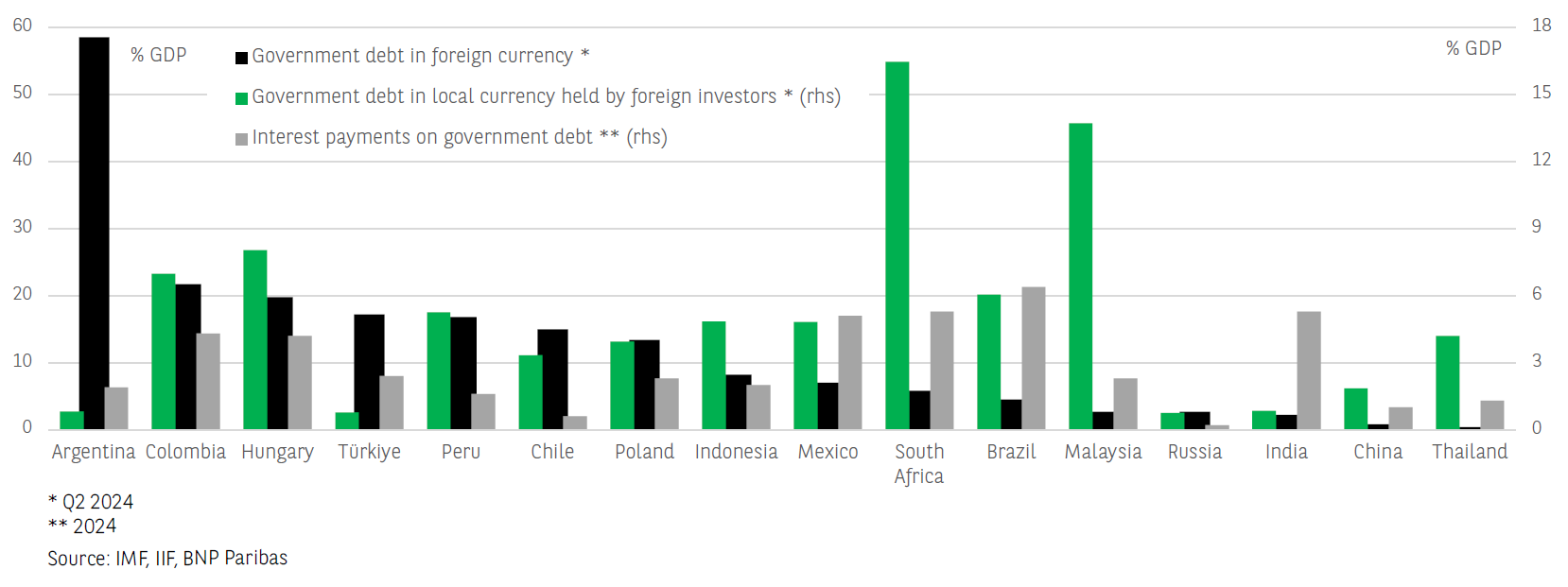

Resilience of external financing conditions overall. The election of Donald Trump to the White House has caused a rally in the US dollar and revived uncertainties about the external financing conditions of emerging countries. The Argentinean peso, the Turkish lira and the South African rand are among the emerging market currencies that recorded the largest depreciations between November 5th, 2024, and February 24th, 2025, losing 6.3%, 5.7% and 5.2% of their value against the US dollar, respectively. Overall, emerging sovereigns should be relatively resilient against a stronger dollar and the risk of increased investor selectivity towards risky assets. However, all of them are not in the same boat. As the chart shows for the main emerging market economies, the exposure of government debt to currency risk, foreign capital outflows and interest rate risk varies greatly across sovereigns.

Exposure of government debt to currency risk, capital outflows and interest rate risk

But exposure to currency risk varies greatly. On the one hand, looking at the ratios of government debt in foreign currency to GDP, we observe that South American countries, with the exception of Brazil, are among the sovereigns most exposed to currency risk. They are more so than in 2016, because government debt in foreign currency in these countries has increased since then: this is the case for Argentina, whose government debt in foreign currency rose from 43% of GDP in 2016 to 59% in Q2 2024, but also for Colombia (from 15% to 22%), Peru (from 9% to 17%), and Chile (from 3% to 15%). The dynamic is the opposite when we look at Eastern European sovereign borrowers (Hungary, Poland, Czech Republic), which have reduced their exposure to currency risk since 2016. For Hungary and Türkiye, whose government debt in foreign currency reached 20% and 17% of GDP respectively in Q2 2024, the exposure to currency risk remains high. However, since Türkiye’s total public debt is relatively moderate, at 29% of GDP, in the event of an exogenous shock it should have more room for manoeuvre than Hungary, whose total public debt reaches 72% of GDP. Finally, the exposure of Asian sovereigns to exchange rate risk has changed little since 2016 and remains very limited, with the exception of Indonesia.

And so does exposure to capital outflows. On the other hand, the uncertainty generated by the new U.S. trade policy is likely to lead to foreign capital outflows from emerging markets. Emerging sovereigns are exposed to these capital flights via their debt denominated in local currency but held by non-residents. Investment outflows from non-residents have the potential to generate high volatility in bond yields and especially in exchange rates, due to the direct impact of local currency securities sales on the local foreign exchange market. Sovereign borrowers of South Africa and Malaysia, whose local currency debt held by non-residents reached 16% and 14% of GDP respectively in Q2 2024, are highly exposed to such capital outflows. To a lesser extent, Hungary and Colombia are also exposed, adding to the vulnerabilities related to the large stock of foreign currency-denominated government debt in these countries.

Potential rise in the interest burden. In addition, the Fed's monetary status quo could force the central banks of emerging markets to delay their own monetary easing cycle or even tighten their rates further. This would increase the interest burden of many sovereign borrowers, while it is already large for several of the major emerging market economies and it has stood at alarming levels for many developing countries (Ghana, Kenya, Zambia, Jordan, Pakistan, Costa Rica, Jamaica).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.