Economic Commentary: Tracking Trade Conflicts in Asia and Mexico

When I scheduled my annual trip to Asia earlier this year, I was hopeful that trade frictions with China would be resolved before the journey. Instead, the acrimony between the main antagonists has increased. While this made my conversations more difficult, it also increased their value. Here are the main takeaways I gleaned from my long series of interactions across four countries late last month.

- It is hard to overstate the differences in style between China and the United States. The Chinese are measured, patient and subtle. They view Washington’s posture as impulsive and unproductive. Several people in Beijing referred to the increase in tariffs and the restrictions placed on Huawei (China’s champion telecommunications firm) as “not the actions of a trusted partner.”

There are certainly those in the United States who would assert that China has not been a trusted partner, given its alleged theft of intellectual property and its failure to deliver on promised economic reform. Hard-liners in Washington believe China has evaded these issues for far too long, and tough tactics are warranted. Indeed, by subjecting them to a measure of economic discomfort, these measures have gotten the attention of the Chinese.

Tactics aside, the central question is whether America and China can reset the terms of their trade relationship without significantly disrupting the world economy. The rising antipathy between the two could place the global expansion in peril.

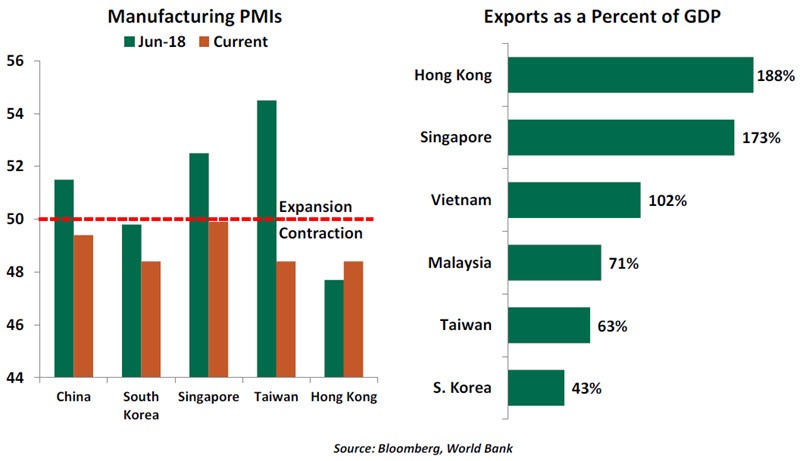

- Developing countries reliant on commerce with China or the U.S. find themselves caught in the middle. Several nations in Asia are heavily dependent on exports for economic growth, and their trade flows are already constricting. (No matter how many times I visit the region, I am always amazed by the number of container ships lined up outside of the ports of Hong Kong and Singapore.)

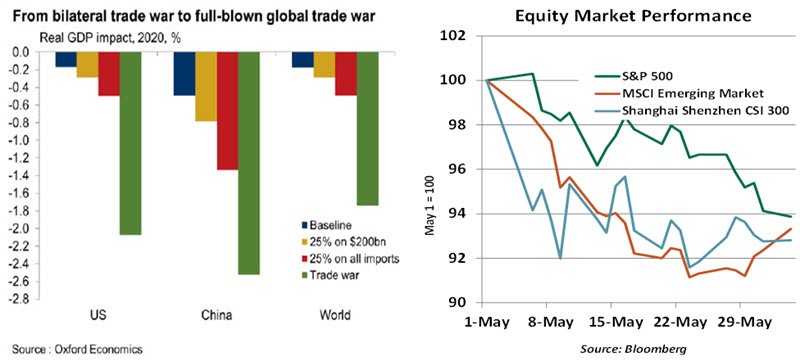

Even if the rhetoric eases and discussions resume, the resulting uncertainty surrounding the situation is harmful to commerce. Confidence and investment indicators from around the world are slipping, presaging slower growth in the second half of the year. Australia’s central bank cut its interest rates this week; the Federal Reserve may be forced to follow in the second half of this year.

“Rising trade tensions are creating unwelcome uncertainty.”

- China is taking aggressive steps to offset the trade conflict’s contractionary influence, including tax cuts, infrastructure spending and increased lending to small and medium-sized businesses. During a conference I addressed in Beijing, senior policy makers repeatedly stressed the importance of supporting the flow of credit to entrepreneurs. In total, the measures amount to the sizable sum of about 2% of Chinese gross domestic product (GDP).

The reservoir of options for China remains fairly deep, but could come at the long-term cost of financial stability. Until last summer, China had been waging a successful battle against credit excesses. The trade conflict has forced the country to retreat, at least for now.

- Trade frictions are teaching us a valuable lesson in how global supply chains work. Many products we buy include components from a variety of countries, and are often assembled in one place and sold in another. This greatly complicates the analysis of who is most affected by tariffs.

As a prime example, Huawei mobile phones include chips and software made in the United States; China’s primary involvement is assembly. The sanctions on Huawei will therefore have immediate consequences for American companies, and American consumers will be paying a lot more for cellphones.

Shifting these chains is not easy, and doing so will be expensive. While some production has already moved out of China and into peripheral Asian countries like Vietnam, the sheer scale of China’s capacity makes the country impossible to replace.

- The U.S. administration’s frontal assault on Huawei could be an even more dangerous accelerant to the trade conflict than are the tariffs. The provision of hardware and software for the next generation of telecommunications (known as 5G) is at the center of China’s long-term economic plan. The goal is to be first and best, to win global markets and diversify away from the manufacture-for-export model that is losing momentum.

Of course, telecommunications equipment can be used for both civilian and strategic purposes. The United States has used this angle to encourage allies to turn away from Huawei. The campaign has been largely unsuccessful: after all, American providers could arouse the same kind of suspicion. (During a meeting in Hong Kong, I noticed Cisco microphones embedded in a conference table, and speculated that our conversation was being piped directly to Washington.)

“Tariffs aren’t the only form of trade restrictions, and may not be the most pernicious.”

That led the U.S. administration to designate Huawei as a controlled entity, requiring firms doing business with Huawei to apply for a license (which would presumably be difficult to get). Huawei’s U.S. suppliers have started to pull back from their relationship with the company, hindering production. China has retaliated by using its cybersecurity law to limit access for US technology providers, and is threatening to restrict the supply of products containing certain rare earth minerals.

Measures and counter-measures are not uncommon during trade negotiations, as each side tries to establish leverage over the other. These declarations can be used as bargaining chips when talks resume. But there is no timeline for renewed discussions; in fact, the rupture in the process seems to be widening.

- The impact of tariffs is not linear. S. importers have responded to the initial 10% tariff with a combination of supplier concessions, price increases and margin compression. Raising the tariff to 25% will dramatically alter the equation, likely resulting in higher consumer prices and lower levels of profitability for American firms. And if tariffs are ultimately extended to all U.S. imports from China, the economic damage will be deepened.

The effect of heightened tariffs may take some time to emerge. Many firms have been stockpiling raw materials and intermediate goods as a hedge against a bad outcome on the trade front. But once these inventories are depleted, the consequences will become more apparent.

A faltering economy is not a particularly strong platform on which to run for re-election. But at the moment, President Trump seems intent on seeking redress for what he perceives as a long series of Chinese trade offenses. He and his aides are betting that either the Chinese will capitulate (unlikely in our view), or the American electorate will look past any economic discomfort and applaud the tough stance. So far, U.S. equity markets have held up relatively well, but bond markets are less sanguine. Interest rates in developed countries have fallen sharply in the last month.

“Continued trade stress will imperil the global expansion.”

It is often said that expansions do not die of old age; something kills them. That “something” is usually a policy error. Unfortunately, what we are witnessing on the trade front from China and the United States could turn out to be exactly that kind of miscalculation. The June G-20 meeting in Osaka will give Presidents Xi and Trump an opportunity to re-set the process. It will be in everyone’s best interests if they take it.

Game Changer

The U.S. administration’s reliance on tariffs to extract trade concessions is old news. But last week, the president changed the scope of the trade conflict by invoking the International Emergency Economic Powers Act to place a tariff on all imports from Mexico. These latest tariffs are meant to motivate Mexico to curb the flow of migrants through the country and across the U.S. border. We call this decision a “game changer,” but this is not a game.

Starting on June 10, President Trump intends to impose a 5% tariff on Mexican goods. The levies will prospectively escalate an additional 5% every month, until reaching a total of 25% by October 1. With the potential to deliver significant costs for both economies, the announcement has rattled markets and businesses.

In addition to having a long and relatively stable trading relationship with the United States, Mexico is America’s third largest trading partner (after China and Canada). U.S. imports from Mexico last year amounted to $347 billion while goods worth $265 billion were exported. But trade numbers show only a part of the deeper economic relationship.

Tariffs will likely put pressure on the regional supply chain networks that underpin millions of American and Mexican jobs. The initial impact would be worse for Mexico, as exports to the U.S. account for 80% of its total exports. (Exports to Mexico comprise 16% of total U.S. exports.) But U.S. corporations would be forced to reevaluate their operations within the region, which could do considerable harm to their profits and the U.S. economy.

As a primary example, automakers will likely suffer the most from disruptions in the supply chain. Car producers such as General Motors, Ford, Fiat Chrysler, Nissan and Volkswagen rely on Mexico for a sizeable share of their North American production. But the point of final assembly doesn’t tell the full story: Parts and components used in Mexico’s plants often come from the U.S., and vice versa. The challenge is not limited to the automotive sector. Medical device makers of pacemakers and artificial respirators have similar supply chains with facilities based in the Mexican border city of Tijuana.

According to Oxford Economics, the implementation of the full 25% tariffs would push the Mexican economy into recession, with its GDP falling by 1% next year. Maximum tariffs will also reduce U.S. GDP growth by at least 0.7 percentage points in 2020. Ironically, a weakened Mexican economy will likely prompt more migrants to seek better prospects in the U.S., rendering the policy antithetical to its stated mission.

Mexico is seeking to avoid implementation of tariffs, but if the U.S. decides to move forward, it is likely Mexico will respond more forcefully through retaliatory measures targeting politically sensitive sectors in the U.S.

American farmers, who only recently got a reprieve from Mexico’s and Canada’s retaliatory tariffs, could come into the line of fire yet again if Mexico decides to retaliate. The energy sector, including natural gas, would also be affected. Though the quantity has declined over the past few years, American refiners import a reasonable amount of Mexican crude oil (8% of total imports) before exporting it back in the form of gasoline. If Mexico decides to retaliate with tariffs, U.S. energy exports would take a hit. In the end, the American consumer will foot the bill for tariffs.

“Tariffs will hurt both Mexico and the United States.”

The U.S. Congress, which has the power to overturn the decision, has been getting restless. Opposition to the move is growing on both sides of the aisle. While Congress has broadly been supportive of the administration’s moves against China, an intervention on the topic of Mexico tariffs is essential to saving the important United States-Mexico-Canada Agreement (USMCA).

Some pundits view the recent tariff threats as a strategy to simultaneously hasten the ratification of the USMCA before Congress takes its recess in August and put pressure on Mexico to curb the flow of migrants to the U.S. But such a tactic carries high risks and real costs to businesses and workers. While the latest move has altered the game, it will not create any winners.

Author

Northern Trust Economic Research Department

Northern Trust